The Devil is in the Footnotes: The Fourth and Fifth Levers OMB Has Over Agencies

This is a free piece of Notes on the Crises. All pieces in this OMB series will be free. Please take out a paid subscription to support this work. Or leave a tip.

Joshua Lawrence is a research fellow at Notes on the Crises and graduate of Sarah Lawrence College. Find him on Bluesky here.

Juan Hanes is a research fellow at Notes on the Crises and a Journalism student at NYU. Find him on Bluesky here.

Today we are returning to our ongoing “seven levers” series about the Office of Management and Budget’s Resource Management Offices (RMOs). To remind readers, the “Levers” are those mechanisms these RMOs use to influence administrative agencies and determine both the form, function and amounts of their budgets. In the last installment, we talked about the three levers available to the RMOs during the “budget preparation” stage. Today, we move on to the levers available during the “budget execution” stage. Unlike much of what we discussed last time, the levers in this stage are granular, detailed, and very difficult to observe from the outside.

Before beginning, we will remind readers that this series is based on the writing and research of Georgetown Law Professor Eloise Pasachoff, whose 2016 paper on the RMOs lays out these mechanisms for control and defines them as “levers”. This series—and much of our OMB project at-large—draws on and is inspired by her work.

But with that being said, let’s first explore a simple question: what is the budget execution phase?

When does budget execution begin?

In the first two parts of this series, we went to great lengths to explain, well, the great length of the budget preparation stage. OMB, though originally born out of the “need” to centralize the formulation of the president’s budget, involves itself intimately in both the presidential budgeting process, and the subsequent congressional budgeting process. All in all, we established that the “budget preparation” phase at large lasts somewhere between 18 and 21 months—and maybe even longer.

When that process is all said and done, though, the “budget” for that fiscal year has become law and now it's time for the budget to be implemented. But how do we determine that the preparation process has ended?

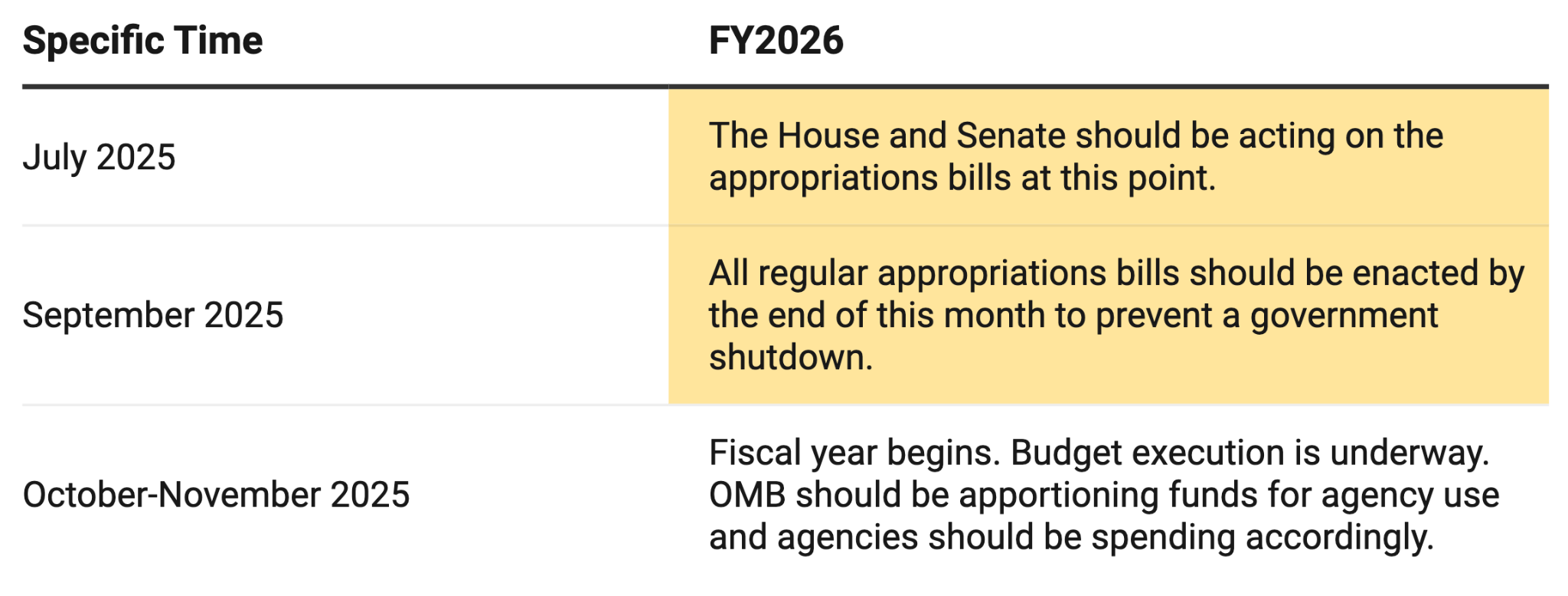

Well technically, the preparation phase has no clean ending. In the (not-so-simple) simplified chart we created in part one of this series, we wrote—perhaps deceptively—that the budget preparation stage reaches its final phases in the last three months leading up to the turn of the fiscal year (July-September). This “winding down” of the preparation phase, though, is typically the most explosive, well-documented, and controversial part. This is when Congress is battling with itself and the president and the public to get the 12 “appropriation bills” passed in time. See below a very abridged version of our chart that focuses on those last few months of the budgeting process. The “budget preparation” phase has again been highlighted in yellow.

Now, if you were paying attention to the very loud budgeting back and forth of the last six months of 2025 (or if you were keeping up with Notes on the Crises coverage), you’d know that the transition from “budget preparation” to “budget execution” was not as smooth or timely as our chart might suggest. This is due to the constant appropriations crises of our modern government regularly delaying and complicating the transition between the two stages. The full effects of such crises and OMB’s role in them will be the topic of the next installment in this series. But for the time being, we will focus merely on an imagined world in which our government was capable of passing a budget in advance of each fiscal year, the government never shutdown and ad-hoc “continuing resolutions” were not necessary to provide stop-gap appropriations for basic agency activities.

Under our heroic (and heuristic) assumption of congressional competence, we can say that the “budget preparation” phase for a given fiscal year ends with the passage of the 12 appropriations bills. Therefore, the “budget execution” phase correspondingly begins on October 1 — the first day of the fiscal year. And with that, we can now explore how the budget is actually executed.

How does budget execution work?

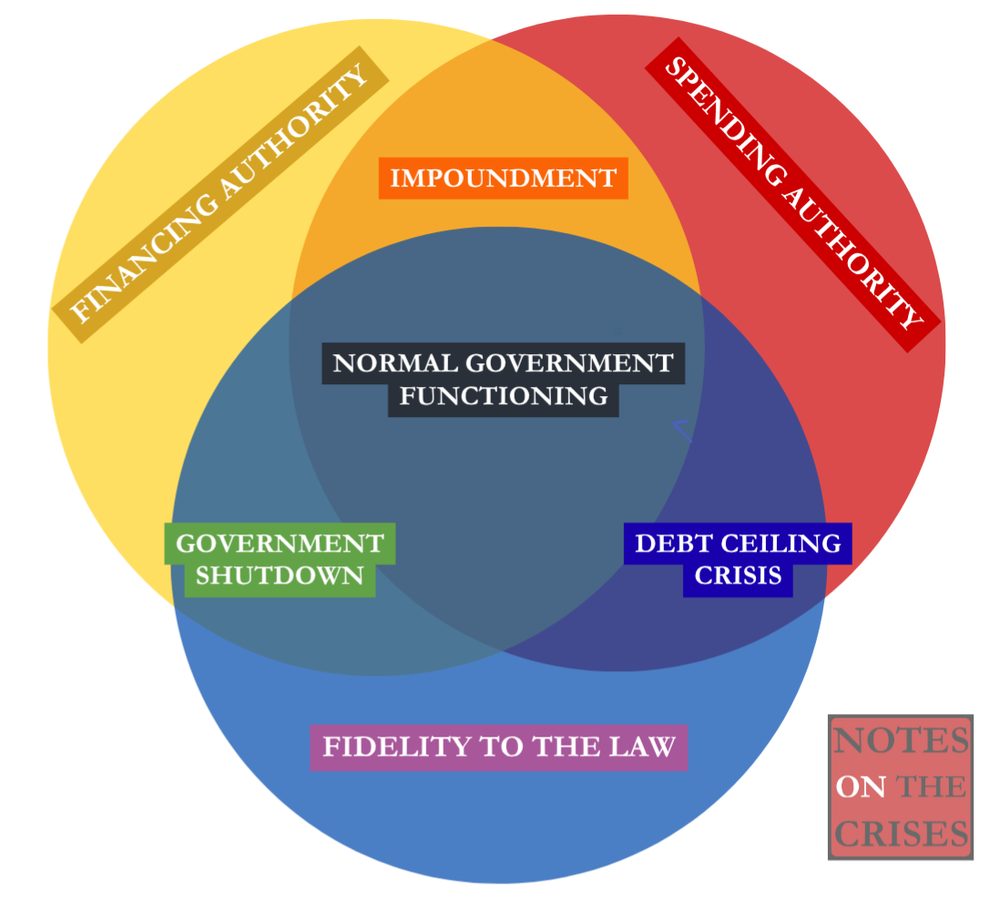

It may be useful to refer back to a graphic Nathan created last year which showed that “normal government functioning” was the intersection of adequate financing authority, spending authority and a basic fidelity to the law in creating and executing government policy. The distinction between “spending authority” and “financing authority” is useful here insofar as it reminds us that agency authority to spend is different from the treasury’s authority to finance spending. As Nathan laid out in his “OMBification of DOGE” piece, the OMB administers a kind of “internal money” for the administrative state but actual agency payments are processed by the Treasury’s Bureau of Fiscal Service (BFS) and come out of the Treasury’s main bank account, the Treasury General Account (TGA). To put it simply, a single appropriations bill will create many individual budget authorities that the Office of Management and Budget interprets and creates “appropriations accounts” based upon.

These “appropriations accounts” are often referred to as “jointly administered” by the BFS and the OMB, but this is somewhat misleading. Precisely how these accounts are administered will be the subject of future pieces. For now what's important is that the BFS’s administrative responsibilities related to “appropriations accounts” is processing payments that “come out of” these accounts and to track these payments for financial reporting purposes. It is the Office of Management and Budget which defines the appropriations accounts, determines their balances and both interprets congressional restrictions on these expenditures and creates their own. Unless an agency is very small, it will typically have multiple appropriations accounts with the OMB, each pertaining to a certain agency function as determined by congressional appropriations legislation.

It is the good old OMB that “helps” agencies manage and spend their “unobligated balances” throughout the year. The office ultimately derives a large degree of its authority from the “Antideficiency Act”, which was first passed in 1870 and has been amended countless times since then. Understood simply, the Antideficiency Act aims to prevent agencies from “overspending” their budgetary authority and running out before the year is over. As the story goes, prior to the Act, some agencies would strategically spend their full appropriations before a fiscal year was over as a way of forcing Congress to increase their budgets. The Antideficiency Act made such overspending illegal, and in its modern form, OMB is tasked with managing agency budgetary authority to prevent such practices.

The tool for managing spending is none other than “apportionment”, the obscure legal mechanism that we’ve mentioned in our first OMB memos breakdown. Apportionment, as executed by OMB, splits an agency’s budgetary authority into various chunks that the agency can gain access to over the course of the fiscal year. This splitting is done by time, project, or both, often meaning that an agency will only be allowed to spend X amount of money during a given month or quarter, and that a good chunk of that money might only be legally spent on certain “projects” as deemed by OMB.

This apportioned amount, of course, is only a fraction of the total budgetary authority that Congress appropriated to that agency for the year. To put this into “monetary” terms, congressional appropriations are a kind of congressional “check” to agencies. However the institution that processes the “congressional check”, the Office of Management and Budget, does not “process” that check how we are used to. Have you ever deposited a check into your bank account but only had a portion of the funds available to spend? Apportionment is an analogous process to that, whereby only a portion of the “congressional check” is made available for expenditure—or “obligation”—for a given fiscal quarter (or even month) and agencies will have to wait three months before more of an appropriation account’s balance is “released”. To be absolutely clear, apportionment subdivides the funds in an “appropriation account”, but does not create “new” appropriation accounts.

(For an interesting discussion of these congressional “orders to spend” and a unique proposal to modernize them, see Willamette Law Professor Rohan Grey’s paper “Digitizing the Fisc”)

Once budgetary authority has been apportioned, an agency then has the power to “obligate” it, meaning that the agency can enter legal agreements wherein it agrees to give another party a certain amount of money in exchange for a good or service. Once that obligation has been “executed”, the Treasury General Account is debited through Bureau of Fiscal Service payment processing, the agency’s available balance is debited by the OMB and money finally enters the wider economy.

The unfolding of the above process, repeated thousands of times across the various agencies day-in and day-out, is what we might call the “execution” phase of the budgetary cycle. Budget execution for administrative agencies is less tied to the “fight” for additional appropriations and instead about adhering, and objecting to, the OMB’s administrative choices in the apportionment process while engaging in appropriation financial management processes to prevent their accessible budgetary authority from reaching zero. As we are seeing in the current impoundment crisis, that process of "adhering and objecting” to OMB administrative choices is not neutral or apolitical, even if it is “technocratic”. Let’s talk about the levers that OMB has over agencies in the budget execution phase then

The Specification Lever (as manifest through apportionment)

Ultimately, budget execution, though much more time consuming and logistically demanding than what comes before, is much more conceptually simple than the budget preparation phase. As a result, there are “only” really two ways in which OMB injects itself into the process: via specification on how to execute the budget and via the subsequent monitoring thereof. Specification itself is quite complex—especially when the government is amidst an appropriations crisis. But for this piece we will focus solely on the primary means by which this lever is pulled.

Specification manifests first and foremost through … you guessed it: apportionment. As our explanation of the process might have indicated, the ability to divvy up an agency’s budgetary authority and disburse it over the course of a year offers OMB quite a few opportunities to massage agency policy. This is true in every presidential administration, as we will get into, since apportionment gives OMB the power to demand agency compliance with certain policy choices in exchange for the disbursement of budgetary authority. But under a president like Trump and a director like Vought, this carrot-and-stick mechanism can become much more coercive. The fact that OMB is the central intermediary between administrative agencies and the processing of government payments to employees and outside suppliers gives it enormous power. In short, the OMB is a critical “chokepoint”. You might even say that it's the Federal Government’s internal “Strait of Hormuz”. This is quite the convenient power for an administration that claims to hate spending money but, in reality, hates legislative power and, above all, hates legislative power utilized to restrict executive power.

But before we can even explore the most creative and destructive ways that OMB under Vought can exercise this specification power, we should first understand this lever at its most innocuous and procedural level.

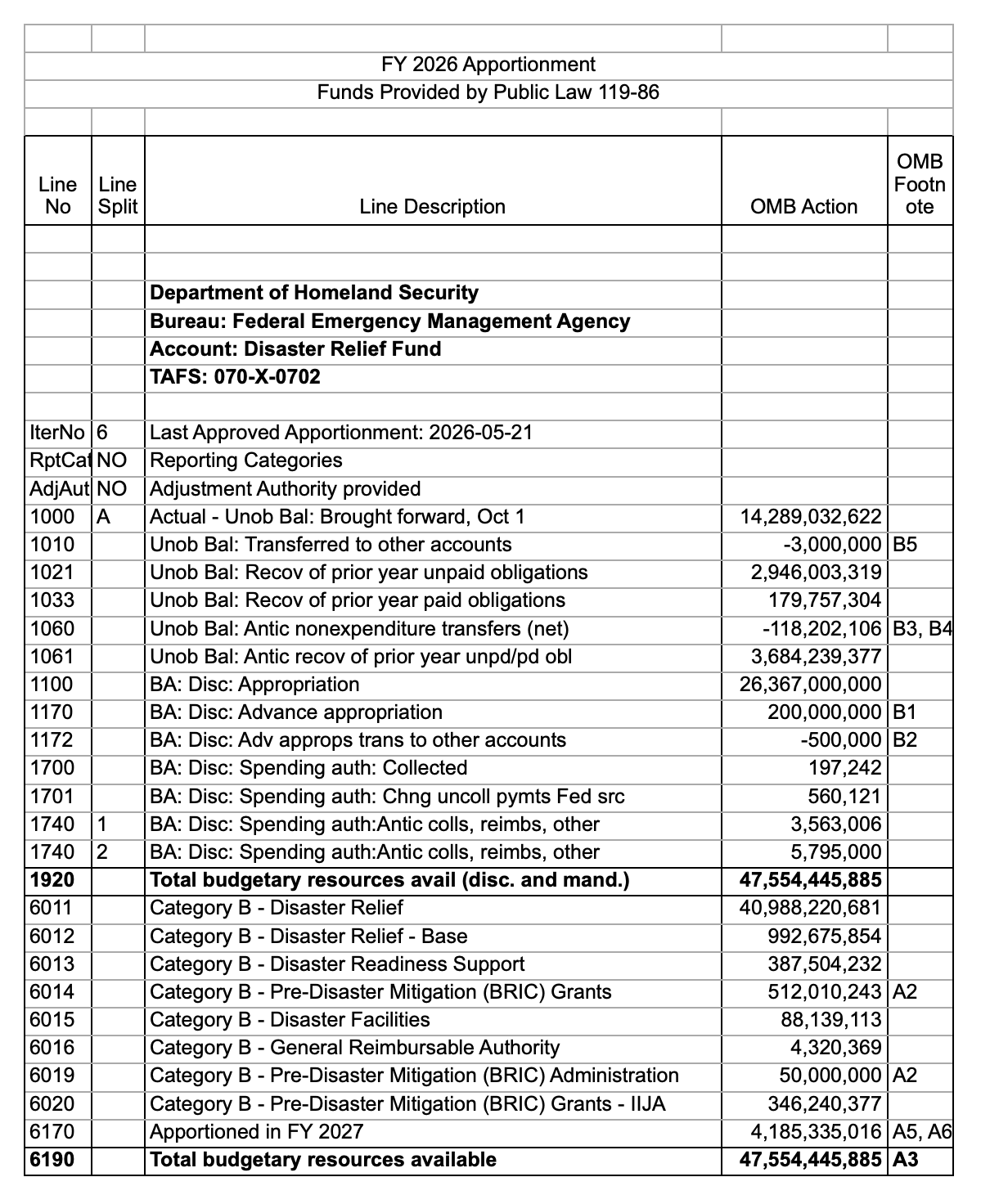

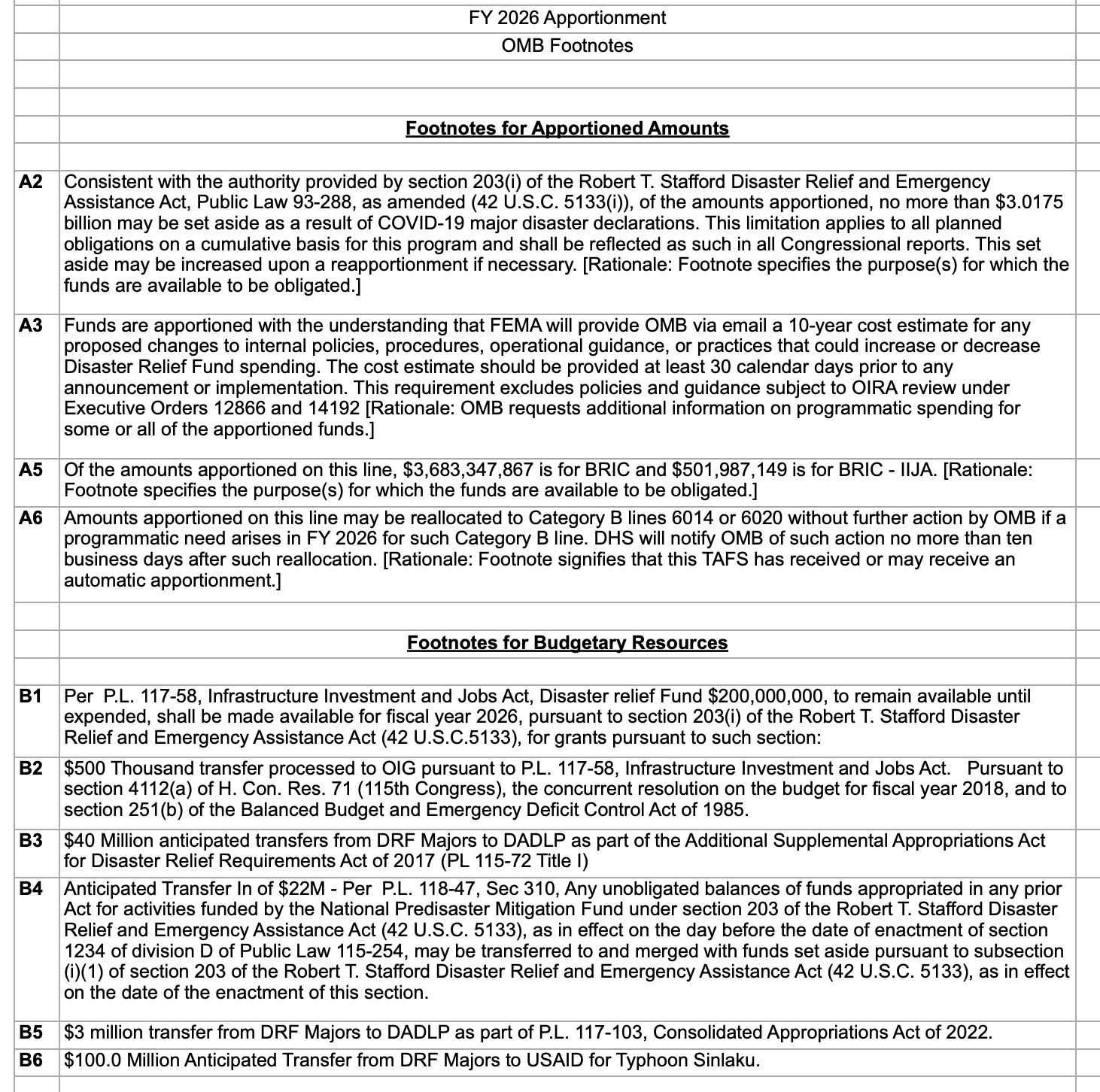

Shown in the above image is the most recent apportionment for FEMA’s Disaster Relief Fund appropriation account (this information is courtesy of Project Democracy’s OpenOMB and the incredible work they do to ensure that apportionments are visible to the public).

We know what you are thinking. This looks like a random collection of half-spelled words and big numbers that an LLM spit out in a particularly strange “hallucination”. Its not, but we won’t try to torture you until you can read this modern bureaucratic cuniform. At least … not today. Instead, we show this only to get readers accustomed to seeing this monstrosity … but also to highlight one specific feature of apportionment.

Please direct your attention to the two columns on the right side of the spreadsheet. The column with all the numbers is titled “OMB Action”; this is where we get to observe what changes OMB is actually making to the FEMA account’s budgetary authority. In the next column, we see “OMB Footnote”, with only some items having a corresponding alphanumeric code attached to them. What could these footnotes possibly mean? Well thankfully, when you download an apportionment, you not only get a sheet containing the actual numbers, you also get a separate sheet explaining the footnotes. Take a look at that sheet below.

As Duke Nukem would say, “wow thats a lotta words, too bad I’m not readin em”. Thankfully, we don't need you to try and read or understand a “raw” apportionment. But we will highlight the first footnote in order to get to the main reason why we are showing you all of this:

Consistent with the authority provided [by the law] …, of the amounts apportioned, no more than $3.0175 billion may be set aside as a result of COVID-19 major disaster declarations. … This set aside may be increased upon a reapportionment if necessary.

If you have read this and are still following along, then you might understand now why we want you to see this. Put simply, with the power to apportion funds comes the power to attach footnotes to a given apportionment. These footnotes, as demonstrated in the above example, allow OMB to stipulate how or when apportioned money may be used. In the case above, the stipulation is that only about $3 billion of the money appropriated towards pre-disaster relief grants can support COVID-related disasters. This is a carryover footnote from the Biden administration, when caps were placed on outgoing FEMA grants as many reports suggested that large amounts of improper payments were being disbursed via the government’s COVID response programs. It's important to note that these kinds of improper payments are a question of an agency’s internal controls, as former BFS employees emphasized to Nathan last year.

Our chosen example demonstrates the power of footnotes at a fairly procedural level, but even here we can see how OMB’s apportionment power can be leveraged to make some political or ideological decisions. Professor Pasachoff refers to these as “value-laden” decisions. As mentioned, this particular footnote was carried over from the Biden administration’s efforts to clamp down on alleged COVID grant fraud. The authority to set this particular cap was pulled from the “Stafford Act” and a related amendment, which stated that the President has the power to determine whether or not natural disaster claims made by local governments are deserving of funding.

The idea that the best way to deal with allegations of fraud is to put a flat cap on how much money can be spent to alleviate a worldwide health crisis can hardly be considered an uncontroversial or technocratic decision. Clearly, with great footnote writing power comes great footnote writing responsibility. And beyond our (randomly) chosen example here, we can reference one other instance where the Trump administration famously wielded that power against Ukraine during the president’s first term. Well, the incident is famous. But the mechanism is not.

Back during Fiscal Year 2019, Congress had appropriated $250 million dollars for the “Ukraine Security Assistance Initiative” —a program to provide military training and weapons to Ukraine. When OMB began apportioning the relevant account for the year ahead, they included a very odd footnote under the Ukraine assistance funds. Take a look at what was written:

Amounts apportioned, but not yet obligated as of the date of this reapportionment, for the Ukraine Security Assistance Initiative (Initiative) are not available for obligation until August 5, 2019, to allow for an interagency process to determine the best use of such funds. Based on OMB’s communication with DOD on July 25, 2019, OMB understands from the Department that this brief pause in obligations will not preclude DOD’s timely execution of the final policy direction. DOD may continue its planning and casework for the Initiative during this period. [emphasis added]

The apportionment was signed on July 25, meaning that OMB was withholding the power to obligate the funds for about 10 days. On August 6, though, a day after the funds were supposed to become available, OMB released another apportionment with a footnote declaring that the funds were to be withheld until August 12. This pattern of delays continued up until September 12, when OMB quietly removed the footnote. By that point, though, it was too little too late, and $214 million of the originally appropriated amount went unobligated as the funds expired just a few weeks later. In other words, they canceled a congressional appropriation by administrative fiat.

Congress ended up reappropriating the funds for the following fiscal year, but Trump’s efforts to withhold the money would not go unnoticed. As it turned out, this episode was part of a wider effort by the Trump administration to pressure Ukrainian President Volodymyr Zelenskyy into investigating the Biden family in the lead up to the 2020 election. Many readers might remember that it was this series of events that led to Trump’s first impeachment in December 2019.

Between the two extremes of OMB footnotes — with one side being fairly procedural and the other side being brazenly illegal — there remains a whole world of ways in which OMB can direct agency policy or straight up impound funds. The typical strategy for slowing down the obligation of funds that OMB would rather not see disbursed is to make agencies jump through dozens of hoops before they are allowed to use their money. Long questionnaires, sets of complex instructions, and tedious requests for information have all been included in footnotes as non-negotiable requirements to fulfill before funds were made available. Per Shelley Lynne Tomkin’s 1998 book on the OMB, there is even a legend of one examiner who issued footnotes that were each hundreds of pages long.

No matter what strategy an examiner or OMB official uses, though, the end result is the same: footnotes help to slow, modify or entirely prevent administrative agency use of congressional grants of agency budget authority. And where footnotes fail to go that far, they still often force agencies to use the money in the way OMB wants. The room to inject the policy interests of the White House is thus absolutely enormous.

The Monitoring Lever

It is difficult to say much about the “monitoring” lever because, as Pasachoff noted in her original article, it is perhaps the most "ambiguous" of them all. In truth, this lever encompasses not just the budget execution phase, but all of the budgeting process and beyond. Moreover, the fundamental concept of this lever is something we have referred to time and time and again throughout this series.

In short, the monitoring lever reflects the fact that OMB’s program examiners are omnipresent within the agencies. As we have hopefully made clear throughout the series, OMB is notable not only because it has the final say in agency activity, but also because the office makes its presence known throughout every step of the process. This omnipresence is the monitoring lever manifest. OMB, primarily via its examiners but also through the higher level staff, has the power to monitor and interfere with agency activities on a near constant basis. This allows for an unending stream of OMB and White House policy to be injected into the agencies as they carry out their mandates.

The actual mechanism that enables the monitoring lever to work is first and foremost the clearance process we have talked about many times already. The fact that agencies need to clear basically every externally published document with OMB means that effectively nothing leaves the administrative state without going through a program examiner beforehand. With agencies already anticipating discussion and conflict with OMB, it becomes only natural that they might work to anticipate the decisions of their examiner before they are even made. In this sense, the monitoring lever works to massage agency policy even when the examiner is not right there in the room with agency officials.

But as we have referenced indirectly in past pieces, program examiners are not just OMB employees on the other end of a phone or an email. They also engage in program examination by showing up to administrative agencies in person. When in person, they ask numerous questions demanding justification for agency decisions. After in-person justification, examiners will routinely markup agency documents, and send them back demanding revisions. Sometimes, as John Hudak noted in conversation with many officials in the government, OMB examiners will even revise and publish agency documents without ever going back to the agencies for consultation.

In effect, the monitoring lever works in multiple ways. In part, the lever serves to pull agency decisionmaking in a certain direction via the constant interactions with and demands from examiners and higher level OMB officials. On the other hand, the understanding that OMB serves as the end all be all for agency action means that those in the administrative agencies feel compelled to fall in line even when OMB is not directly making demands. Pasachoff notes that this lever grants incredible power to the examiners, but that such power also moves up the chain of command, enabling the Deputy Associate Directors, Program Activity Directors and the top-level Directors to affect agency policy via monitoring.

To that end, we will highlight that when the Trump administration sought to withhold aid from Ukraine, the Government Accountability Office found that OMB had moved those particular apportionment duties out of the hands of the program examiners and into the hands of the PADs. In essence, this shows how the otherwise technocratic-seeming monitoring powers of the examiners can be co-opted and placed into the hands of political appointees.

Outside of this broad overview, though, it is difficult to pin down the exact workings of the monitoring lever. It manifests in countless different ways and appears in tandem with many of the other levers we have described in the series thus far. But it is crucial to recognize that the informality of the monitoring lever is itself what makes it so powerful.

That is all for this installment of our “Seven Levers” breakdowns. In the next installment, we will nuance our understanding of the “budget execution” phase, by looking at how OMB involves itself when the transition from “preparation” to “execution” is held up by political crises.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025