Banks as Debt Monetizers: Monetary Policy 101

The Shtetl Bank Comes to Town

#MonetaryPolicy101 is a weekly series about the basics of monetary policy. This is the Fourth Post. See Post 1 here, Post 2 here and Post 3 here. If you like this series please consider taking out a paid subscription here. It is reader support which sustains my ability to treat this substack as a full time job.

In last week’s post I said:

What the shtetl needs is to increase the “moneyness” of their IOUs by gaining the legal right to settle payments with them. The problem with the current system is it is a set of bilateral (two way) debts with limited transferability and usage possibilities for each IOU. In other words, the payment system in this little town is diffuse, fragmented and unreliable. Of course, this type of system isn’t simply a free ride. In small communities with bilateral, informal payments you can be sure to be ridiculed if you don’t return the favor. The trouble is that these enforcement mechanisms are grounded in local knowledge and have very little in the way of formal third party enforcement or use beyond the local area. If money is indeed “what a payment system does” then making IOUs more widely acceptable, more easily transferred and payment processing faster is in a very literal sense improving and streamlining money itself. Next week we’ll expand our purview to banks, but for today we’re going to start with an entity called a “clearinghouse”.

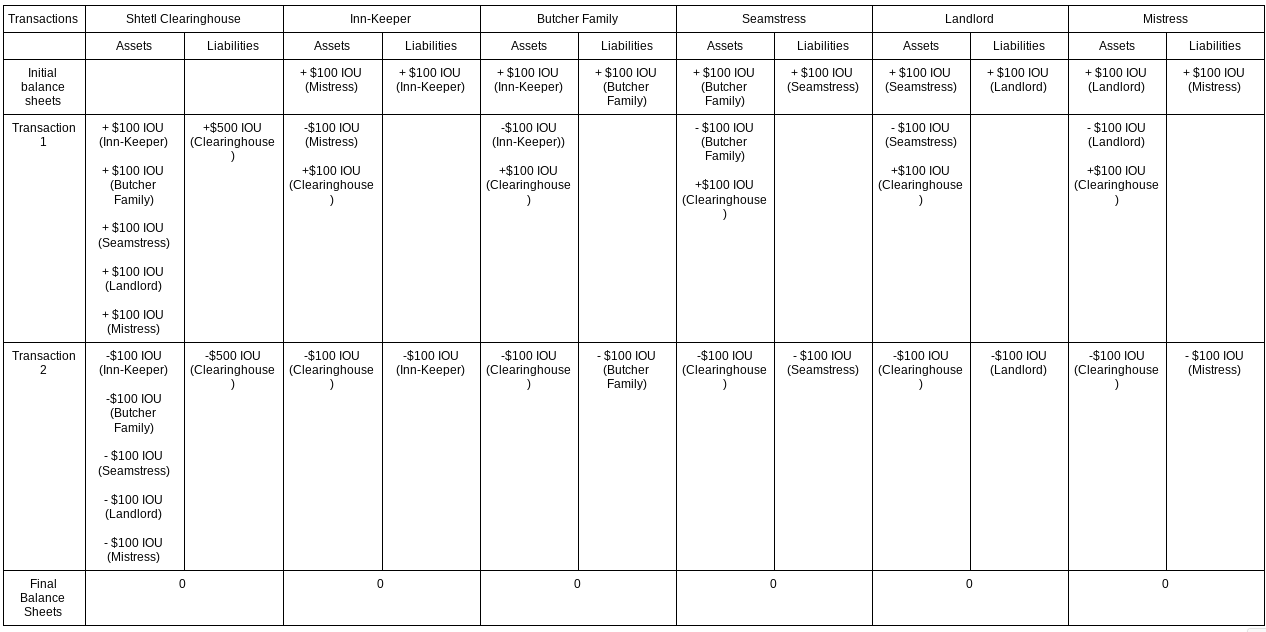

If you read the paragraph above carefully, you’ll notice that the key problem for individuals is increasing the “moneyness” of their liabilities. Another way of saying that is this: they need their debts monetized. Last week I told that story through the institution of the clearinghouse. The trouble is, it is very difficult to build a system based on individual membership in a clearinghouse. In our simplified shtetl example there is a small, tight-knit community and it is easy to settle payments between people. More importantly, everyone joined the clearinghouse with the understanding that they all owed and owned the same face value of IOUs and thus all would fully shed their debts by participating. That was, of course, a big simplification. Once all payments are netted, someone could easily still owe a substantial amount of money to the clearinghouse. What if they can’t pay it? The question of default uncertainty in a clearing system brings up sticky issues of collateral- as well as valuation. In our simplified example the clearinghouse is accepting the notes of individuals at face value without taking into account default uncertainties. The seamstress probably has a higher likelihood of default than the landlord. This system would likely break down if the clearinghouse tried to apply different “discount rates” on each IOU and arriving at different “collateral prices”. It is here where banking enters. First though, let’s look back at the Shtetl clearinghouse.

There are a number of interesting things that I think are worth highlighting about this set of transactions in light of today’s topic. First, the clearinghouse IOU is “money” in this circumstance. It can be used to make payments to the clearinghouse itself, as well as other individuals in the Shtetl. By swapping his IOU for the clearinghouse IOU, The Butcher’s IOU has become “monetized”. We hear a lot about debt monetization but usually only in the context of the Federal Reserve purchasing government securities. However, that kind of “monetization” is much less significant (as I’ll write about more in the future) than swapping individual IOUs for newly created money. The Federal Reserve is simply swapping one safe and liquid government liability for another.

The second thing you’ll notice when you look at this set of transactions closely is that this process of netting out of debts doesn’t particularly require a clearinghouse. All you need is an entity which buys additional IOUs from every individual. In turn, each member of the shtetl could use the proceeds of selling IOUs to that entity to pay off their debt to other members of the shtetl. We actually have an entity that does that in our society today- its called a bank. The most basic feature of banking involves the bank creating its own IOU which it swaps for the IOU of households or businesses. This is clearest when we use the example of U.S. banks before the Civil War which simply emitted their own unique banknotes. Hence the phrase “banknote”; they were literally the notes of banks!

Both my bank and I are expanding our balance sheets. The difference is the IOUs that Banks create are widely accepted “as money”, while my IOUs are not. We’ll say more about why that is true in future posts. For now, it’s important to really grasp that this is not money lending. As the famous economist Hyman Minsky said:

Banking is not money lending; to lend, a money lender must have money. The fundamental activity is accepting, that is, guaranteeing that some party is credit worthy. A bank, by accepting a debt instrument, agrees to make specified payments if the debtor will not or cannot.

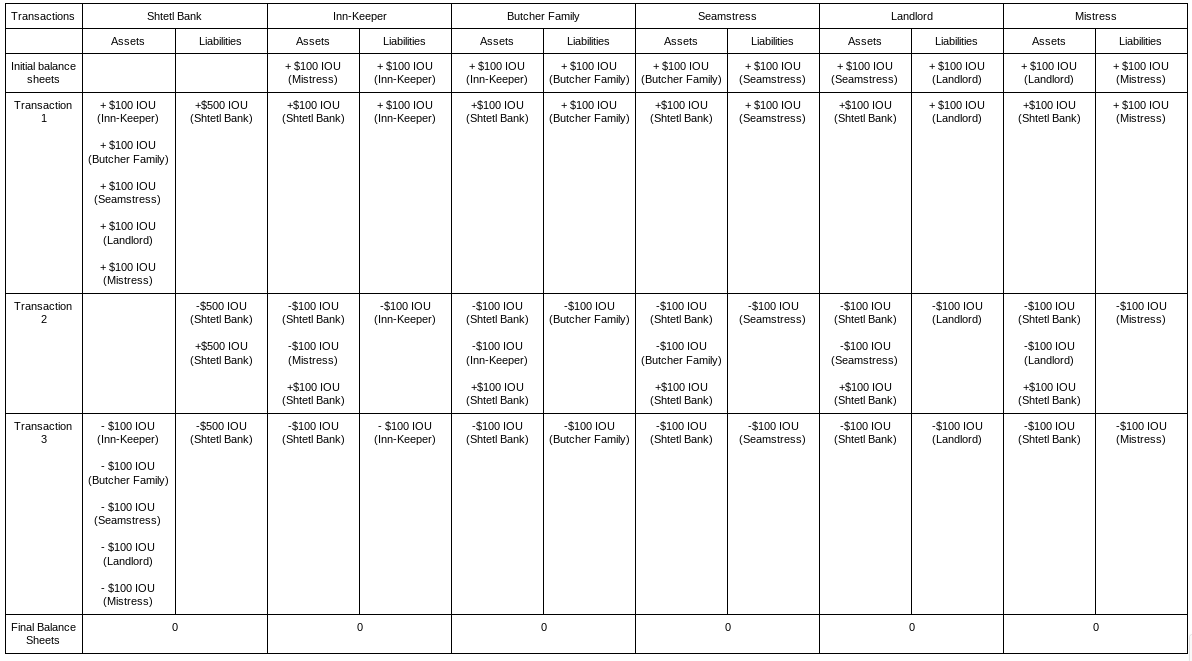

Let’s imagine that instead of a clearinghouse, a wealthy benefactor came in town and set up the shtetl bank. He’s looking to bring “financial inclusion”. He just really thinks what the local community needs is bank lending and payments and he’s going to provide them for the low, low cost of a 10% return on investment every year. If you think about it, this should go similarly as to the clearinghouse- as long as everyone has access to bank loans and are able to clear their debts quickly i.e. without fees, fines or monthly interest payments.

Hey, it worked! Everyone is out of debt, just like in the clearinghouse case. This is the ideal version of banking. Everyone sees their debt monetized, no one is running a deficit or a surplus and no one is in debt by the end of it. The real world, of course, doesn’t remotely work out like this. Yet, it is important to emphasize that with plentiful access to bank credit our payment chains are unquestionably shortened in both size and time from incurrence to repayment. We clear trillions of dollars of payments every day and the surpluses or deficits of each sector are order of magnitudes smaller. By monetizing our debts, banks facilitate making payments between individuals and businesses. Less creditworthy individuals can make sure their IOU trades “at par” (meaning 1 for 1) by supplementing their creditworthiness with collateral worthiness, as we discussed two weeks ago. The interest earned from loans helps banks build buffers of financial net-worth so that they can afford to take losses in case of default.

However, that isn’t sufficient to make sure the bank avoids taking losses and clears payments at par among households and businesses. The dirty secret of par clearing among banks is exclusion. Banks facilitate payments between the vast majority of individuals and businesses through making loans and without taking severe losses by simply excluding a part of the population from loans. For those with full access to banks, their ability to make payments is greatly enhanced by the banking system. For those who don’t, they are greatly hurt. Non-bank credit arrangements required widespread lack of access to bank credit to be used in the numbers required to function as a viable payments system. It is this careful process of exclusion and inclusion which facilitates the smooth functioning bank payments system we see today. The only thing worse than being a dispersed, bilateral set of debt relationships between individuals is to be stuck in those sets of social relationships on the margins of society. The fully “banked” expect prompt payment because they are used to assuming that everyone has access to some way to monetize their debts. The give and take of slow, grinding shtetl payments has completely evaporated.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025