Yet Another Debt Ceiling Crisis! (Or, How Joe Biden should Learn to Stop Worrying and #MintTheCoin.)

.

After the Georgia runoff elections many had high hopes for fiscal policy. But instead, we have hit very rough terrain. President Biden’s whittled down infrastructure spending plans are in critical danger ( weary readers may recall these plans started life as a much more expansive approach to “building back better” and what “infrastructure” meant). As time has draged on, the fights over the Biden administration’s spending agenda have crashed head first into our recurring cycle of debt ceiling crises.

To recap, for obscure reasons in fiscal history, congress has decided to pass appropriations bills which authorized and required spending, while imposing arbitrary limitations on how much debt the treasury can incur in meeting the obligations which congress has imposed on the Treasury. Congress then raises this debt ceiling periodically (or suspends it altogether…). But this is not permitted before making raising it a place for partisan political grandstanding. This spectacle has gotten more serious as partisanship sharpened, and the Republican party became more single-minded in its policy-invariant opposition to Democratic presidents in the 1990s.

This is the most serious debt ceiling crisis yet — today there is not even a pretense of negotiations between the parties. Worse, the Democratic party controls the senate by the thinnest of margins, giving right wing Democrats enormous leverage. Many in Washington see what’s at stake as nothing less than the ability of those in the majority to govern and pass the agenda they were elected to pass — a reasonable perspective, to my mind.

For my purposes, what is sufficient is that either some legal or financial technicality will bypass the obstructions, or the Biden administration's spending agenda will need curtailing — or even to be abandoned altogether. I think that is a high cost to bear, especially since there are alternatives. I’ll leave aside the complicated legislative maneuvers happening now since others are covering these in great detail. As others are focusing on the legal technicalities, I will focus on my specialty: the financial technicalities.

Avoiding the Ceiling Altogether

Before we discuss a certain coin of … ample denomination, it’s worth taking a step back to think of other available options. There are more conventional measures that could have been done to avoid, or at least delay, this eventuality. But how seriously were these being considered?

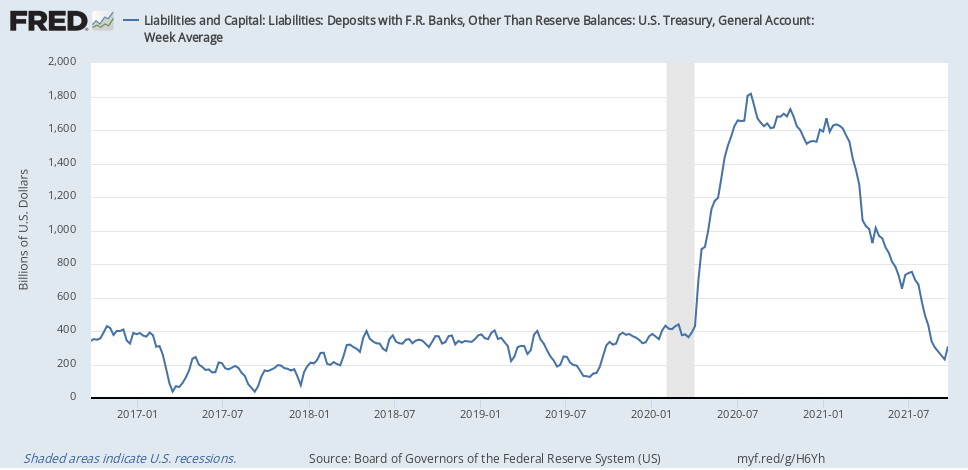

One option is to simply keep the balance in the Treasury General Account (essentially the U.S. Treasury’s “checking” account) at the Federal Reserve very high. In thinking about this, I was very surprised to find that as soon as Janet Yellen became Treasury Secretary, the TGA began precipitously dropping. This is partially understandable: funds from various recently passed legislations presumably began to be dispersed in large quantities. Nonetheless, this could always be offset by more treasury auctions.

Of course, the downside to sustaining the Treasury’s general account at such high levels would normally be that you reach the debt ceiling limit that much sooner. However, this is not the problem it appears at first sight because the debt ceiling no longer works this way. In the last few rounds of debt ceiling fights, congress abandoned simply raising the debt ceiling limit.

Instead, they “suspended” the debt ceiling. That means that if no solution was reached by the time of the suspension’s expiration, the new debt ceiling simply became however many treasury securities were in the hands of “the public”. (The debt ceiling resumed at the end of July 2021, which is why we’re talking about all this now.)

The “extraordinary measures” the Treasury uses to avoid missing payments (whether they be interest payments or social security payments) has carried it this far. But those stopgaps are expected to run out sometime in the next month or so.

Thus, the new structure of temporarily dealing with the debt ceiling obstacle has fundamentally changed how the U.S. Treasury can deal with the situation. Since the debt ceiling, if it should return, will just apply to whatever treasuries are outstanding, the Treasury department could have issued 10 trillion dollars worth of securities. As we’ve talked about at great length, the Federal Reserve ensures that Treasury security issuance doesn’t interfere with its monetary policy objectives. That means there are no concerns over the liquidity of these treasuries, or the overall level of interest rates.

Of course, on a day to day level there would have to be a significantly increased level of coordination between the Treasury and the Federal Reserve, but this would be a difference of degree and not of kind.

I realized as I wrote this piece that this option created by the new legal structure of the debt ceiling has never been properly articulated publicly (at least as far as I’m aware). That is likely a big reason why the general account wasn’t sustained at high levels — or even greatly increased from the “lameduck” Trump era. Still, I do find myself somewhat disappointed that Secretary Yellen didn’t do more to make the resumption of the debt ceiling a politically less painful experience. I can’t help but wonder if her historical deficit hawkishness prevented her considering an option that would have technically meant more debt outstanding sooner.

I’ve discussed this option informally with a number of people in economic policy circles over the last couple of years. I have taken to calling it the “Poor man’s Trillion Dollar Platinum Coin”. While this option is an interesting conceptual exercise, it is a moot point now. The debt ceiling has resumed. The platinum coin however, is a live option.

Which brings us to our big boy, the Platinum Coin.

Yes, #MintTheCoin

Could a trillion dollar platinum coin solve our cycle of constitutional crisis from causing intractable financial chaos? Let’s recap!

I’ve discussed this intriguing technicality in U.S. coinage law at the very beginning of Notes on the Crises. At the time, it served as a kind of “fiscal rhetoric”. A rhetorical tool clear to the public that responding to the Coronavirus Depression was financially feasible.

However, the coin began life as a discovery by an enterprising independent lawyer named Carlos Mucha, who was researching ways to get around Obama’s debt ceiling crisis. Thus, we have swung back around to the “classical” platinum coin debates (and yes, they’ve gone on long enough to have “classical” debates!). It is important to emphasize in the context of these “classical” debates that this is a currently available financing instrument which can be used at any time.

The debt ceiling only caps how much debt can be outstanding and not all liabilities count for that purpose. An obvious example of a liability that doesn’t count would be the Treasury’s obligation to pay social security payments to retirees. Even some currently circulating instruments don’t count under the debt ceiling. For example, the Treasury has the ability to issue its own paper money (called “Treasury Notes”) which does not count under the debt ceiling.

However, paper issuance has its own particular cap of 300 million — an antiquated limit which dates from the 19th century! Coin issuance has no such cap. However, coins are usually statutorily limited in what denomination they can be issued. It would be technically unfeasible (to say the least!) to issue dollar coins in sufficient quantities to cover modern deficit spending.

There is however, one exception. Section 5112(k) of the U.S. Code authorizes the mint and issuance of:

It may seem absurd when you first think of it — but according to this provision the U.S. mint can legally mint platinum coins in denominations of the trillions, or more. So, why not?

My colleague Rohan Grey has written the definitive law review article on its legality and implications. Grey’s piece features an extensive response to all the currently made objections, and likely consequences for the debt ceiling.

Moreover, the Treasury Secretary has not only the option, but the constitutional obligation to use this coinage power. Coinage must be deployed if it stands as the only option available to her for avoiding default — and so it seems to be!

This constitutional obligation is one reason why it is very concerning that the Biden administration has publicly declared that this option is not on the table. The other reason it is concerning is that it means they are willingly ceding leverage to Republicans. What will they give up in order to avoid using the coin option?

Democrats very understandably want to generate a political narrative around Republican intransgenience — and in fairness, there is a lot of intransgenience to point to. However, it is also intransgent to ignore and leave aside these alternative solutions in favor of a political showdown. I also think Democrats overestimate the political benefit they get from highlighting how difficult republicans are making legislating. Potential voters are just as likely to drop out and feel voting is pointless as they are to feel extra motivated to vote and oppose Republicans. Spending, however, can motivate people.

And the best hope for Democrats passing a big spending bill is for accounting gimmicks to be dealt with by accounting gimmicks, rather than lowered expectations. The debt ceiling is an accounting problem, calling out for an accounting solution.

That’s a lot of words to say something simple: Mint the damn coin! And then let’s refocus on the real crises.

Subscribe

Printer Friendly Version

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025