The Secularly Stagnating Arguments of Olivier Blanchard and Larry Summers

.

Subscribe

In my last piece, I spent a lot of time examining the evolution of Paul Krugman’s views on fiscal policy. I found that these had shifted markedly,as a direct result of the coronavirus depression and President Biden’s election. I think his evolving views are important — both because of the significant influence Krugman enjoys personally, and an indicator of how our new conditions will produce new thinking from mainstream economists. One way to emphasize how unusual his evolving views are is comparing them to important contemporaries of his from the economic profession’s elite.

Two men in particular are worth highlighting: Olivier Blanchard and Larry Summers. The reasons for comparing and contrasting Krugman’s recent statements and theirs are two-fold. First, Blanchard and Summers have co-authored a number of pieces in recent years, arguing that the U.S. economy has a tendency towards “secular stagnation”. Second, while both have argued for a greater role of fiscal policy in responding to recessions, both have criticized the Biden administration for pursuing expansionary fiscal policy “too aggressively”.

To start, let’s take the idea of “secular stagnation”. This idea has a very long history. But for our present purposes what’s important is that there is a (nearly) forgotten tradition in mainstream economics emphasizing an array of “long term and structural” forces. These forces are thought to lower “economic growth”, elevate unemployment and, well, cause stagnation. The version of this idea which Larry Summers and Olivier Blanchard have taken up is (unsurprisingly) the version most amenable to being integrated into recent economic thinking. In this version of the secular stagnation thesis, these “structural” forces lead to an economy which can only reach full employment if interest rates are very negative. Since interest rates (allegedly) can’t go negative, we are left to stagnate.

The concept of a “full employment” rate of interest is also known as the “natural rate of interest” (sometimes referred to as the “neutral” rate). In the 2010s that topic was a major focus of my intellectual energies. During the 2020 pandemic however, this idea took a backseat. The Federal Reserve was focused on supporting the economy using credit policy which sets aside, to a certain extent, the obsession with stabilizing the economy with interest rates. Meanwhile, federal fiscal policy took center stage — without the concern about “overheating” which has dominated debates in 2021.

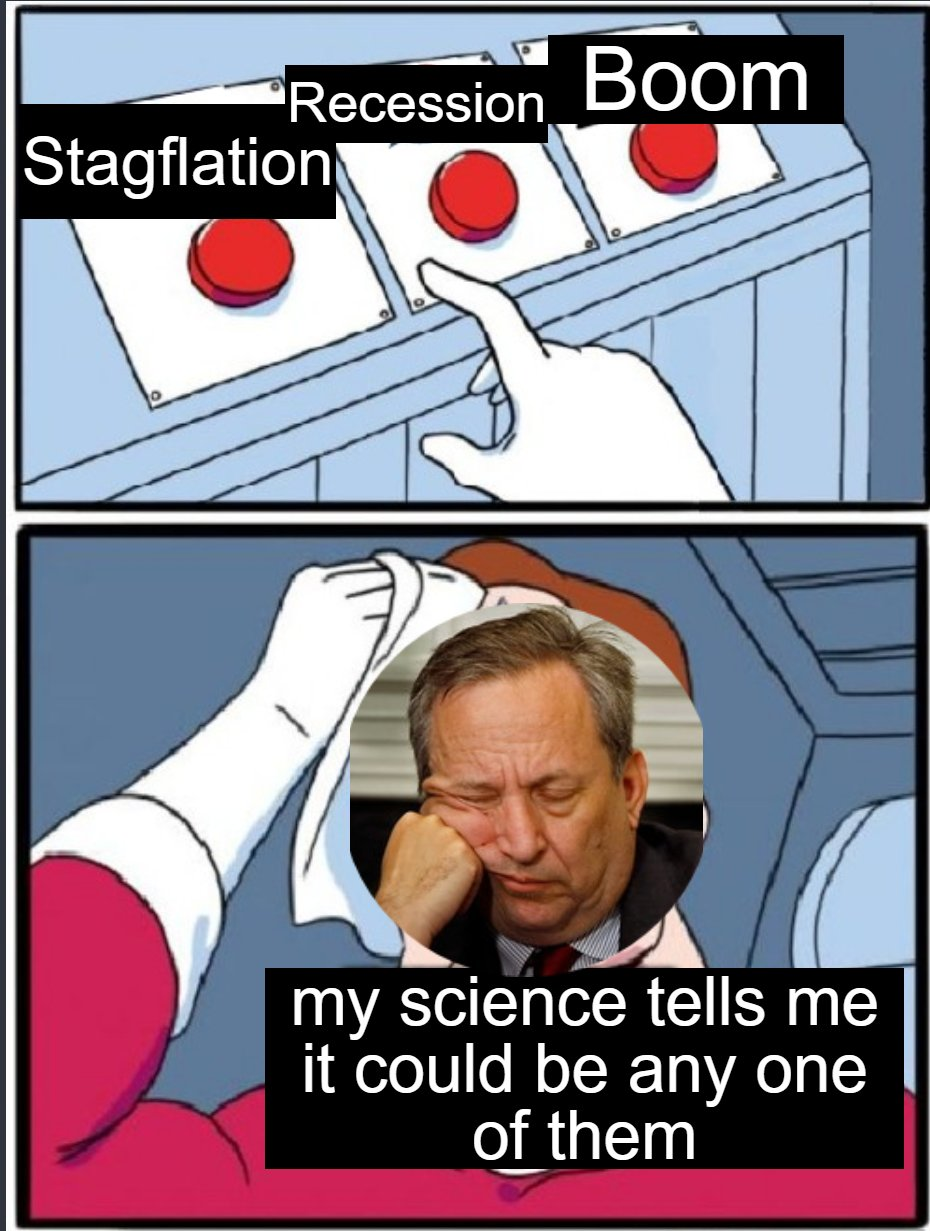

Overheating brings us back to Blanchard and Summers. Take Summers first: it is difficult to nail down his views, as he has been on every side of every issue. Following Biden’s covid relief legislation in March, he infamously predicted that there was a “⅓ chance” of each of the following: a “recession”, “stagflation” and a “boom”. In other words, he predicted everything and nothing. It turns out he has a bad habit of making this style of “⅓ chance prediction” for every major policy issue he’s been asked to comment on in the last 15 years.

A chief focus of his comments for months, which I dealt with in December, has been a focus on the “checks”. This fixation seemed underpinned by the presumption that giving people one time dollops of cash would particularly “overheat” the economy. Last weekend he added to this narrative that there is a “labor shortage” according to a “large number of anecdotes” and that job market “quits” have returned to the pre-coronavirus norm.

Summers predictably attributes a significant amount of this “labor shortage” to unemployment insurance boosts which elevate “income replacement” rates at the low end of the labor market. We can safely ignore this discussion. Show me big wage hikes at the bottom of the labor market, and I will reconsider my view that this “shortage” is an illusion. If not wanting to work for little wages for an employer who isn’t providing adequate protection from a deadly virus is a “shortage”, then I have an egregious “shortage” of people willing to pick up my laundry for one dollar.

Oliver Blanchard’s criticisms of Biden’s fiscal policy have been more measured and precise. I think they are captured by his oxymoronic-yet-clarifying phrase “excessive overheating”. After all, Blanchard has recommended some degree of overheating in the past. Apparently, this package is too much of a good thing. But why?

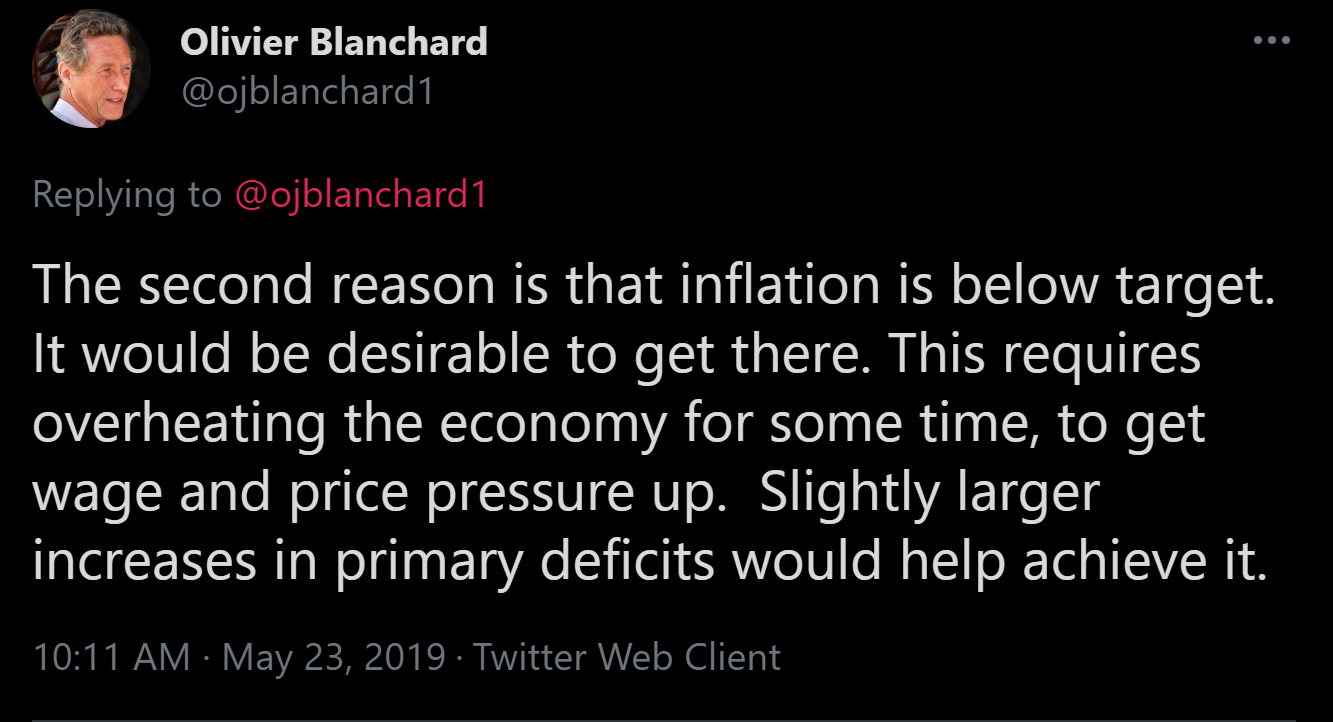

Blanchard does clearly underestimate the persistent economic weakness left over from the Great Financial Crisis. But for the purposes of this discussion I think the key to understanding his view can be found deep in a twitter thread from February.

If it were to happen, it would lead to strong inflation (not the 2.5% that some predict, but potentially much more), and, likely a strong reaction of the Fed to limit the overheating, a very large increase in interest rates, again far more than is currently priced in. Why go there? Why force the Fed to in effect cancel some of the Biden package?

Cancel culture is clearly going too far.

In any case, Blanchard is implicitly acknowledging “Paul Krugman’s” point that the Federal Reserve can effectively offset demand from the Biden package. He is simply presenting what Krugman points to as a positive- — gaining a lot of space to cut interest rates in the future — as a negative. One reason this could be negative could be that the Federal Reserve can’t really “offset” demand pressure from very expansionary fiscal policy. But of course, that is a conundrum for these mainstream economists in good standing because that would suggest the whole idea of a “natural rate of interest” is off base.

More likely, Summers and Blanchard think there are big “costs” to having significantly higher interest rates, even temporarily. This allows them to avoid concerns about interest payments going “to infinity”. In fact, Blanchard’s acclaimed 2019 paper “Public Debt and Low Interest Rates” is a surprisingly predictive guide to these evolutions in Blanchard’s views. For that reason, in a future piece I’m going to examine that article in detail. I don’t think it will surprise readers to know that I don’t think Summers and Blanchard’s current claims will age well.

More pertinently, I think they badly misread the public —as well as the intellectual — mood in ways that will close the door on their future influence. Krugman is staying just ahead of the curve — and he will (as usual) benefit greatly from doing so.

Subscribe

Printer Friendly Version

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025