Can the Aspen Institute’s Elite Economists Beat the Coronavirus Depression?

Analyzing Proposals from Timothy Geithner, Jason Furman and … Glenn Hubbard

Hello Subscribers, I apologize for not posting last week. I had severe back pain which prevented me from working on my laptop. I will be returning to my normal posting schedule this week. I hope that, in lieu of posts last week, readers accept this long deep dive into the Aspen Institute's Economic Strategy Group report on “Promoting Economic Recovery After Covid-19” as a substitute. I worked very hard at it. If you’re a new reader, please consider taking out a paid subscription here.

Between the CARES act, its headline number of 2.2 Trillion dollars (which is inflated) and the extensions to the Payroll Protection Program, as well as its expansions, congress has been pretty self-satisfied with its crisis response. Congress hasn’t even returned from recess to respond to the Floyd Uprisings. The democratic party leadership’s “HEROES Act” is a grab bag meant to perform a political purpose and isn’t meant to become actual passed legislation. To their credit, elite economists within the Democratic Party are nowhere as blaise as their political leadership. As such, there are a variety of proposals circulating the DC think tank world. One in particular I think is worth analyzing: “Promoting Economic Recovery After COVID-19”.

This paper is a product of the Aspen Institute’s “Economic Strategy Group” which is a collection of some of the most influential economists and policymakers the United States has to offer. Take, for example, the signatories from their December 2019 statement. They include the past two Federal Reserve Chairpeople Janet Yellen and Ben Bernanke, Erskine Bowles of the Simpson-Bowles Deficit Reduction Commission under Obama, Austan Goolsbee formerly head of Obama’s Counsel of Economic Advisers, Bush Treasury Secretary Hank Paulson and a handful of CEOs including the heads of Blackrock and Ernst & Young. There are many more so I encourage readers to look through the full list themselves.

Of course, the most relevant figures in assessing this paper are its authors. These figures are very influential in and of themselves. They are Obama’s former Treasury Secretary (and Bush Era President of the New York Federal Reserve) Timothy Geithner, Obama’s “lameduck” Council of Economic Advisers Chairman Jason Furman, George W. Bush Council of Economic Advisers Chairman Glenn Hubbard and University of Maryland professor Melissa Kearney. Kearney is influential as well, having headed up the Brookings Institution’s Hamilton project and serves as director of the Economic Strategy Group, but she hasn’t served in government, isn’t a macroeconomist and as a result I’m going to focus on her coauthors in assessing this report.

This is not the place to profile this trio of male economists but Geithner and Hubbard are infamous. Furman has a lower profile and is largely known for shifting the macroeconomic consensus with his “New View” of Fiscal policy at end of the Obama administration when in its first years he rejected the use of more fiscal policy and advocated focusing on government debt to GDP ratios instead. He has used the perch provided by his “new view” to defend orthodoxy from outside challenges. This collection of well-credentialed and experienced figures is clearly meant to give this report great weight, which I think it does have. Thus, it serves as a great temperature check for what kind of advice democratic leadership and the Biden campaign is getting. It is also a good window into what elite economists are thinking about our current moment- and perhaps the holes or severe failings in their vision. As we’ll see, this report also serves as a barometer, and a solidification, of good policy ideas which have only recently gotten serious attention in mainstream think tank circles.

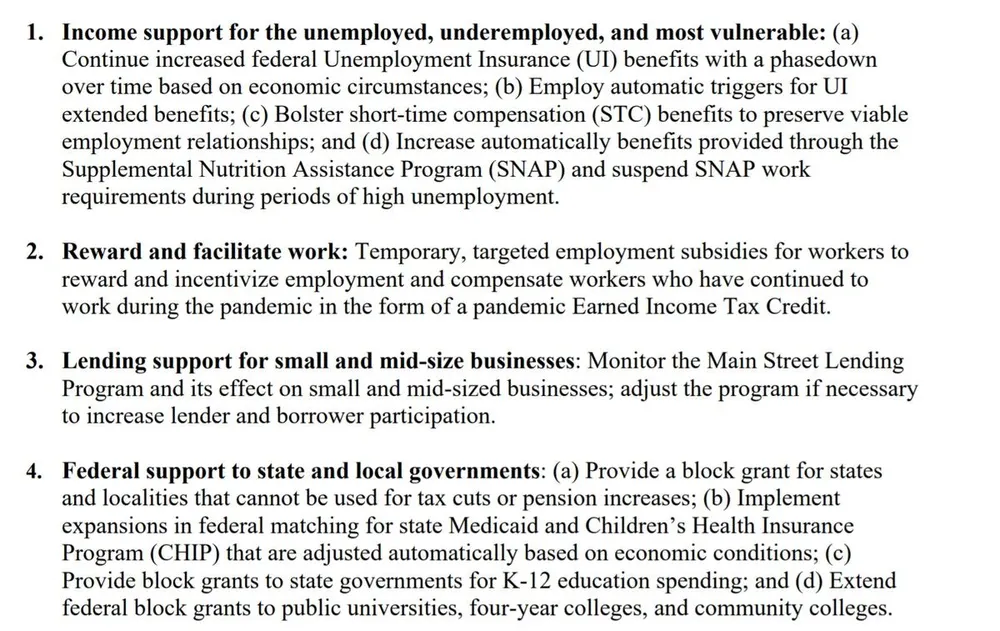

Helpfully, they summarize their main proposals at the beginning of their report:

However, this is a little difficult to look at with its proposals and sub-proposals. I’m going to reorganize it into a 10 point plan:

- Continue increased federal Unemployment Insurance (UI) benefits with a phasedown over time based on economic circumstances

- Employ automatic triggers for UI extended benefits

- Bolster short-time compensation (STC) benefits to preserve viable employment relationships

- Increase automatically benefits provided through the Supplemental Nutrition Assistance Program (SNAP) and suspend SNAP work requirements during periods of high unemployment

- Temporary, targeted employment subsidies for workers to reward and incentivize employment and compensate workers who have continued to work during the pandemic in the form of a pandemic Earned Income Tax Credit

- Monitor the Main Street Lending Program and its effect on small and mid-sized businesses; adjust the program if necessary to increase lender and borrower participation.

- Provide a block grant for states and localities that cannot be used for tax cuts or pension increases

- Implement expansions in federal matching for state Medicaid and Children’s Health Insurance Program (CHIP) that are adjusted automatically based on economic conditions

- Provide block grants to state governments for K-12 education spending

- Extend federal block grants to public universities, four-year colleges, and community colleges.

The Good

To start with, let’s talk about what’s good in this report. My predisposition from seeing the outlet putting it out and people involved is certainly to be very critical so I want to begin by pointing out what is interesting and useful in what they have to say. The first and most obvious good thing in this report is that it proposes embedding triggers in unemployment insurance tied to unemployment rates which would increase the size and length of unemployment benefits in a recession. This is not a proposal that is unique to the authors of this report by any means, but it is useful that they put their stamp of approval on it. Such structures make U.S. fiscal policy more countercyclical without the need for discretionary fiscal policy by congress. Strengthening fiscal countercyclicality has been a longstanding interest of heterodox economists, especially Modern Monetary Theory economists, and the resurgent interest of mainstream economists in this topic for the last few years goes a long way to shifting the conversation. “Flexible formula” fiscal policy to supplement fiscal automatic stabilizers was theoretically popular in the 1950s but have largely been forgotten by mainstream economists until recently. Alex Williams has coined the term “Autonomous Stabilizers” for them which is a term I’ll be adopting to distinguish them from automatic stabilizers.

That said, this proposal is not without its problems. The whole report strangely neglects Claudia Sahm’s pioneering work providing superior measures for triggering autonomous stabilizers. She proposes, in a now famous chapter of the Brookings Institution book “Recession Ready”, that autonomous stabilizers “begin after a 0.50 percentage point increase or more in the three-month moving average of the unemployment rate relative to its low in the prior 12 months”. This ingenious measure accurately and quickly predicts the onset of recessions in all past U.S. recessions without “false positives”. Any program that is designed to begin in a recession and end once the recession recedes must be tied to the “Sahm rule”.

The Furman, Geithner, Hubbard et al. report does not do so. Instead they propose, following a similar proposal in Furman’s paper in the Brookings 2019 book “Recession Ready”, that “the benefit could be triggered when a state’s unemployment rate surpasses its 25th percentile since 1980 plus 2 percentage points”. As Alex Williams said in his excellent recent masters thesis:

The authors use a different stimulus trigger than Sahm: the 25th percentile unemployment rate measured in the state, plus one percentage point. This is a less fluid and adaptable trigger than used by Sahm and used in the present paper, in that it takes longer to adapt to structural changes and may fail to trigger spending on some recessions.

It’s hard not to think that Sahm’s work is not being utilized because of social hierarchies in economic policymaking which is unfortunate as it's strictly superior to the trigger they use.

Their third proposal is also a good proposal: providing additional support to state level short time compensation programs. These programs provide funding for businesses to reduce working hours of their employees rather than laying people off. I haven’t really paid attention to these programs- nor their expansion over the last decade to 26 states- and it is genuinely useful for these economists to highlight these programs. They also helpfully summarize the CARES act funding for STC programs:

Typically, STC benefits are financed through employer payroll taxes administered by states. Under the CARES Act (Section 2108) the federal government reimburses states with STC programs for the entire cost of STC benefits (up to the equivalent of 26 weeks of total unemployment benefits per worker) through the end of 2020. In addition, the act provides federal funding to cover up to half of the cost of new programs that are implemented by states by December 2020 and provides additional grants for implementing new programs. States are able to make individuals receiving STC eligible for the additional $600 FPUC benefit.

Short Time Compensation has been a significant gap in my coronavirus response coverage and if all this report did was generate awareness about these programs and get people thinking about ways to bolster them on the federal level, it would be very useful. They propose administratively simplifying the program and standardizing how they function across states, making its replacement rates match Unemployment Insurance and embedding their subpar (but better than nothing) unemployment trigger. It’s not clear why they don’t simply propose these programs be federalized, an issue we will take up in the next section. Overall though, I think this part of their 10 point program is an unambiguous positive.

Point 7, 9 and 10 I’m going to deal with together as they are very similar programs- providing block grants to sub-federal governments to prevent state and local budget cuts. Their block grants are aimed at general funding, K-12 education funding and higher education funding. I’m very pleasantly surprised that they devoted significant space to these issues as other economic policymakers have neglected the coming local budget cuts, especially to education. My Column for The Appeal was titled “Avoid austerity to prevent a state and local coronavirus depression” and was laser focused on the scale of the response needed to simply prevent state and local budget cuts. By highlighting the programs that will see the biggest cuts, secondary and post-secondary education, they are helping to make state and local austerity a greater focus of federal policymaking.

That said, their proposals are inadequate. The timidity of their proposals can be captured by their approach to part of K-12 funding:

We support additional one-time federal funding for K-12 of about $65 billion, which would aim to offset roughly half of the lost revenue that would be applied to K-12 education among states.

Why not offset all of the lost revenue? They take a similar approach to the block grants for the state’s general budget (while trying to limit pension increases and tax cuts):

A block grant of around $500 billion to be split between states and localities and spread out over two years would, together with our other proposals, fill much of their remaining budget holes, enabling them to avoid draconian spending cuts

While “draconian” cuts are worse than “moderate” or “small” cuts, budget cuts during a depression are nonetheless still bad. I will analyze what I think motivates the inadequacy of these proposals in the next section when discussing their medicaid proposal. The final thing to be said about these block grant proposals is that it is strange that they are not tied to unemployment triggers which are clearly established to be better ways of designing fiscal policy tools with the previous programs. Alex Williams proposal is superior in that it uses the Sahm rule to trigger block grants to state and local governments and ties the size of those block grants to the degree to which the unemployment rate is elevated above some baseline (for details of how this would work, see here). With that, it's time to examine the bad.

The Bad

Before going through each proposal I consider bad, it's worth summarizing what I think is the main problem with them. To summarize, most of the bad proposals are motivated by a desire to “incentivize work” and prevent what they see as “resource misallocation” while shifting focus away from the central problems- the actual pandemic, unemployment, massive shortages of demand and resource planning. As I discussed in my post “What are the Three Concurrent Crises of the Coronavirus Depression?”, there are issues of physical resource allocation but they don’t result from disruptions to the “price mechanism”:

It should be directly physically reallocating resources and organizing production through hiring workers and guaranteeing private producers markets. Resources left unplanned, are predictably unorganized. Private Sector planning works at dealing with medium and long term resource questions but struggles to move quickly and effectively in times of crisis.

Furman, Geithner, Hubbard and Kearney do not appear very concerned with these issues. When they focus on resource allocation, they are worried about the operation of the “price mechanism” and are valorizing how labor and resources would be reallocated absent government intervention by the operation of “normal market processes”.

This perspective clearly guides their 1st, 5th and 6th proposal in their 10 point plan. Their first proposal is to phase out the $600 dollar per week supplementary federal unemployment insurance benefit in favor of higher “replacement rates” in order to incentivize working:

Optimal unemployment insurance requires balancing the desire to help households smooth their consumption against the moral hazard of unemployment insurance discouraging work. The higher the unemployment rate, the more generous the optimal benefits because the constraint on employment is weighted toward the availability of jobs versus the intensity of job searching

Recognizing this tradeoff, we recommend replacing the Federal Pandemic Unemployment Compensation after July 31 with a new system that provides a federal unemployment benefit, in addition to state benefits, of up to 40 percent of covered wages with a maximum federal UI benefit of $400. For workers making up to the median wage this would replace about 80 to 90 percent of their wages when combined with regular state replacement rates. The replacement rate would then decline for workers whose lost wages are above the median. [...]

Some states will be unable to implement a bonus replacement rate system by August, in which case we propose that they could continue using the flat bonus formula through the end of the year, with the bonus set at half of the maximum federal benefit—equal to a maximum of $200 per week. Note, the sooner an extension is passed, the more time states will have to update their systems for the new benefit formula, a problem when the flat $600 benefit was passed in March with essentially no advance preparation time.

I think this proposal is very bad. Because there is no guaranteed public option in employment, the effective minimum wage is zero. Absent a move towards a guaranteed public option, it is up to programs like unemployment insurance to partially set minimum standards in labor markets. It is completely appropriate to set absolute minimum standards in the labor market. In contrast, as I’ll discuss more in a moment, they are clearly motivated by encouraging and subsidizing low wage employment. The flat $600 dollar bonus is one of the best parts of the CARES act and should not be lost. The obvious and easy way for employers to avoid their wage offerings being below unemployment insurance benefits is to… raise their wage offerings. This is a more general issue with orthodox economic policy proposals which mistake employer unwillingness to raise their wage rates with shortages of workers more generally.

This leads to their proposal to directly subsidize low waged employment:

we propose a Pandemic Earned Income Tax Credit (PEITC) that doubles a family’s refundable EITC tax credit, as based on earnings in the 2020 tax year. Basing the pandemic employment subsidy on the existing EITC has the key advantages of achieving income and family structure targeting and being relatively straightforward to administer. It has the disadvantage of being distributed to families as an annual, lump-sum amount. If it were administratively feasible, it would be preferable to supplement the earnings of workers on a higher-frequency basis, based on monthly or quarterly earnings [...] The downside of the PEITC approach is that workers would not receive payments until the following year, so its impact as stimulus would be muted. The benefit would still achieve the goal of rebalancing the financial benefits of work versus receiving unemployment insurance

There is a large debate over the Earned Income Tax credit which is beyond the scope of this article to assess. What I will say is incentivizing people to engage in low income work- even if that incentive is not very effective- without proposing a minimum standard for health and safety regulations is actively dangerous. Proposals like Tlaib’s emergency responder corps are superior because we can directly set the minimum working conditions, pay and benefits with this sort of employment (and it directly responds to social needs created by the pandemic). There is a reason that the top labor demand is not hazard pay but higher OSHA standards. More generally, as I said above, I don’t think incentivizing low wage work is appropriate in general. Employers should meet minimum wage and benefits standards if they want to employ people. If employers are struggling financially because of pandemic related reasons, they should receive direct support- such as my proposal for an emergency basic income to businesses. Subsidies to employers should be direct and overt, rather than indirect and covert.

This leads us to their 6th proposal- expanding and changing the requirements associated with the Federal Reserve’s Main Street Lending Program. Somewhat shockingly, they do not support extending and expanding the Payroll Protection Program. To them, its extension and expansion would lead to the misallocation of resources and subsidize businesses that “should fail”:

The goal of government lending programs during the post-pandemic recovery should be to support firms that could be solvent in the post-pandemic economy, but that need new capital to sustain or reopen operations. In any given time period, there is substantial churn in the economy and many small and mid-sized firms go out of business. The pandemic has also led to a substantial reallocation of economic activity, much of which might be lasting. As a result, it is not economically desirable to try to freeze in place the economy of February 2020 or to give unlimited and indefinite grants to businesses. […]

Support for small and mid-sized businesses should be provided to businesses that would have been successful had they not experienced the negative shock associated with the public health crisis, and that can be successful when economic conditions improve. In addition, they should be loans that could be repaid if the business succeeds, rather than grants. Doing this will not require Congress to appropriate any additional funds at this time, but rather require the Treasury and Federal Reserve to make much more aggressive use of the $454 billion that Congress has already passed for this purpose. We do not propose further extensions to the Paycheck Protection Program or the Employee Retention Credit, which were part of the CARES Act passed in March. As discussed above, these programs helped to preserve employment relationships during the sudden shutdown of economic activity. However, extending these programs into the recovery period would create undesirable distortions during a period of economic reallocation. Therefore, we emphasize policies that support out-of-work individuals during this period and encourage continued lending support for small and mid-sized businesses that will continue to be viable going forward

The problems with their arguments are manifold. How can we know which businesses can be successful post-coronavirus or which businesses would have been successful absent coronavirus? They do not provide a criteria for assessing this but the implication seems to be that some measure of the riskiness of current loans can capture this. In their proposal, the Federal Reserve should lower its underwriting standards and accept much higher loan loss rates, but these should still be loans and not grants or quasi-grants. The idea that those with the most flexible and softest financial constraints are the most efficient ones is powerful and dominant within economic policymaking, but it isn’t necessarily the case. In this case however, this logic is even more strained because we have no way of judging which consumption shifts are permanent and which aren’t. Restaurants may see a permanent downturn in business. On the other hand, they may see a boom as people satisfy their unmet need for social interaction on a previously unheard of scale. The idea that we should be explicitly designing policies to lead to mass business failure in a pandemic induced depression because some portion of those businesses may not be a good use of our economic resources is absurd on its face.

Their proposal also underemphasizes the current problems with the program which seem to not be taken up by banks at all. They say in an aside that the program should be made increasingly attractive to both borrowers and bankers to increase program reach and utilization but do not focus on this point, which is very important.

I was happy to hear about the #MSLP initiative by the @federalreserve as part of the CARES Act - money that could help businesses weather these uncertain times.

— Matt Valeo (@Phenomaly) June 16, 2020

It was announced 3 months ago though and keep getting changed before even going live. /1

I also tried @BankoftheWest and @Chase and a few others.

— Matt Valeo (@Phenomaly) June 16, 2020

Same result. Never heard of it.

So after spending a full day doing exactly what @BostonFed says to do, I decided to email them to ask for help finding a "participating lender"

Their response? /12

"We have no plans to publish a list of eligible lenders. We encourage you to contact other financial institutions that plan to participate"

— Matt Valeo (@Phenomaly) June 16, 2020

Sigh

Fin /13

As I’ve said in the past, banks are very bad credit intermediaries. The incentives that they will need to participate, as well as borrowers, may be beyond the scope of what the Federal Reserve is willing to do and even if they do, it may begin to approach a poor version of the Payroll Protection Program. Grants are greatly superior in this respect and if people are obsessed with “private demand” taking over the resource allocation process, that can be accomplished by phasing out the grants when employment and incomes have recovered.

Their neglect of preserving businesses and the current institutional structure which coordinates production may be the most dangerous part of this proposal. Things will be lost that can never be regained, or will take many years to regain. The untested Main Street Lending Program is being asked to accomplish far too much in their proposal as they are essentially being assigned the role to find the “optimal level” of business failure. Their proposals along these lines are also very inconsistent with their subsidies for low income employment. They want to allow the “resource reallocation” process to work but they’re worried that resources will be “reallocated” away from low wage employment and that these employers will lose bargaining power. While I have been an outspoken supporter of putting businesses into a financial “coma” for the duration of the pandemic depression, the one element of their direct household support centric approach that I could potentially like is losing employers with low wage, benefit and working condition standards. Yet, they explicitly make additional proposals to neutralize this one benefit.

This leads me to the 8th point, their proposal to increase the Federal share of Medicaid and CHIP (the children health care program) during recessions. On its face, this may seem similar to the imperfect but good block grant proposals I discussed earlier, however I think this proposal is bad for certain key reasons. First though, the proposal:

We endorse the Hamilton Project proposal by Fiedler, Furman, and Powell (2019) to increase automatically the federal share of expenditures on Medicaid and CHIP during recessions. Specifically, Federal Medical Assistance Percentage (FMAP) in both programs would increase by 4.8 percentage points for every point increase in the state’s unemployment rate above a certain threshold, with a cap at a 90 percent reimbursement rate.5 Although FMAPs vary across states, the average rate for Medicaid in fiscal year 2020 (before the passage of the Families First Coronavirus Response Act) was roughly 60 percent, while for CHIP it was around 80 percent.

Again, Alex Williams is worth quoting, this time on his direct criticism of this proposal:

However, the Medicaid and Children’s Health Insurance Program matching grant proposal (Medicaid proposal) in Recession Ready is at best a very partial solution [...] The explicit goal of the proposal is to provide cover for 2/3 of the gap in spending within one program that accounts for roughly twenty percent of state budgets, rather than to provide general macroeconomic stabilization. This reluctance to commit to substantial spending to support aggregate demand in a downturn is evidence of reliance on a model that predicts substantial costs to an expansion of the federal debt through a crowding-out mechanism. This finance anxiety shows up in the Medicaid proposal as a demand cost of $.033 per every additional dollar of federal debt. As will be shown below, this figure comes from reliance on a failed macroeconomic framework, and our proposal supports much larger spending on the basis of a realistic account of the behavior of federal-level debt. [...]

Lastly, the Medicaid proposal requires that there be no significant other changes in the mechanisms of the healthcare system in the US in order to continue functioning as an effective automatic stabilizer, even on its own small scale. Recent proposals for a “Medicare For All” would invalidate much of the background administrative structures underlying the Medicaid proposal, and it is far from clear that the same multi-level financing would obtain under a Medicare For All regime. Additionally, credibility issues arise due to the complexity of the proposals involved as it may be hard for states to predict the scale of stabilization payments. Most crucially, the program suffers from timidity. It ends up being a part of a solution to a well-identified problem in an environment where more complete solutions can easily be developed.

Alex’s comments echo one of my earliest posts, which argued that “Medicare for All is a Great Automatic Fiscal Stabilizer”. Given the extensive criticisms of Medicare for All by economists, it would be worth acknowledging that that proposal would be superior to other proposals in increasing the countercyclicality of government budgets. Even without considerations of Medicare for All, the temporary federalization of health care spending and coverage for unemployed workers during deep recessions should be a serious proposal that economists comment on, especially during pandemics. Their block grant proposals move the conversation forward much more than this very weak healthcare funding proposal which was already proposed before the pandemic. Economists must do a much more serious rethinking of their defenses of multi-payer healthcare systems and should be forced to acknowledge that the left wing proposals they have derided have superior macroeconomic properties along the lines they are already pursuing. This leads us to the ugly parts of their report.

The Ugly

One of the glaring omissions in the report is a comprehensive approach to our healthcare problems. As discussed above, they propose increasing federal funding for medicaid and CHIP but otherwise neglect taking a comprehensive approach to healthcare financing which could significantly speed up the response to the crisis- and thus shorten the shutdowns, in addition to having the macroeconomic properties we discussed above. They dismiss the topic with a one paragraph reference to “other proposals”:

The highest priority remains the effective handling of the reopening and legislators should provide whatever funding is needed for the health response, including funding for testing, personal protective equipment and other medical supplies, and support for the development, manufacturing, and distribution of treatments and vaccines. Such spending has potentially enormous returns in lives saved and in accelerating the return of economic activity to normal levels. Many other experts and groups are working on these issues, so we do not make any specific proposals on these topics in this report.

As I discuss above, healthcare financing reform is a key place where we can strengthen our automatic fiscal stabilizers. Their neglect of this issue is telling and it is hard not to see it as related to who participates in the “Economic Strategy Group” which counts among its members a CEO of a Blue Cross Blue Shield state hospital network. Whenever these sorts of establishment economists approach the issue of healthcare, the grains of salt that you take their arguments with must become a mound.

The other ugly thing in this report is the proposal to “suspend” work requirements for SNAP- i.e. food stamps. This is not an original proposal to the authors here- it was proposed in a chapter of the Brookings book “Recession Ready”- but it turns my stomach every time I see it. Work requirements to get basic access to a minimal amount of food is gross. This kind of policy decision making has no place in a remotely ethical society. The logic of suspending work requirements- that they are punitive because people are unemployed because they can’t find an adequate job not because of “laziness” or other such reasoning- applies all the time. A 4% unemployment rate doesn’t mean that there’s an adequate job available for anyone who wants it. Meanwhile, a 4% overall unemployment rate means a recession level unemployment level in the Black community. Work requirements do not work and disrupt the functioning of these programs as automatic fiscal stabilizers- and this remains true whether they keep work requirements outside of recessions or not.

Not only should food stamps not have work requirements- I do not think they should be means tested at all. The income benefit to upper income people is extremely minimal- even if they accessed the program which is doubtful. Meanwhile making this program openly available to everyone would greatly reduce the stigma associated with it and ensure that all who needed the program accessed it. This would also ensure that the program served its automatic fiscal stabilizer role, just as medicare for all and full federal financing of government programs more generally would as well. It is the peak of liberal instincts to gutless half-measures that suspending work requirements in recessions is a dominant policy proposal among establishment think tank analysts but simply eliminating them all together is not.

Conclusion

This report has more good features than I thought it would, but it also has many glaring holes which make it dangerous as a roadmap to economic recovery from the Coronavirus Depression. Their argument for moving away from payroll protection is weak and especially dangerous and their healthcare financing proposals are especially weak. What is good in this report is done better by others- with the exception of the Short Time Compensation proposal- especially around more comprehensively strengthening our automatic and autonomous stabilizers. Alex Williams and Claudia Sahm’s work is especially important to read. Claudia Sahm’s original proposal was for recession triggered cash payments to households and they neglect this issue all together. As I’ve discussed, I’m a strong supporter of emergency payments to households and think it's important to do as financial constraints are the biggest problem that households face when confronting a sudden depression. If I had to take one major element of the report and discard the rest, it would be a comprehensive set of block grants to state and local governments, particularly focused on education at all levels. To think through how to more fundamentally make government budgets sufficiently countercyclical and mobilize physical resources to respond to the emergency, readers will have to look elsewhere. It is certainly not the comprehensive fiscal agenda to promote recovery that they bill it as.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025