Paul Krugman Has Changed His Tune About Our “Long Run Budget Problem"

.

Functional Finance Has Apparently Gotten A Lot More Functional

Subscribe

Dear Subscribers: For those that don’t know, I have left Substack and have moved my newsletter to the non-profit platform Ghost. You can read why here. I apologize for the necessary hiatus this process has required. However, now my new website is up and looking better than ever. For my readers there shouldn’t be any difference except that now you login to Ghost (Check my “Migration from Substack FAQ” for more answers to your questions). Comments will be back sometime in May. Having a website that is fully my own also means that I will be able to bring more exciting features, sooner than expected (such as a podcast). Also stay tuned for exciting pieces coming up including: “Why Bitcoin is Not a Bubble”, “What The Hell is an ‘Overheating’ Economy? An Origin Story”, my inflation 101 series, and more! Thank you for bearing with me during this migration, and let me know if you have any issues.

2021 is the year of fiscal policy. The 1.9 Trillion dollar package that Biden just signed into law in the second week of March has barely been processed by budgetary experts. Yet we’re already stuck into a protracted debate about long term infrastructure spending. One of the interesting things to me about the debates “we’re” (meaning economics twitter and economist pundits) having over fiscal policy is that, as frustrating as they are, they are about inflation. The old conversations about fiscal crises may still be discussed in the White House and in corners of the popular press…. But that hasn’t been what economists have been debating about in public. The policy details of these proposals matter, but today I want to take a broader look. Let’s focus on how these rhetorical stars have aligned.

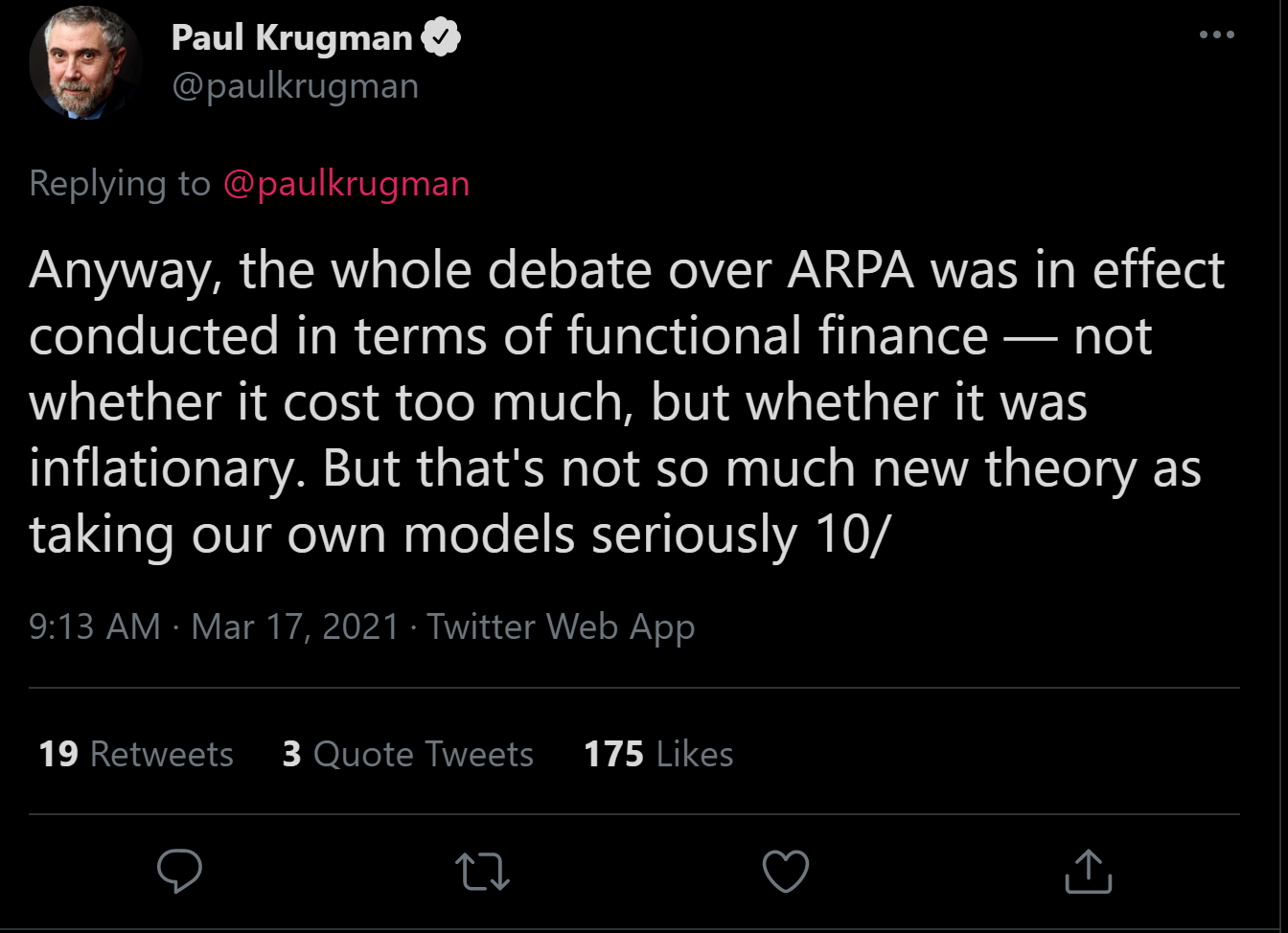

I’m not the only one who noticed the growing mismatch between what economists are discussing, and wider audiences. Paul Krugman said on twitter that “Anyway, the whole debate over ARPA was in effect conducted in terms of functional finance — not whether it cost too much, but whether it was inflationary”.

Paul Krugman is, of course, an important bellwether for how these policy debates are going more broadly. Professor Krugman’s elocutions tend to come slightly ahead — or slightly after — changes in the “club” of economic policymaking . He also tends to be persistent. As I write more about fiscal policy and inflation in the coming years, his work will become more relevant to my commentary. Krugman usually doesn’t have much to say about financial regulation, or the technical details of central banking as these are not “his areas”. The rare exceptions come when it's time to notice that a financial crisis has happened, and staple some insights from Hyman Minsky’s “Financial Instability Hypothesis” onto a mainstream general equilibrium model.

As a result, Krugman has not previously been much of a figure in Notes on the Crises. However, he’s undeniably an important touchstone in discussions of macroeconomics more broadly. Now that the most acute phases of the crisis have passed, the more “conventional” aspects of fiscal and monetary policy have regained their importance. He’s also probably the best writer among living mainstream economists — I’ve learned a lot about both economics and economics writing from reading him, for over a decade. This makes his pronouncements some of the most important economics rhetoric out there. I’m not the only one who sees Krugman’s intellectual trajectory coming into focus in 2021 — though I’m likely one of the most critical.

It is in this context that Krugman’s recent writing has been fascinating to me. In it, he seems to have taken some subtle, yet obvious, turns towards ideas coming from MMT scholars. Take the quote I cite above for example: functional finance is a core element of Modern Monetary Theory (though not the only element). Both that quote and other recent commentary from Professor Krugman suggest that economic debates should always happen on these terms. Yet, before the Coronavirus Crisis Krugman was adamant that functional finance didn’t make much of a difference, and was also a bad guide to fiscal policy-making in general. His most definitive pre-covid argument against functional finance appeared in February 2019, entitled “What’s Wrong With Functional Finance? (Wonkish)”. He throws out a number of arguments in this piece, but the core is this paragraph:

What about debt? A lot depends on whether the interest rate is higher or lower than the economy’s sustainable growth rate. If r<g, which is true now and has mostly been true in the past, the level of debt really isn’t too much of an issue. But if r>g you do have the possibility of a debt snowball: the higher the ratio of debt to GDP the faster, other things equal, that ratio will grow. And debt can’t go to infinity – it can’t exceed total wealth, and in fact as debt gets ever higher people will demand ever-increasing returns to hold it. So at some point the government would be forced to run large enough primary (non-interest) surpluses to limit debt growth.

Let’s unpack this. First, in this context “r” stands for the average interest rate on government debt. “g” in turn stands for the growth rate of “Gross Domestic Product” or “GDP”. Often in this context people speak of the “real interest rate” and “real GDP growth”. But since we’re comparing these two variables, it doesn’t matter whether we divide them by a price index or not. Thus, what Krugman is saying is that in a world where the average nominal interest rate on government debt was always above the growth rate of total nominal incomes, government interest payments would always become a greater and greater percentage of overall GDP. That is, in the language of mainstream economists, “unsustainable”— and thus (presumably) invalid policy.

The central problem is this: why would we assume a short term rise in interest rates would change this long term pattern of “r<g”? The only recent era where nominal interest rates stood above GDP growth was the Reagan era (famously because of Paul Volcker.) And interest rates have been moving down from that high plateau ever since. The critical conflation 2019 Krugman makes — the “Calvinball” if you will — is presenting a short term rise in interest rates as equivalent to interest rates being persistently high for literally infinity. (Remember that nothing goes to “infinity” over a finite period of time).

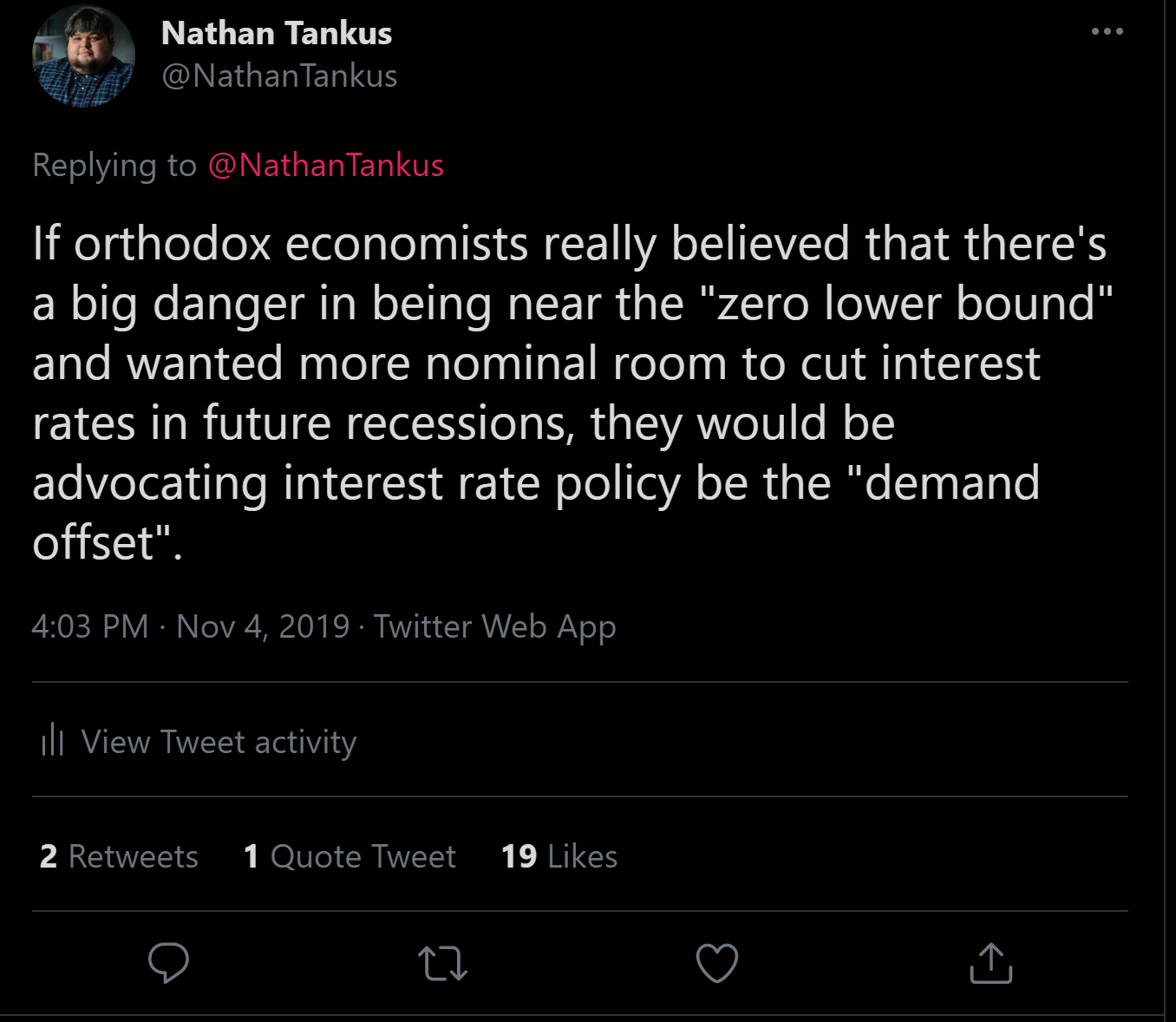

Interest rates may rise now, but that doesn’t mean that interest rates will stay above the growth rate of the economy forever. In fact, if you believed that the main problem with relying on monetary policy to manage the economy is the “zero lower bound” — as

many mainstream economists profess — then it follows you should advocate an expansionary fiscal policy “offset” by monetary policy. I made this point at the time:

Which brings us to today. After the Coronavirus Depression and in our “new era”, Professor Krugman has discovered that his central objection to “Functional Finance” doesn’t really apply. He has now begun making the points I just made. In a recent article on Biden’s forthcoming infrastructure plan (“How (not) to pay for building back better”) Krugman explicitly makes the case for “not paying for it”. This piece is also worth quoting at length, simply because of how profoundly it reverses the logic of his earlier critique of functional finance:

OK, you may say, that’s what happens when you keep running deficits: you end up with more debt, which means more interest, which means more debt, and the whole thing snowballs. Right?

Actually, no. CBO’s big projected interest bill doesn’t have a lot to do with higher debt; it’s mainly driven by the assumption that the average interest rate the federal government pays on its debts will rise dramatically [...]

even if there’s a short-term boom as the pandemic subsides and money from the American Rescue Plan flows into the economy, we’ll probably be back in secular stagnation — where it takes very low interest rates to achieve full employment, even in good times, and the Fed lacks the ammunition to respond in bad times — after a year or two.

And those two implications make the case for a sustained program of public investment that isn’t paid for, that’s deficit-financed. Such a program would do double duty: We need the infrastructure, and it would also provide continuing stimulus in an economy that needs such stimulus, giving the Fed room to respond when adverse shocks hit.”

And because interest rates would stay low, the debt service from such a program isn’t likely to pose a problem.

Evidently the “debt snowball” from 2019 melted into air over the past two years. Now Krugman is telling us we don’t have to worry about rising interest rates. And even if interest rates increase, they won’t persistently stay above GDP growth. This is, of course, a point that MMT economists have made for years and years, while Professor Krugman was writing about our “long term deficit problem”. It is particularly notable because a friend of MMT and professional colleague of Krugman’s, James Galbraith, made this exact point in a critical policy note — that is now just over a decade old. “Is the Federal Debt Unsustainable?” runs through the exact same issues with the CBO’s forecast. Galbraith comes to the same conclusion (albeit more firmly):

The CBO’s assumption, which is that the United States must offer a real interest rate on the public debt higher than the real growth rate, by itself creates an unsustainability that is not otherwise there. It also goes against economic logic and is belied by history. Changing that one assumption completely alters the long-term dynamic of the public debt. By the terms of the CBO’s own model, a low interest rate erases the notion that the US debt-to-GDP ratio is on an “unsustainable path.” The prudent policy conclusion is: keep the projected interest rate down. Otherwise, stay cool. There is no need for radical reductions in future spending plans, or for cuts in Social Security or Medicare benefits, to achieve this. Do not change the expected primary deficit abruptly. Let the economy recover through time, and do not worry if the debt-to-GDP ratio rises for a while

Of course, if policymakers repeatedly launched large spending programs without considering the economic effects, the Federal Reserve may raise interest rates continually. Under this extreme and unlikely scenario- which functional finance by definition advocates against- interest rates may break from their century long historical pattern. It is in this world- and only in this world- where you really have to worry about continually growing interest payments relative to GDP. Even in this extreme world however, there is an obvious alternative. Monetary policy could instead rely on non-interest rate monetary policy tools to regulate demand. As some readers will know, this is a big subject of my own research. Financial regulation is a potent monetary policy tool and there are plenty of reasons to think that it would be more effective at curbing demand growth. Remember, the “big” problem in this extreme scenario is the average interest rate on government debt. That problem is easily solvable, since interest rates on government debt are a policy variable.

Contra-2019 Krugman, functional finance doesn’t ever lead to the feared “snowball”. On the more pessimistic side of things, taking functional finance seriously means recognizing that some taxes (such as those targeting the rich) take in a lot more revenue than they do reduce demand. If Krugman thinks we’ve been mostly debating in terms of functional finance and that that is now a good thing, he should be taking the project of redesigning our budgetary institutions to reflect that more seriously. And that goes for the policymakers he influences, too. But that’s a story for another time.

Subscribe

Printer Friendly Version

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025