The Inflation Reduction Act, Employ America and Oil & Gas. Now What?

At the end of July, a few hours after I wrote about Employ America’s Oil and Gas proposal, the Biden administration implemented a modified form of their proposal. To briefly summarize, the Biden administration committed to further emptying the Strategic Petroleum Reserve. At the same time, they committed to buying oil over the next few years, at specified minimum prices. Depending on your point of view, the timing of my piece was either perfect or extremely bad. The very next day the world was caught off guard by a surprise deal between Senate Majority Leader Chuck Schumer, and habitual enfant terrible Joe Manchin.

Schumer and Manchin’s fiscal deal, amusingly named the “Inflation Reduction Act”, is far smaller than the original Build Back Better proposal. It is also much smaller than the cut down proposals people tried to get Manchin to accede to. But it is still something, and better than nothing. It also has a number of climate provisions, but also Oil and Gas provisions. A colleague of mine described it as a “quarter of a loaf” — and I am still deciding whether I would even be that generous. Nonetheless, it is something at a time when it seemed like there might not be any further fiscal action at all.

Ever since both announcements came down I have been trying to formulate what I think about both issues. In particular, I have a strong sense that these are deeply related topics. My issues with both Employ America’s proposal and the Inflation Reduction Act are deeply intertwined, but it has been difficult to articulate. At their core, both policy shifts indicate an emerging approach to climate change that emphasizes growing both the fossil fuel and renewable energy industries in the near term, and crucially only phasing out fossil fuel production when it is convenient. This is a policy which involves no disruptions which will need to be managed. In this view, emissions are purely “induced” by the demand for goods and services. They don’t involve particular production choices by fossil fuel businesses themselves.

Before diving into my problems with this perspective, I want to speak to one type of criticism I got from readers after my EA piece. I have many, many readers who are interested in my financial markets analysis, and maybe even some of my macroeconomic analysis but who think I should stay out of topics like climate change. That will not be happening.

Ultimately, the only reason to be interested in macroeconomics is to want to contribute to policy which will improve people’s lives at a systematic level and accomplish important societal goals. No goal is more important than responding to climate change today. My monetary policy report from earlier this year is in large part about using direct credit regulation as part of a macroeconomic strategy for dealing with climate change.

As a result, I can’t “stay neutral” on these topics. I have developed my own view of Climate Change, and the very substantial body of empirical evidence and expert opinion among scientists and energy specialists so that I can provide useful and accurate macroeconomic analysis. This doesn’t mean I won’t continue to write about granular financial market issues (as the Monetary Policy report itself demonstrates). But just as I’ve commented on the coronavirus pandemic with an eye to the actual public health situation, I will now do the same with climate change.

I will also say that ignoring issues of climate change would also make my analysis of monetary policy and financial regulation less accurate over time. I can attest from my experience attending the Journal of Financial Regulation conference two weeks ago that climate change is very much a contemporary part of the monetary policy conversation, and will not be going away any time soon.

With that out of the way, let’s return to the issue at hand. The core idea of the Inflation Reduction Act is pairing a series of tax credits for renewable energy, battery storage and so on with approvals for fossil fuel infrastructure, and mandatory auctioning of oil and gas drilling leases on federal lands. Now at one level, this is merely what they needed to agree to to get Senator Manchin on board. Or more accurately, this is what Manchin proposed, and what Democratic party leadership agreed to more or less sign on the dotted line.

At another level though, I think this bill also represents some intellectual shifts on climate change in Washington DC. Over a decade ago, climate change policy was defined by proposals to “price carbon” (under strong influence by orthodox economists), and more general restrictions on fossil fuel development. It was seen as an area where, more or less, you either “do climate policy” by “giving in” to climate change advocates — or you don't. There were problems with this perspective, as I discussed in some detail in my original piece about Employ America. And it’s thankfully no longer the limit to these discussions. In response to the failures of the climate movement during the Obama years—and in the upheaval of the Trump administration—different policy ideas surrounding climate change emerged. Tying climate change to true full employment policies (particularly at the low end of the labor market) and transformative spending projects, rather than carbon pricing gained credence. The idea of a “Green New Deal” encapsulated many of these emerging intellectual trends.

The Inflation Reduction Act, in a bizarre and unintended way, shares this intellectual lineage even if it's a fraction of the proposed green spending. It focuses on transformative spending tax credits rather than schemes to “put a price on carbon”. However, it also goes beyond that. Rather than simply “not pricing carbon” or directly restricting fossil fuel development, it ties these spending projects to supporting fossil fuel projects. In the context of looming bottlenecks and high energy prices, part of the “inflation reduction” plan today is clearly to boost fossil fuel production. The Biden Administration’s implementation of Employ America’s proposal signals to me that these elements are not merely “concessions”. They are part of an intellectual trend that has extrapolated from the deemphasis of carbon pricing to a broader worldview. One where currently stable fossil fuel prices—without pursuing things that will reduce energy demand—is the most important priority.

When challenged by climate activists, scientists and specialists who recognize the obvious need to phase out fossil fuel production as quickly as possible, advocates of this worldview give one of two answers.The first foregrounds the previously mentioned issue that this was “the best that can be gotten”. This claim, while hard to argue with, is missing some key points. For one thing, now that the legislation is passed there is nothing stopping the Biden administration from doing everything it can possibly do to discourage energy consumption (besides selective arguments about electoral success) Second, settling for a “compromise” does not mean you have to gild the proverbial lily, and make it out as something better than it is.

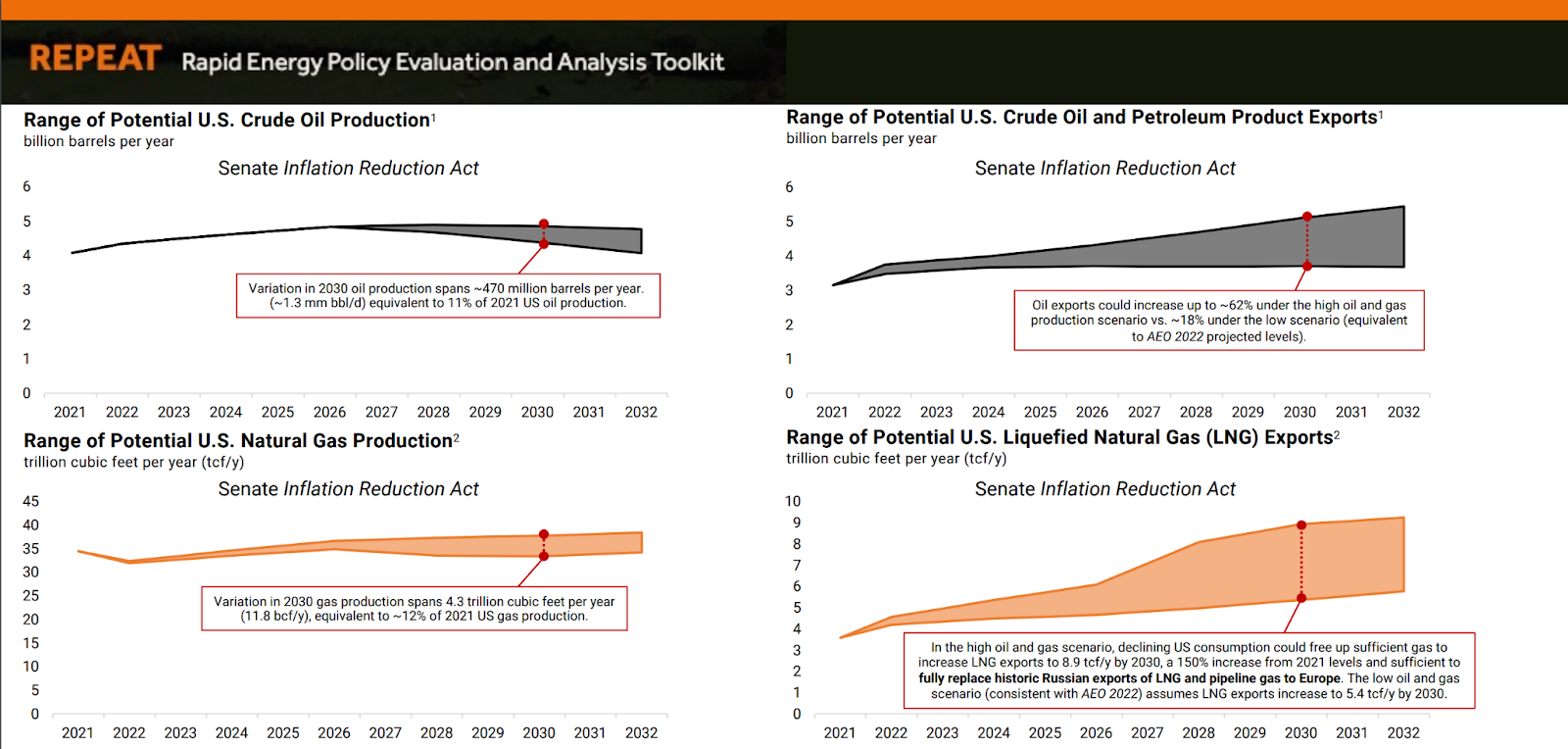

The second response dismisses concerns about increased fossil fuel production. This argument points to projections of significant emission reductions relative to the “no Inflation Reduction Act” status quo. Petroleum and Gas production is projected to fall by 13% and 8% respectively by 2030 according to the REPEAT Project, one of the major modelers of the energy and emission consequences of different U.S. legislation. As the researchers behind this project will tell you themselves, there is considerable uncertainty built into their projections. These are also relatively small projected cuts. The REPEAT project does a good job of pointing out that variations in U.S. oil and gas production will largely be determined by variations in the rest of the world’s demand for U.S. energy.

Under their “high” Oil and Gas scenario, U.S. Oil and Gas production is not all that different a decade from now. This is in large part because of a large run up in oil and gas exports. Their estimate of the additional emissions as a result of this production does not count the emissions from using these fossil fuels. As such, it is at least partially an undercount of emissions (depending on how you want to think about the demand for fossil fuels). It’s worth pointing out that the U.S. had a longstanding ban on exporting crude oil from 1975 to 2015 that was lifted in December 2015 (just days after the Paris Agreement on Climate was signed…)

Reinstating that ban while the Ukraine crisis continues is likely not a good idea. However, we shouldn’t treat these export-based emissions as natural and inevitable over the long term when they are a result of a remarkably recent policy change. It's hard not to look at these numbers and think that U.S. policy is aimed at continuing to be a fossil fuel exporting power house to the 2040s and beyond. The logic of using the U.S. Treasury to stabilize energy markets leads seamlessly to the U.S. becoming an even greater fossil fuel exporter (and it's already number two). Not burning the fossil fuels we produce is starting to be rhetorically reframed as purely the problem of those who import them. Of course, market conditions can shift rapidly. Fossil fuel prices collapsed in 2020. We are only at the beginning of a decade of intense instability. Conditions could still easily shift rapidly against U.S. fossil fuel exports. However, just as the 2014-2015 fossil fuel bust was not an intentional goal of policy, we shouldn’t credit any future fossil fuel busts to the policy suites that are now easing constraints on fossil fuel production.

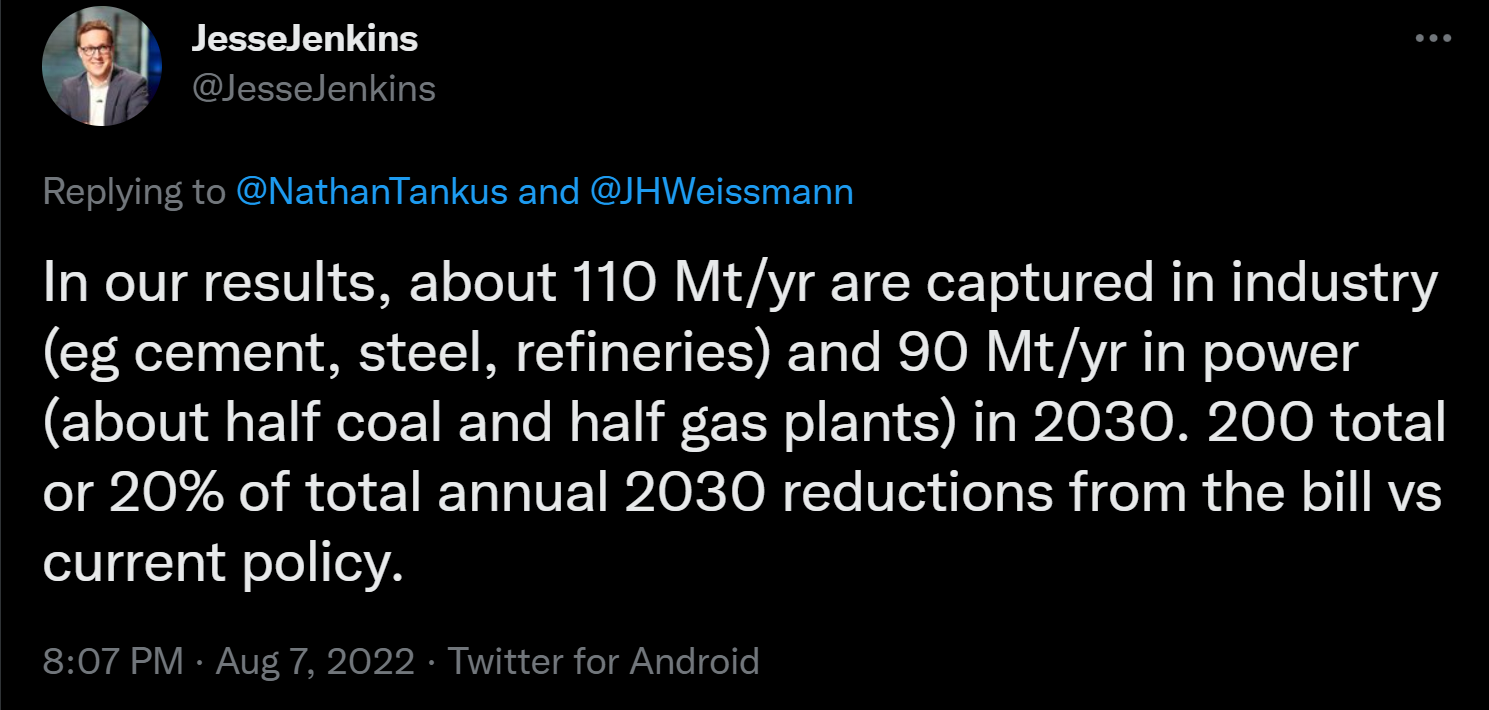

It is well beyond the scope of this piece to provide a full assessment of the climate implications of the Inflation Reduction Act. Others are after all better suited to that task. However, I do want to comment on one further element I found troubling in looking at the REPEAT Project’s forecasts. A significant percentage of their forecasted emission reductions come from “carbon capture and storage”. Professor Jenkins, who heads the project, confirmed for me on twitter that 20% of the forecasted emission reductions comes from a rapid scaling up of still nascent CCS technologies. As professor Charles Harvey and his industrialist coauthor Kurt House pointed out just today in the New York Times, more than 90% of the commercial CCS projects in the United States are capturing carbon dioxide in order to inject it into the ground and “enhance oil recovery”. This makes CCS tax credits to fossil fuel producers, especially Oil and Gas, another fossil fuel subsidy.

Professor Jenkins is quick to point out that if carbon capture in electricity generation does not scale up, this does not mean that all those emissions gains are lost. That’s quite correct: instead, this may simply mean that wind and solar power expands even more than in his forecasts. Obviously, the forecast is also subject to considerable uncertainty — so the exact numbers should not be taken so seriously. However, that does not stop news articles from bandying about numbers from these forecasts, as if they are established matters of fact. Ben Storrow in Politico Pro had an excellent article on the three main climate models assessing the Inflation Reduction Act, and the very considerable uncertainty involved in these forecasts. It is also possible that very pessimistic assumptions about carbon capture would make these forecasted emission reductions far less rosy. Without the models being rerun, it's hard to say anything definitive.

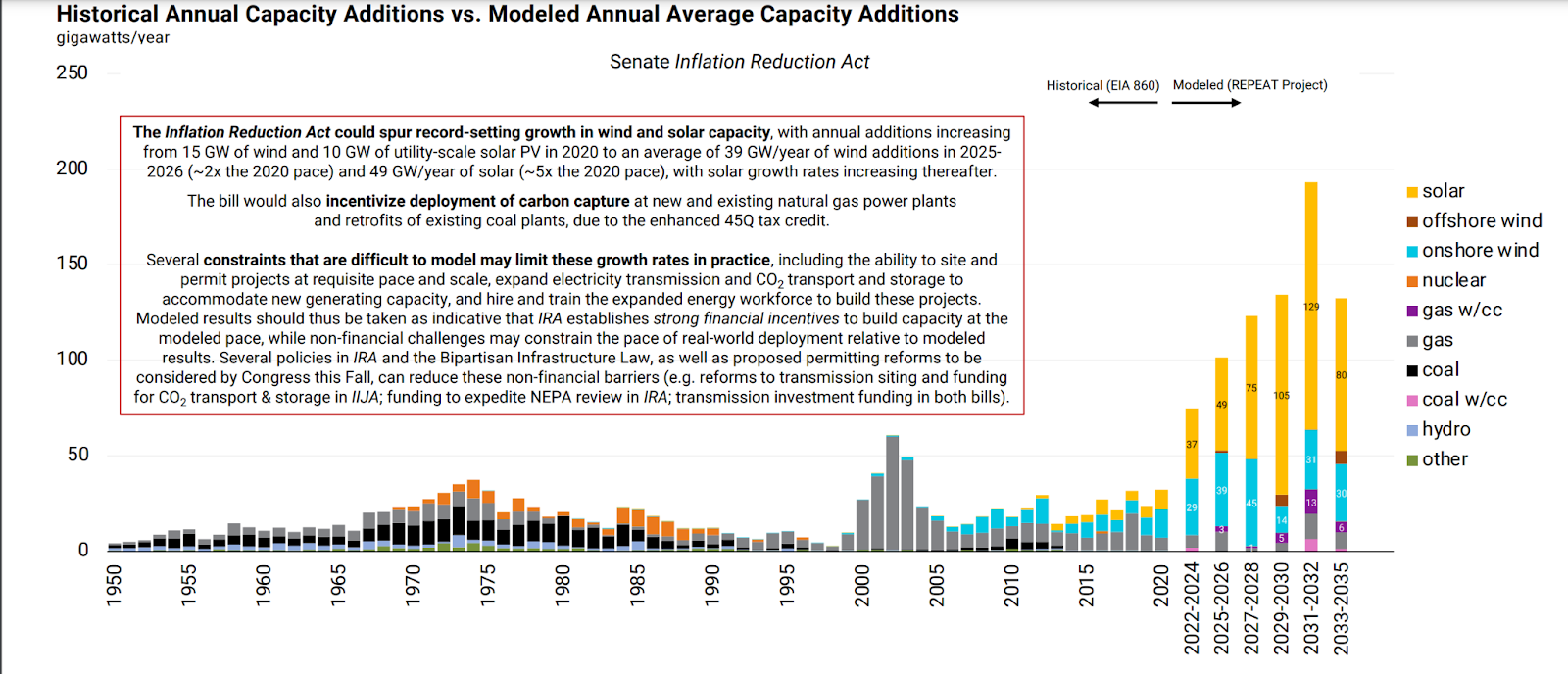

Finally, an important element of these forecasts renews focus on state and local policy, both in zoning and in fiscal policy. To grow at the projected pace, significant non-financial barriers need to be swept out of the way. From land use laws to utility rules and everything in between, there are many reasons why a basic financial incentive to pursue receiving a tax credit may not be enough. In particular, these forecasts involve an unprecedented rate of growth in solar and wind investment. These models also assume that adequate transmission and storage will be built to accommodate whatever renewable energy is generated. This is a herculean assumption — as the modelers themselves will readily tell you.

My point is not that this forecast should be discounted, but rather that local and state actors (both governmental and non-governmental) will need to make these forecasts true. A huge fight is already gearing up over energy policy now that the Inflation Reduction Act is law. Subnational fiscal policy may readily expand in anticipation of being “repaid” by utility customers, and these federal tax credits. Using public investment to speed up these decarbonization investments will become newly attractive, in a post-IRA world. Even if you aren’t particularly interested in climate change as a topic, this big brewing fight at the state and local level will potentially reshape the U.S. economy. The aftermath of the IRA will significantly change the finances of large segments of the private sector and public sector. You may not be interested in climate policy, but climate policy is interested in you.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025