Prices, Prices, Prices. (Almost) Everything You Wanted to Know, but Were Too Annoyed to Ask.

This is a premium piece of Notes on the Crises

I haven’t covered what’s been going on in pricing and the “inflation” conversation. At this point there is a lot to talk about, to say the least. In fact, part of what has taken this piece so long is any time I got a handle of all I wanted to say, yet another layer of the conversation emerged. I had made a lot of progress in fleshing out everything I wanted to say and then… Russia invaded Ukraine. I will discuss some of the implications that have for these issues later, but there is so much more of interest to say about sanctions—especially from a financial regulation perspective.

Before getting started though, it is important to cover some basics. You may hear commentators refer to something called the “price level” and/or talk about inflation like it is just one thing. I won’t get into whether inflation is even a useful concept here (you can read this piece to get some introductions to my thoughts). But for the purposes of this piece, what I am interested in focusing on is the actual price indices published by several government statistical agencies. In the United States the main important consumer price indices are the Consumer Price Index (CPI), and the Personal Consumption Expenditures price index (PCE). These indexes are published by the Bureau of Labor Statistics and the Bureau of Economic Analysis, respectively.

For our immediate relevant purposes—and most importantly for political purposes—movements in these indices are “inflation”. You may see commentators, especially orthodox economists, say that x or y movement in a price index “isn’t inflation”. We are just going to ignore attempts to define some idealized conception of inflation, separated from the actual measurement of price averages

This is important to clarify because it helps us set aside two types of arguments that mirror each other. One type of argument tries to set aside “idiosyncratic” factors—such as the pandemic or the Russian invasion of Ukraine. These affect a few categories of prices much more than others and thus- so the argument goes- are not related to “inflation”. At some point I’d like to devote an entire piece to the concept of “categories” in price indices. But for now what is important is that the price of different products are not inherently comparable. You will be looked at strangely if you say “the average price of a television/banana is 400 dollars”. Price indices solve this problem by weighting different products, by how much the “average” household spends on that consumer good. But this method makes “inflation” sensitive to the approach towards weighting, and makes certain prices (such as rents) very important to the behavior of the overall price index.

Notwithstanding that point, the second type of argument claims that there really is no such thing as particular factors which impact some categories much more than others. Instead, particular factors are a kind of “superficial smokescreen”, that papers over the “fundamental” factors that are supposedly driving “inflation”. You may think that, among other things, a shortage of microchips has created unique bottlenecks in car production that have particularly impacted the used car market. Therefore in the absence of a microchip shortage, measured CPI or PCE would have been lower. The defenders of the second argument posit that since “inflation” is generated by overall demand conditions (or more infrequently, “the money supply''), the elimination of particular bottlenecks won’t actually “positively” impact the overall Consumer Price Index.

The economic fallout from the Russian invasion of Ukraine is a major challenge to both these sorts of arguments. Many commentators may wish to dismiss the economic consequences of sanctions on Russia, and the devastation of Ukrainian production (and exports) as not part of “inflation”. But in both economic policy and in politics, “inflation” has no existence outside of these measured indices. The Federal Reserve itself is almost certainly raising interest rates faster and higher than it would otherwise if the invasion had not happened. That is because of how it interprets its “price stability” mandate. Of course, at the most basic level, these price increases still impact ordinary households—even if some commentators want to conceptually distinguish them from “inflation”.

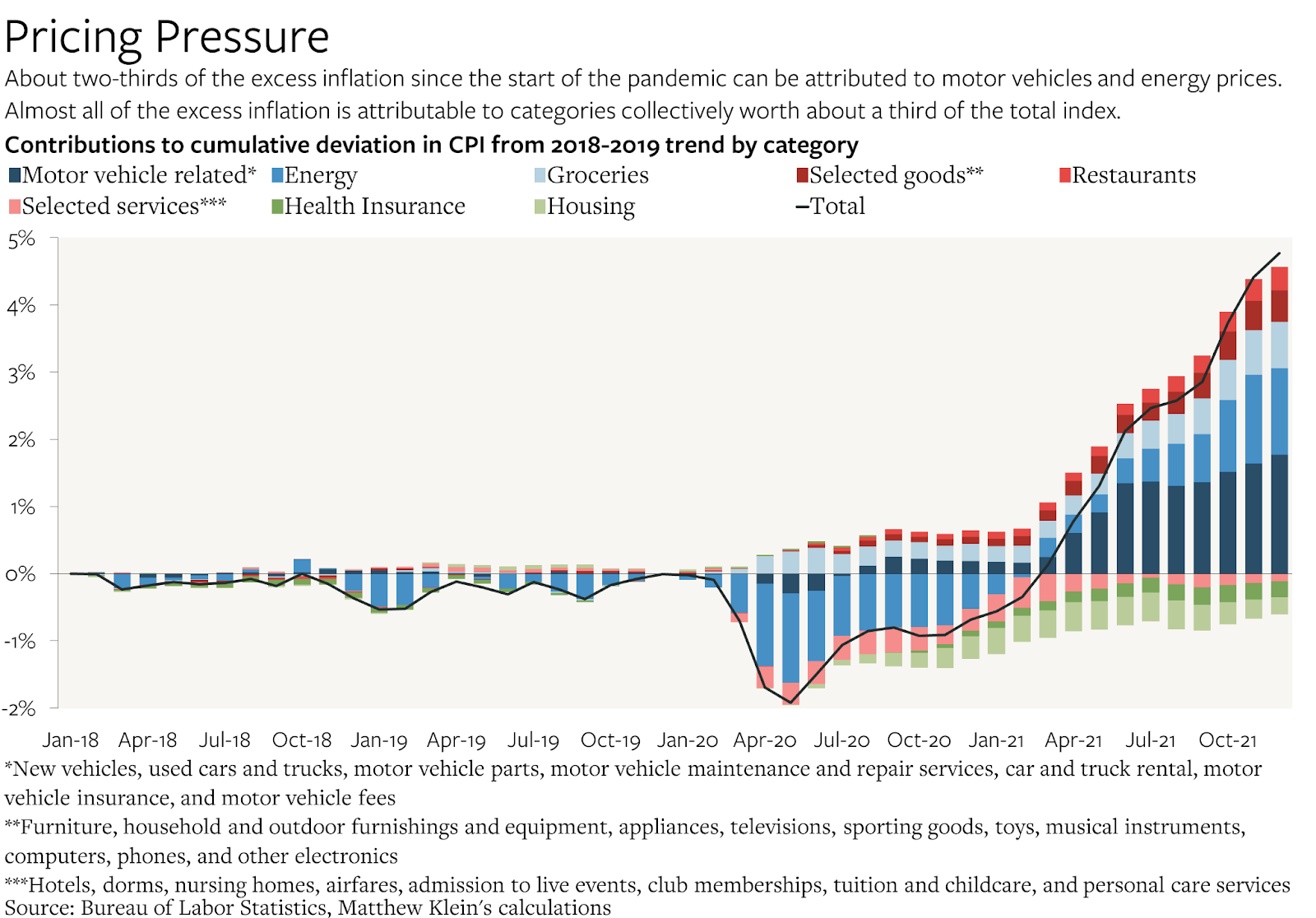

On the flipside, the rise of energy and food prices in response to this latest crisis highlights what journalist Matthew Klein has been highlighting for a long time now—even before the Russian attack the “excess” growth in CPI was almost completely attributable to food (largely meat), energy and “motor vehicle related” prices. (See Klein’s excellent chart above). That is without even considering the potential knock on price increases from energy costs rising for businesses operating in other industries. Some commentators attribute higher inflation in 2021 and early 2022 to the American Rescue Plan Act of 2021. But why would the “real” cause of these earlier price increases be a generalized “excess” demand when the price increases appeared, in large part, in food and energy. By contrast, price increases in mostly the same sectors are suddenly explicable by supply chain disruptions in the aftermath of war in Eastern Europe. The war in Ukraine is horrible. However, there is not a very strong case to be made that it has been more disruptive to supply chains than the Covid pandemic.

These points nonetheless bring me into conflict with some of the progressive and center left narratives that have surfaced in the past year about inflation. In general, I don’t find it shocking or implausible that corporations have pricing power that they can successfully deploy to raise profit margins and prices (at least in certain circumstances). However, “potentially plausible” and “the empirically identifiable cause of faster price index growth” are two different things. As I’ve just laid out, the price increases accelerating growth in the consumer price index have mostly not been in sectors with “administered prices”. In other words, not in the sectors where prices are determined by companies setting a price for weeks, months, or even years, at a time, and held constant for a significant number of transactions. Even motor vehicles, which do see administered prices, are unique in that there is a submarket for “used cars” managed by dealers. This secondhand market sees sudden and large price increases that affect the administered price decisions of car manufacturers (who have important relationships with those same dealers).

The rest of these markets are, for the most part, managed by formal exchange markets (such as the Chicago Mercantile Exchange). These exchange markets see day by day traded prices become a reference price for both wholesale and consumer prices. These markets are jointly managed by financial firms and the rules the chartered exchanges administer themselves. Many critiques can be made of how these markets are managed—but undeniably, their dynamics are not clearly explained by discrete pricing decisions by corporations. There is a case to be made that a market like meatpacking in the United States (for instance) is mostly run by the major meat companies like Cargill or Tyson. But even here, the impact on prices is debatable. Before the pandemic, the main progressive critique of meatpackers was that they were holding down meat prices for upstream producers, by locking them into long term contracts, and keeping cattle from auctions. Now it may be the case that if the meat industry were restructured, meat packing profit margins would fall. But it's very questionable whether meat price growth would have been lower during the pandemic if cattle were returned to the auction price determination process (which inherently benefits sellers.)

This all being said, it is the case that during at least the first 18 months of the pandemic many corporations experienced significantly elevated profits. Some may look at that and think that contradicts what I am saying, asking: “didn’t those profits come from higher prices?”. I don’t think so. As I explained early on in the pandemic, total profits across all businesses come from a few major sources. One of those sources is the government budget balance. Given the large expansion of government budget deficits, we should expect higher aggregate profits—regardless of specific pricing decisions made by companies. Those profits went up as the government temporarily took on business expenses, with programs like the Payroll Protection Program. Programs like unemployment insurance provided income to newly unemployed workers (who thus were no longer business expenses either). The infamous “stimulus” checks provided income across the board, to workers and non-workers alike. Both groups spent this income on goods and services sold by businesses. With these drops in expenses and jump in sales, it's no surprise that profits went up.

One could argue that if companies had “passed on” those higher profits into lower prices, overall inflation would have been lower. Some have made a version of this argument. I do not find it very convincing. In the first place, some of those profits came from programs that—implicitly or explicitly—were standing in for retained earnings by companies. These companies didn’t have big enough “rainy day” funds to get through the pandemic, and so the government stepped in. Is it really the best policy to instantly unwind those savings, just as they got built up? Now we can always make the case that far too much profit is being put into dividend payments, stock buybacks and merger and acquisitions. But financial regulation aimed at forcing businesses to save for a rainy day (an option I discussed at the beginning of the pandemic) would still not leave room for cutting target profit margins, in order to lower prices. Rebalancing away from these alternative uses of cash towards more corporate savings will not solve the “pricing problem”.

Furthermore, in the midst of a pandemic it is unrealistic to expect companies not to prepare for the obvious contingencies that may emerge such as geopolitical instability created by the pandemic such as… well… a war in Ukraine. These problems emerge without even mentioning that there were very good reasons to expect this boost in sales not to last. It is important to keep in mind that pricing is forward looking. You set a price, and thus a target profit margin today, in the hopes of having successful financial results in the future. Cutting target profit margins (or alternatively boosting the estimates of budgeted output) in the expectation that sales growth will be sustained can easily lead to financial disaster when sales growth slows, or even reverses. If before the pandemic companies didn’t already have a sense of how quickly macroeconomic trends can turn against them, the pandemic certainly taught that lesson very harshly.

This one time shot of “deficit driven” cash couldn’t sustain lower prices indefinitely—if it were even possible to coordinate among companies in the first place. The data that many organizations are relying on to claim that companies have been “price gouging” is financial accounting data of a company’s overall results. The “average profit margin” in financial accounting data is simply total profits, divided by sales. This is not very informative about much of anything: it doesn’t even tell us if companies are raising their target profit margins at the individual product level. In order to provide oversight and judgment of business pricing decisions, we need managerial accounting data that delves down to the individual product level.

Complicating things further, “cost based” price increases can lead to better financial results. That’s because businesses generally set profit margins on a percentage basis, rather than in dollar terms. In other words, if you set a profit margin on diapers that is 6% of your budgeted average total costs then any increase in budgeted average total cost will increase the dollar amount of your profit margin—even though the percentage stays the same. We can debate whether that is an appropriate approach to pricing that is in the public interest. However, the company interest in not having percentage profit margins shrinking consistently over time is obvious.

None of this means that we shouldn’t regulate corporately administered prices (I will comment on various proposals for that in the future). Nor does it mean that increasing target profit margins may not be a more significant source of price index growth over the next few years. The fact that there is so much we still don’t know is reason enough to create regulations which make the decisions—and the cost data—of corporate pricing committees far more transparent and open to critical scrutiny. What it does mean is that the answers to these questions are not as simple as they may seem on the surface. So there will need to be a two pronged approach to managing prices: one which takes the institutional differences between formal exchange prices and corporately administered prices seriously.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025