Federal Reserve Issued Securities: Not Such a Crazy Idea After All

.

This is a free piece of Notes on the Crises. Please take out a paid subscription if you want pieces to continue to be free.

Long time readers of Notes on the Crises will know that I’m an advocate of the Federal Reserve issuing its own securities. In fact, it's been almost exactly three years since I first wrote about this idea for Notes on the Crises. Please do go read my original piece if you are unfamiliar, but to recap: currently the United States Treasury issues treasury securities to fill up its account at the Federal Reserve. That means that on a consolidated basis, in other words combining all the government agencies and government corporations together, the federal government emits “money” (more narrowly defined) into the rest of the economy when it spends and sells government securities, after the fact. I’ll explain what I mean by “more narrowly defined” later on. The key point right now is that the assignment of creating checking account balances to the Federal Reserve and securities to the treasury obscures the lessons that consolidating the Federal Government, for the purposes of macroeconomic analysis, provides.

If you instead gave both agencies direct and overt money creation powers, while assigning securities issuance to the Federal Reserve, what is now covert and hidden will be revealed. The “national debt” is a scary idea that drives politics. The outstanding stock of “Federal Reserve securities” would be a boring detail only nerds like me care about. It would also provide the Federal Reserve complete control over the quantities and prices at every part of the yield curve, which its reliance on treasury securities auctions today limits. This is most clearly seen in the conduct of “balance sheet” policy over the past fourteen years. With “quantitative easing” the Federal Reserve bought many longer maturity treasury securities. When it wanted to engage in “quantitative tightening”, i.e. selling securities, its choices to sell were limited. Instead of being able to issue short maturity securities, it had to sell longer maturity securities or simply wait for securities to mature, and not buy more. They chose to do the latter, and it has been a grindingly slow process.

Of course, this proposal remains at the margins. Its benefits have not been widely extolled. It has been proposed in legislation co-authored by my colleague Rohan Grey. But we remain its core advocates and while we gain influence every day, to say the least, we are nowhere near making policy that changes the behavior of the Federal Reserve or the Treasury. As a result, I was surprised to come across a memo authored by the staff of the Federal Reserve Board and the New York Federal Reserve Bank in June 2009 entitled “Implementation Strategies for the Issuance of Federal Reserve Discount Note Obligations”. “Federal Reserve Discount Note Obligations” is just a somehow more dry way of saying “Federal Reserve securities” (of a particular type…more on that later).

As far as I can tell, no one else has noticed that this memo was declassified on May 21st 2021. That means the piece you are reading right now is the first public commentary on this memo, and its implications for Federal Reserve monetary policy. This memo is important because it establishes how widely and seriously the idea of the Federal Reserve issuing its own short maturity securities was taken. Of course, I knew that this had been discussed in 2008 and 2009 briefly, but I had not realized the extent to which the Federal Reserve not only believed in this option, but thought it was something of an “ideal” one. A speech from May 2009 from none other than then San Francisco Federal Reserve Bank president Janet Yellen is worth quoting:

An alternative approach that could accomplish the same goal, and perhaps do it better, would be something completely new for the Federal Reserve—that’s to issue interest-bearing debt broadly to private investors. Let’s call this debt Fed bills. Congress would have to authorize this, but it too is a tool available to many central banks. The sale of Fed bills would reduce the reserves of the banking system, as in a typical contractionary open-market operation. As with interest on reserves, we could accomplish a tightening of policy while maintaining our support of credit markets. But Fed bills would have an advantage over interest on reserves. The loans to the Fed would come from investors throughout the economy, not just from banks. At a time when we need banks to lend to the private sector to fight a credit crunch, this is a decided plus.

This is a very interesting excerpt. It shows that many in the Federal Reserve not only supported Federal Reserve issued securities, they thought it was superior to the current monetary policy framework. Previous to reading the Fed staff memo, I would have found such comments interesting, but perfunctory. In context, it is clear to me that they took this idea very seriously, and likely stopped talking about it for only two reasons.

First, this proposal was simply going nowhere with congress. Congress had no appetite for giving the Federal Reserve even more power. The Fed, for its part, was limited to technocratic appeals which don’t communicate the true political possbility of Federal Reserve securities. As another memo issued the exact same day says “At present, the legislative environment does not appear to be favorable for such an initiative”. Second, over time the Federal Reserve grew comfortable with setting interest rates through paying interest on reserves. There were some remaining issues as these memos illustrate. However, practical experience assuaged a number of concerns. They also could use reverse repurchase agreements with their existing legal authority to drain settlement balances from the banking system, and “support” interest rates. I will be writing about the reverse repurchase facility sometime soon.

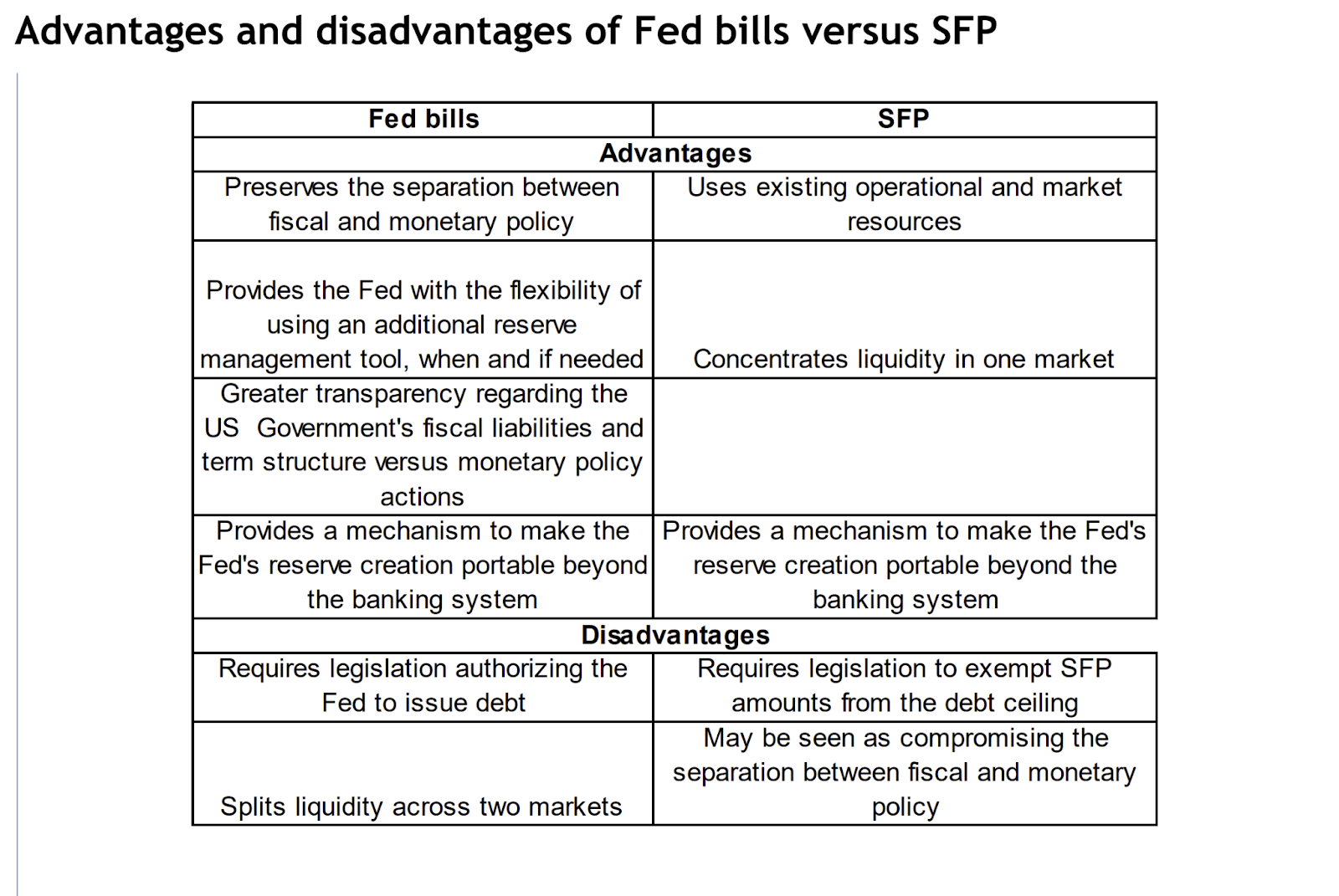

Another interesting element of this memo, and other similar discussions at the time, is the most direct alternative to “Fed bills” that was under discussion- a new program for issuing treasury bills. Called the “Supplementary Financing Program”- was actually done in 2008 to drain settlement balances. The banking system had far more settlement balances after the Federal Reserve crisis facilities filled it up. It's worth emphasizing that these were issued purely for monetary policy purposes and were held in a separate “SFP” account at the Federal Reserve. So why didn’t they go with this option on an ongoing basis?

Because of none other than the debt ceiling! This is an area where the debt ceiling has directly interfered with the conduct of monetary policy, and is part of why the treasury does not issue short maturity securities in the quantities that Zoltan Pozsar thinks is necessary to provision safe assets and “crowd out” shadow banking. As the memo says:

The effect of the SFP, therefore, is economically equivalent to the issuance of FDN. The outstanding size of the program, which peaked at about $560 billion in October 2008, has since then shrunk to about $200 billion, partly reflecting Treasury’s concerns about breaching the debt ceiling limit [...] bills issued under the [expanded] SFP would be excluded from the debt ceiling

Pozsar, and many other theorists, treat short maturity treasury securities as a form of money, albeit not one you can directly make payment with like the settlement balances I have discussed at length today (and will continue to). This is what I meant when I said settlement balances were money in a “narrow” sense earlier on. Treasury bills are money in a “broader” sense. As always, what money is depends on your level of analysis.

Anyway, the memo also proposes that Federal Reserve securities themselves be exempt from the debt ceiling. However, even with the debt ceiling exemption they still articulate problems with the Supplementary Financing Bills for precisely the reasons I highlighted at the beginning of this piece:

This constraint, however, illustrates a significant shortcoming of the current SFP in comparison with the proposed FDN program—the Federal Reserve does not have complete control over the size and timing of SFP debt issuance. In order to address these issues and as an alternative to FDNs, the SFP could be revised to require the Treasury to issue obligations promptly at the request of the Chairman of the Board. [...] Although the revised SFP would achieve similar monetary policy objectives, FDN issuance is a preferable instrument as its ultimate decisions would reside within the Federal Reserve, and consequently, there would be a more limited need for coordination on a daily basis with Treasury. In addition, although the legislation would grant control of the SFP to the Federal Reserve, market participants might perceive such a program as not truly being under the control of the Federal Reserve, with possible negative implications in the public perception of Fed independence

Thus, the official opinion of the Federal Reserve Board and Federal Reserve Bank of New York staff was, as of 2009, that the concentration of security issuance in the U.S. treasury makes the Federal Reserve dependent on the Treasury and disrupts their control over monetary policy implementation.

Of course, they are proposing short maturity securities. They are not proposing Federal Reserve securities across the yield curve. The draft legislative text in the memo limits the maturities to a maximum of one year. In fact, they even suggest only issuing securities with a maturity of less than four weeks. This is because they envision these securities co-existing with treasury securities, and are concerned about “fragmenting” liquidity for government securities. This issue of “fragmentation” is in fact the central “problem”, outside of legislative authorization, they see facing Federal Reserve securities. Interestingly enough, there is only one mention of “Fed Bills” on the Treasury website. It is, however, an extraordinarily useful one that summarizes the similarities and differences between Fed Bills and SFP Bills. I believe it demonstrates the superiority of a Federal Reserve security “only” approach.

In a battle between a technical issue of liquidity fragmentation (i.e. two instruments of the similar maturities serving the same purpose), and perceptions of treasury control or influence over monetary policy, the solvable problem of liquidity fragmentation emerges as the lesser problem. Government officials were timid and reactive in all sorts of ways in 2009. This area is just one of many where that was true. But with greater understanding and time to reflect, the wisdom of the Federal Reserve securities approach is becoming clearer and clearer, in the time of recurrent shadow banking runs and recurrent debt ceiling crises. Read closely, these very establishment documents provide intellectual support for that approach.

Notwithstanding the last paragraph, there are still some operational issues to discuss with the “Federal Reserve securities only” proposal. For one thing, the memo proposes that the securities become a joint liability of all Federal Reserve Banks. This liability would then be periodically divided up on an accounting basis, much like the securities (that is, the assets) acquired in Federal Reserve system purchases are divided in what is called the “System Open Market Account” (SOMA). I don’t like this for a number of reasons, one of which is that that would make these securities a matter of governmental corporations (or “instrumentalities") rather than agencies. An alternative would be for the Federal Reserve Board to be the issuer of the securities, and the proceeds go into its account. That’s right, for all the talk about the “Federal Reserve creating money”, the part of the Fed in Washington DC technically does not “create money” itself. Instead, it imposes a “levy” on Federal Reserve Banks to cover its expenses, then leaves those funds in accounts at one or more Federal Reserve Banks.

This modification to the proposal has a number of advantages. First, it means that reserve banks can simply purchase and hold Federal Reserve Board Securities and earn interest on those holdings just like they earn interest on treasury securities today even though these are government securities. The issue of Federal Reserve Bank income could be dealt with in different ways, but this is a simple approach which fits closely with current practice. When interest payments are made, the Federal Reserve Board could simply book a corresponding asset in a “Monetary Policy Conduct Account” so that its net worth does not change. In this way, the concerns of right wing critics of alternative monetary policy arrangements can be allievated.

This brings us to the second issue, that of treasury finance. Without treasuries, the United States Treasury would need an alternative financing tool. In fact, the issue of treasury powers was one of the things that stymied Albert Hart’s original proposal. In his proposal, the Treasury would be financed by an unlimited overdraft at the Federal Reserve. Economist George Bach says about such a proposal in his widely read but now forgotten 1950 book “Federal Reserve Policy-Making” that it “would result in a drastic reduction in traditional Treasury powers, probably too drastic to be tolerable to the government's chief financial agency.” As we’ve seen this year with the discussion of the Federal Reserve’s fiscal agent role, relying on the Federal Reserve to fully pursue its fiscal agent mandate does not inspire full confidence.

However, I think this is an issue that should be revisited more than seventy years later. As I discussed in Financial Times Alphaville earlier this year, since the late 1940s the treasury has nearly fully handed over operational responsibility for interest payments, securities tracking and securities issuance to the Federal Reserve. In the late 1940s the Bureau of Engraving and Printing was still literally “printing bonds” and securities issuance and allocation was facilitated by the Federal Reserve, but it was not fully controlled by it. The Treasury could have, in theory at least, still have sold physical securities to banks for bank deposits and even those bank payments could have been cleared on an alternative payment system to Fedwire to avoid Federal Reserve interference. This is an extreme scenario, but it illustrates that it is literally true that giving up security issuance at that time would have been giving up a significant amount of operational power. When treasury securities were fully turned into a non-physical book entry system, this operational power disappeared. The only thing that hasn’t changed is the accounting arrangements that lie behind that issuance.

Thus, as a practical matter the Treasury relinguished operational independence from the Federal Reserve and thus fully relies on the Federal Reserve legally fulfilling its fiscal agent role. This was the core point I was making in the Financial Times. Security issuance to avoid the debt ceiling, especially breaking the debt ceiling, has the same operational risks as issuing the trillion dollar platinum coin. I’d even go so far as to argue it has less since depositing the coin is the most operationally simple workaround of the debt ceiling and most directly and clearly implicates its fiscal agent role. If the Federal Reserve won’t accept this deposit, what other deposits won’t it accept? Symbolically and legally the trillion dollar coin also represents direct treasury monetary creation, which going into debt to the Federal Reserve with an overdraft does not.

How does the platinum coin fit in with the proposal for Federal Reseve Securities? Quite well, as long as you have the Board issue the securities. George Selgin’s long standing concern that platinum coins are a threat to Federal Reserve Bank income can be solved in other ways, but Federal Reserve Board Securities solves those concerns cleanly. When a platinum coin is deposited with a Federal Reserve Bank, it fills up the Treasury’s checking account. The Treasury then spends. There are more settlement balances in the banking system. The Federal Reserve Board can then issue more Federal Reserve Board securities, draining those settlement balances. The lack of interest the Reserve Bank is earning from the coin is matched by the lack of interest it is paying to the Federal Reserve Board. There is no problem of lost income here.

We can, in fact, go further. Not only is there no problem of lost income, authorizing the Federal Reserve Board to issue securities facilitates permanently solving the issue of Reserve Bank income. The Federal Reserve Board could always issue securities and sell them directly to Reserve Banks. This would always provide them additional income. The board could even “purchase” the platinum coins off of Federal Reserve Bank balance sheets with Federal Reserve Board securities. They can also engage in operations the Treasury currently does, swapping new FRB securities for maturing securities or, really, securities of any maturity. In this way Federal Reserve Banks can cleanly and easily acquire securities of any maturity and denomination they want, in any quantity they want, when engaging in open market operations.

The only remaining issue is that of “remittances”. Since the Treasury no longer needs any non-”seigniorage” inflows into its accounts (it still needs tax collection for macroeconomic reasons), Federal Reserve System remittances would serve no purpose. Worse, since this reorganization of Federal Reserve accounting relationships means that the Federal Reserve Board can always generate income for Federal Reserve Banks by selling them more securities, their income would be completely arbitrary. Meanwhile, since the Federal Reserve Board is now taking responsibility for interest payments, the Federal Reserve System on a consolidated basis would now be (usually) running a cash deficit, offset by the “Monetary Policy Conduct Account” entry. Using its existing “levy” authority, the Federal Reserve Board could appropriate all of the Federal Reserve Bank’s “residual net earnings”. That would lead the Board to mark down the “Monetary Policy Conduct Account”.

George Selgin will probably still not be fully satisfied with this accounting reorganization because the interest payments would not be reflected on the Treasury’s balance sheet- but why should they? It’s the Federal Reserve which is deciding that interest payments on government liabilities should be positive. That decision should be reflected on their balance sheet. Where Selgin sees the menace of “Fiscal QE”, I see the menace of covert central bank fiscal policy. They cause interest payments, under existing arrangements, for another agency they do not take responsibility for. Furthermore, the entire federal government should be reflected in fiscal deficit measures and, properly consolidated with the rest of the federal government, negative net income of the Federal Reserve System would be reflected in the consolidated fiscal deficit.

At this point the reader's head must be swimming. I’m sorry to add to it, but I have one more thing to discuss. Technological change has not only eliminated the basis for the original operational objection to Hart’s proposal. It has also opened up greater space for the operational independence of Treasury money creation. In addition to the platinum coin, a Digital Fiat Currency could provide the payment rails for the Treasury to create currency and directly send payments throughout the economy. These currency balances (meaning they are not accounts) could be held in digital wallets with banks, paypal, venmo, and all sorts of other apps- including publicly (or post office) administered digital wallets. My understanding is that this same integrated hardware software set up can also facilitate a new accounts layer on top of the digital currency payment rails. My colleague Rohan Grey has been a visionary pioneer in this space, writing about it just as the corollary idea of a “Central Bank Digital Currency” was just getting going in elite circles, let alone public consciousness. I can tell you based on my personal experience that when I met him 11 years ago, this was already an embryonic topic of conversation.

This is, of course, something that needs to be talked about at much greater length elsewhere. For our purposes today, what’s relevant is that not only has the existing Treasury lost the battle over operational financial independence from the Federal Reserve, there are new technologies which can reinvigorate operational independence through direct money creation. Giving up securities issuance is not the diminution it would have been seventy years ago. Concerns about the treasury engaging in its own monetary policy can be alleviated by legally restricting the financial activities it can engage in. In doing so, the Federal Reserve would still be at the height of monetary policy operational independence. That means it would just not be able to say nonsensical things about “fiscal sustainability”, or politically wield the illusory threat of fiscal crises. The debate will be purely about the macroeconomic implications of different policies in terms of aggregate demand, inflation, recessions, income inequality….and other real concerns.

To recap, this memo provides four key lessons about monetary policy:

- The Federal Reserve took actions in 2008 concerned that crisis facilities would interfere with the conduct of monetary policy. They expended political effort to drain settlement balances by asking the U.S. treasury to issue treasury bills referred to as “supplementary financing bills” that were purely issued in order to serve a monetary policy purpose. They expended political effort proposing Federal Resreve bill issuance. A major reason this political battle was abandoned is that over the course of 2009, the Federal Reserve realized that they had sufficient tools to raise interest rates, if “necessary”.

- While my proposal is still outside of the bounds of current mainstream political discourse, it's not outside the bounds of technocratic discussion among Federal Reserve experts. This memo is a rare revealing look into that technocratic discourse, with many profound implications

- The debt ceiling is interfering with the conduct of monetary policy far more profoundly than many realize, even when it isn’t that close to binding. It needs to be done away with, Federal Reserve Board securities and direct and overt treasury monetary creation is one way of accomplishing that parsimonously

- The book-entryification of treasury securities that began in the 1960s, as well as the emergence of digital fiat currency hardware & software technologies recently, creates a far different technological context for proposals to reorganize monetary policy implementation. Today the Treasury is giving up a lot less, and gaining a lot more, in letting the Federal Reserve fully take over the security issuance process and simply engage in direct monetary finance. Interest on reserves combined with Federal Reserve Board Securities, preserves the Federal Reserve’s ability to conduct monetary policy under such conditions.

That’s it for today. I recommend rereading this piece over the weekend, there’s a lot here.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025