Don’t Let Dick Cheney Ruin Price Regulation Too.

This is a Premium Pieces of Notes on the Crises

In my last piece I focused on laying out how I view the “inflation” conversation that has been going on in 2022 (on the abstract level). There I briefly touched on some received narratives about “price gouging” that have circulated among the center left. While I am skeptical that much of the elevated growth in the Consumer Price Index (CPI) or the Personal Consumption Expenditure price index (PCE) so far can be explained by discrete corporate pricing decisions, orthodox economist responses to these discussions have been far worse. They have tried to rule out the possibility that corporations can ever raise prices to elevate target profit margins (merely by assumption). They have also taken aim at any form of direct price regulation, by shaking around textbook mythologies about past experiences with “price controls” (claims made without much historical context.)

There have been too many commentaries, and too much nonsense, to deal with every argument here. However, I will take aim at a few primary issues that I think have been the core of these silly exchanges.

At the most fundamental level, this conversation starts from assuming its own conclusion. As discussed last week: mainstream economists believe that elevated inflation is a result of “excess” aggregate demand. If you believe this, direct price regulation cannot “stop” (or permanently reduce) inflation by assumption. All it can do is “repress” inflation: make shortages worse, and lead to higher inflation when price regulations are lifted. The money that people would have spent on higher prices for those goods will simply be directed to other, less price regulated goods.

The obvious issue is that we don’t all agree with orthodox economists about what is leading to higher headline inflation today. If the price increases are concentrated in certain sectors—which they are—and the bottlenecks are concentrated on specific goods—which they are—then price regulation in sectors that aren’t experiencing bottlenecks can lower headline inflation, without attendant problems. Price regulation can even be effective where the bottlenecks are heavily concentrated in very specific areas.

Even more fundamentally, if we believe that firm pricing power is a sustained issue of public concern (and not simply something that only matters in extraordinary situations) then we don’t have to believe that price regulation is of limited, time specific, interest. This is a very controversial point in some circles—but I think returning to a concrete assessment of price indices can make it more palatable for even the most hard charging critics of price regulation. Telecoms, utilities, medical prices, education, insurance and rental housing are all “unique” areas of the economy, where even many centrists agree that very significant pricing power exists, and should be constrained in some way. For some of these sectors, even direct price regulation is much less controversial than it is elsewhere. Rent regulation is of course very controversial outside the left—but at this point, even right wingers argue that legal changes need to be made to constrain rent increases. They just believe those legal changes should only be zoning changes.

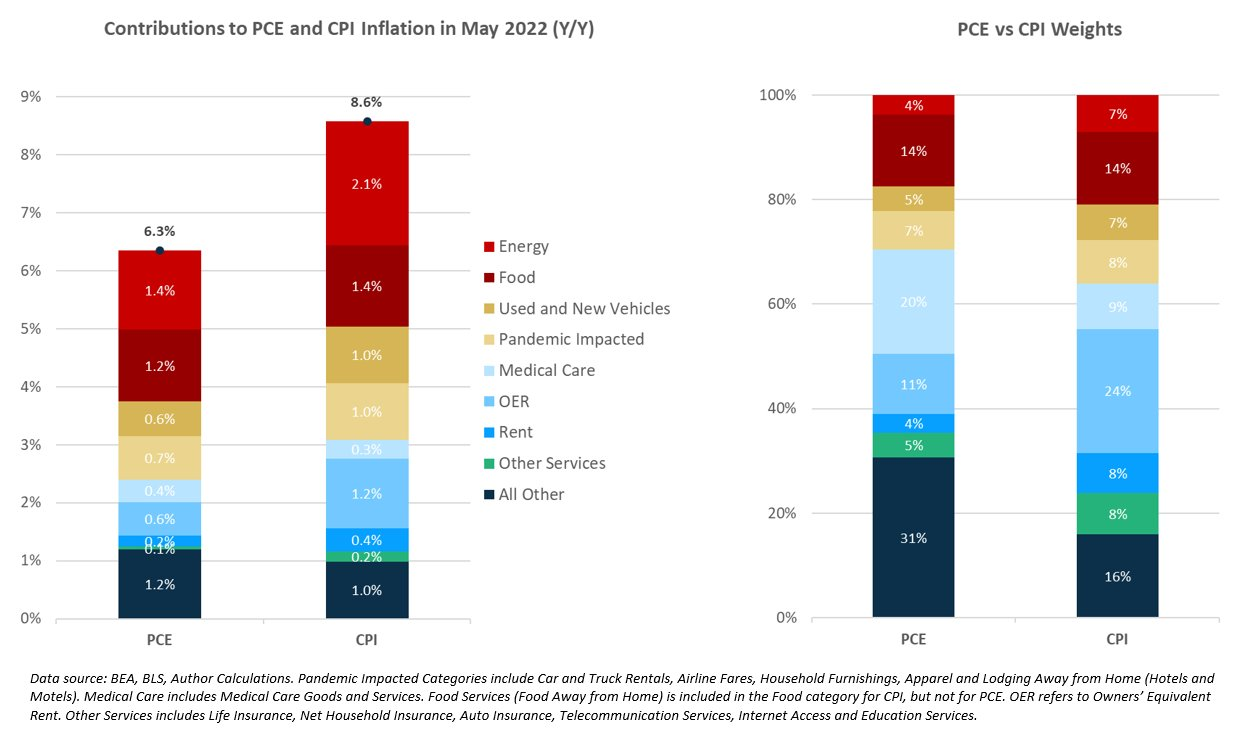

When you add up these categories, they make up between 40% and 47% of price indices, depending on the weighting used or whether you use the Consumer Price Index or the Personal Consumption Expenditure price index. Granted the majority of that number is made of housing in CPI (but not PCE). Yet, as I will argue, the case that direct price regulation wouldn’t lower rental inflation (even if you think it is a bad policy) is not very compelling. The central argument against direct rent regulation at the local level is based on the idea that it would eliminate the private incentive to build more housing. This argument is based on “first generation” rent regulations. These set absolute caps and, especially under wartime conditions, made it notionally possible that landlords could have costs outrun rents. But how relevant is this approach to today’s policy discussions? No area of the United States has had this kind of rent regulation in decades (with the exception of some apartments, which are grandfathered in literally from the world war two era, in a few jurisdictions).

This post isn’t going to discuss the topic of rent regulation in full detail. However, regardless of what you think about the rent regulation debate at the local level, it is extremely unlikely that whatever rent regulation could be applied to rent renewals at the federal level would make it unprofitable to construct more housing, to serve areas which have seen significant population net inflows (such as the south). Further, in the extreme case that this was a serious concern, the federal government could devote far more funding to simply constructing new housing directly. Even if you think both rent regulations and public housing construction (or even just public financing of housing construction) are bad ideas, I think it would be very difficult to make the case that rental inflation would be just as high, if that program was implemented.

Now if you accept the orthodox story, all of this is basically irrelevant. Sure, direct price regulation may reduce the upward contribution of these categories to price indices, but all of that will be redirected elsewhere. However, if you don’t accept this story, then strengthening price regulation over simply these categories—where even conservatives argue there are market structure issues enabling market power driven price increases—can reduce headline inflation. My colleagues at Employ America implicitly made this case in their straightforwardly titled late 2021 article: “Offsetting Persistent Inflationary Pressures With Disinflationary Healthcare Policy”.

In the piece, they argued:

Unlike other major components of core PCE, federal policy and rule-making can have substantial and direct effects for healthcare. Keeping inflation readings in check over the coming years would represent a major opportunity to demonstrate that the ambitious fiscal response to the pandemic need not lead to high inflation. Targeted disinflationary healthcare policy at this juncture could dramatically shift the policymaking and macroeconomic paradigms for a generation.

If Employ America bought the orthodox story, they would have to say that their policy suggestions to reduce medical price inflation would simply cause inflation in other components of PCE. However they, like me, think the case for aggregate demand led price increases are very weak and, like me, think it makes for great politics and good economics to use targeted price regulation to lower headline inflation. The presidential tools are the most straightforward in healthcare but, as the most recent CPI print shows, rent is an area where they could have the greatest impact—if they found the tools. Food and energy are the biggest contributors to headline inflation by far, but they are most difficult to tackle with federal policy, let alone executive authority.

Which brings us back to “price controls”. The problem with price controls is not that direct price regulation is a bad idea—it's that they have historically been designed with the idea in mind that “the” problem is excess demand. As should be clear from above, the “excess demand” argument implies that every single price in the economy needs to be “controlled”. Otherwise, “uncontrolled” prices will simply experience larger price jumps. Even worse, price regulations needed to be temporary in this framing. For one thing, you “have to” eventually return to “market organization”. For another, the point of the controls was to “slow the momentum” of prices. Once “momentum” successfully slows, price stability should continue on its own.

To summarize, the relentless logic of the orthodox position leads to the idea that if price controls are to work, they must be sophisticated enough to regulate every price in the economy. They also need to be a surprise—so markets don’t “get ahead of them” with big price jumps. Finally, they must be temporary. Looked at this way, it's a miracle there are any successful experiences with price controls. I also can’t emphasize enough that all of this sidesteps the issue of market power. If you think at least a part of headline inflation comes from businesses using pricing power to raise profit margins, then the frustrated price increases in those sectors during the “control” period will simply appear all at once when prices are decontrolled. This is true even if you happen to be someone who thinks only peculiar businesses such as telecoms, utilities, hospitals and universities have that kind of market power. This “jump” of prices after decontrol is precisely what was observed in the Nixon experience.

This is also not a retrospective criticism. Gardiner Means, the New Deal economist who coined the term “administered prices” made this point in real time, in both newspapers and articles. His criticisms are especially notable—because he was no enemy of price regulation. In 1975 he referred to this price control experience as “Nixon’s bumbling policies”. Having read what Dick Cheney (yes that Dick Cheney!) had to say about his experience running Nixon’s price controls it's very difficult not to agree. Cheney’s boss was none other than Donald Rumsfeld. I can’t resist quoting Dick Cheney at length:

The Democratic majority in Congress was urging the president to use powers they had given him when they passed the Economic Stabilization Act, legislation that effectively authorized him to commandeer the economy by imposing controls on wages, prices, salaries, and rents. The Democrats voted these extraordinary powers confident that no Republican president, much less a solid free market one named Richard Nixon, would ever use them, and in the meantime, they could criticize him for not taking action. But Nixon took them up on their offer, and on Sunday night, August 15, 1971, he announced a freeze for ninety days on all wages and prices. The Cost of Living Council was created to monitor the freeze and to achieve an orderly return to the free market when the ninety-day period was over

The freeze was simple enough. Nobody was to raise wages or prices. But the follow-on, which became known as Phase Two, would have to have rules covering all sorts of things, from permitted increases in union contracts to the price of dill pickles, for the period until market forces ruled again. The deadline for moving from the freeze to Phase Two came fast, and the two entities that were supposed to write the regulations, the Pay Board and the Price Commission, wrangled and dithered. When it looked as though they were going to miss a crucial deadline for getting regulations published in the Federal Register, Rumsfeld decided to take things in hand. He assembled Jack Grayson, the chairman of the Price Commission, and about a dozen of our CLC staff and said that we wouldn't be leaving until we had the regulations ready for the printer. We set up in Rumsfeld's outer office, and as others paced and dictated, I sat at one of the secretary's desks and typed everything on an IBM Selectric typewriter. By nine the next morning, when the secretaries arrived and emptied the ashtrays and replenished the coffee, we had written the regulations that would now be governing a major share of the U.S. economy. The degree of detail we achieved during our overnighter was truly impressive. We drew distinctions between apples and applesauce; popped and unpopped corn; raw cabbage and packaged slaw; fresh oranges and glazed citrus peel; garden plants, cut flowers, and floral wreaths. We regulated seafood products "including those which have been shelled, shucked, iced, skinned, scaled, eviscerated, or decapitated." We covered products custom-made to individual order, including leather goods, fur apparel, jewelry, and wigs and toupees.

Regulating energy prices was one of the most complex and complicated tasks the CLC had to address. At one point, when we were up against a deadline to set prices for the coming week on oil, we discovered that there was no one available with expertise in that area. Then someone mentioned that Chachi Owens was from Texas and that Texas had a lot of oil, so we called Chachi and asked him to stop by. At that time he was working for the public affairs office. If the CLC was going to permit the price of bread to rise by two cents the following week, it was Chachi Owens who would bring you that news.

Aside from his resonant voice, his claim to fame was that he had played fullback for Darrell Royal at the University of Texas. He turned out to be a very bright young man. Perhaps it was his Texas confidence, or perhaps it was the result of the coaching he'd received, but he had no hesitation about sitting down and writing the oil regs we needed. [In My Time, pages 59-61]

To me, the lesson of the Nixon “price control” experience is that you don’t put Richard Nixon, Donald Rumsefeld and Dick Cheney in charge of the economy. Nixon, a man who actually worked during World War Two in the Office of Price Administration, did not like his experience, and hated his coworkers. Nixon even later claimed later that it was this experience which led to his “lifelong” hatred of Bureaucrats, and “big government”. Like most of Nixon’s political moves, his dalliance with price controls was purely cynical, and carefully calculated. Very few policies can survive the lack of belief and lack of expertise of both the highest political official involved, and the government employees ordered to organize them. Add in the surprise, temporary nature and complexity of the task of comprehensive price controls demanded by the orthodox framework, and you have a recipe for disaster.

However, direct price regulation of selected sectors that are important in price indices are far easier to accomplish with the mechanisms that already exist. They do not require price fixing for every single item, or attempts to use the tools best applied to administered price setters on markets(such as meat or oil) which are not organized by administered prices. Nor do they have to be temporary since they are aimed at managing permanent issues of market structure and market power — rather than temporary issues of excess demand. Even extremely limited price regulation can lower headline inflation, and relieve some pressure on the Federal Reserve to raise interest rates.

Careful readers may have noticed that I focused on the sectors where the case for market power-driven price increases are the most obvious, and least controversial. I happen to think that there is a case for direct price regulation in other sectors where administered prices predominate. I will write about that more in the future—but for now interested readers can check out my chapter in the Cambridge Handbook of Labor in Competition Law, with Luke Herrine. I think price regulation can work in these other sectors, too. But how these markets are organized will likely need to be fundamentally changed for regulation to be most effective. For our purposes today, what matters is that—despite what you have heard—price regulation has a role to play in saving the Federal Reserve from its own policy mistakes.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025