Trump Vs. Powell: The Big Takeaways from Trump’s Assault on the Federal Reserve

Hello readers; I’m long overdue for major updates across a whole range of issues. I have continued to work full time on Notes on the Crises but the work of setting up a physical office takes significant time and energy. Among other things, I have secured a fiscal sponsor so I could take 501(c)3 donations, and continue to pursue investigative work which is taking time and effort to gestate. One small project I can publicly reveal is that, with the help of the yeowoman’s efforts of John Jay student Josie-Grace Valerius I can say that the Notes on the Crises Youtube channel is now hosting the obscure and previously inaccessible recordings of public meetings of the Financial Stability Oversight Council. I thought it was important to preserve these videos with the recent threats to FSOC.

There are other projects I have been working on as well that I am not quite ready to publicly reveal-including frankly, some unexpected but typical delays. Readers will be hearing more about all of these developments-and more- very soon. Finally, frankly, after the first five months covering Trump I also needed to slow down to prevent burnout. Now that I've worked through a large backlog of administrative tasks and project gestation, I can refocus on writing.

However, rather than picking up some of the threads of my coverage going into the summer, I need to cover the monumental developments over the intensifying conflict between Donald Trump and Federal Reserve Chairman Jerome Powell. In certain respects it is strange how little I’ve written about the Federal Reserve. Right up until my January 31st piece on impoundment, the Federal Reserve was the focus of almost all my writing at Notes on the Crises. I spent the last year and a half of the Biden administration intensively doing archival research related to the Federal Reserve, while issuing hundreds of Freedom of Information Act requests targeting the Federal Reserve.

In fact, I issued so many FOIA requests over that period of time that the 2025 FOIA report obliquely referenced my FOIA requests to explain the increase of its backlog;

In addition, approximately twenty-two percent of the incoming requests involved complex information from five news media requesters pertaining to Board members' communications and meetings with members of the executive branch as well as various memoranda concerning a Federal Reserve System publication. [emphasis added]

Those “various memoranda” were memos mentioned in the 30,000 page 1967-1973 Federal Reserve Board Minutes which I successfully acquired through FOIA last year (which are now searchable and freely available on this website). That’s without even mentioning auctioning off a book proposal about the Federal Reserve entitled Picking Losers in April 2023.

So if I’m obsessed with the Federal Reserve, why haven’t I been writing about it? Well in large part it's because I was so busy, and I found it challenging to gather all of my complicated thoughts about the Federal Reserve at this moment. Another reason is that I simply thought the other aspects of the Trump-Musk Payments Crisis mattered much more. At this point, however, I would be shirking my responsibility as a Federal Reserve expert not to comment on the situation. So here goes…

Wait, What’s Going On?

Some readers may not really have clocked the burgeoning conflict between Trump and Powell. The bottom line is that President Trump has long criticized Federal Reserve chairman Jerome Powell for either raising interest rates or not lowering them.

In this respect Trump is straightforwardly bringing his intuitions from his time as a real estate developer. Real estate is an incredibly leveraged industry where relatively small variations in interest rates can raise a project’s average total costs dramatically. As no less than economist Hyman Minsky pointed out in 1990:

Two factors made Trump somewhat unique--one was that he developed a fortune in a period of high real interest rates, and the second was that the cash flows on most of Trump's properties were negative. [...] Trump was golden--he had the magic touch– as long as property prices were increasing at a more rapid rate than the interest rate on the borrowed funds. [...] In the short run Trump could make his interest payments with funds from new loans– but when the increase in property prices declined to a value below the interest rate, Trump would become short of the cash necessary to pay the interest on the outstanding loans

In this commentary Minsky anticipates Trump’s bankruptcies- and perhaps even his October 1990 default to lenders; although it is not one of his, shall we say, more impressive predictions. The point is, Trump is a man who might never have gone bankrupt at all if the Federal Reserve had cut interest rates in 1990- or raised them in 1988 and 1989. The best way to understand him is to see these moments as permanently imprinted on his consciousness.

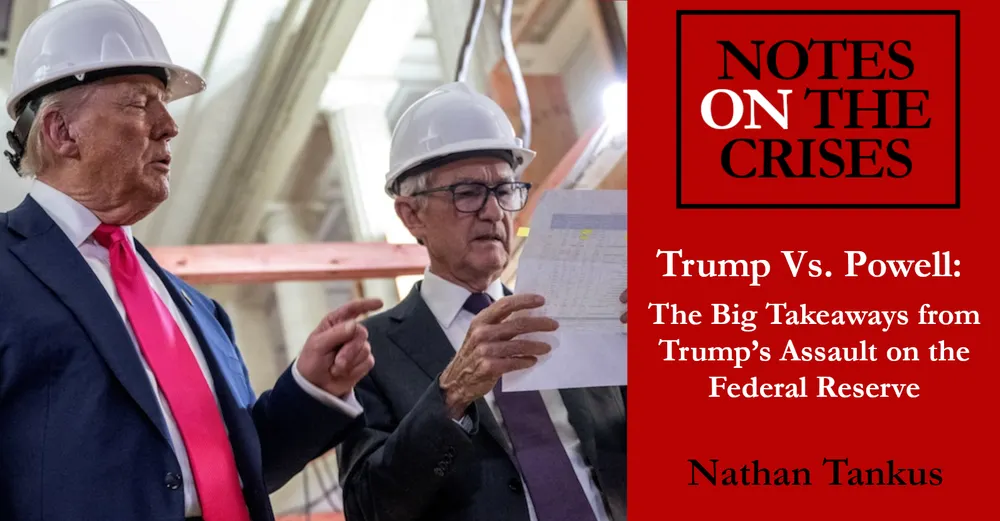

The Federal Reserve has, of course, not been cooperating. This is both because of its views of the general macroeconomic picture and, specifically, the impact of Trump’s erratic tariff policies. Thus, inevitably, the attacks began. Trump spent the summer going back and forth over whether he was going to fire Powell, ultimately backing off- at least for now. A major part of the Trump Administration’s attack was over Federal Reserve Board building renovations and cost overruns. This led to a comic scene of Trump and Powell wearing hard hats walking through a construction site and arguing over budget numbers on a piece of paper. The point is, the pressure is clearly very much on.

Just this Wednesday, a new attack emerged- this time targeting Fed governor Lisa Cook- the first Black woman (or woman of color for that matter) appointed to the Federal Reserve Board. The head of the Federal Housing Finance Agency is apparently accusing her of committing “mortgage fraud” in 2021. She has explicitly told the press that she will “not be bullied”. Trump clearly intends to bend the Federal Reserve to his will, just like he has done- or has been attempting- with every other administrative agency.

Federal Reserve Independence is An Ideology, Not a Legal Arrangement

Which brings us to “central bank independence”. The phrase “central bank independence” gets thrown around so much that I think many readers believe that this is a reference to some statute or law. Failing that, it might seem to have a particular or precise meaning. In fact, this idea is not encoded anywhere in U.S. law. Even in places where some form of “central bank independence” is legally encoded, the ideology came well before the legal niceties. As I wrote about in my 2021 piece (that I only belatedly published earlier this year), this ideology is a crude and amateurish attempt to cover some of the core issues debated in administrative law. This is important for a few reasons.

First, let's have a little refresher on the basics of “law”. The term “laws” is imprecise. Typically, when we think of “laws” we think of bills passed by congress. They are, as the phrase goes, “signed into law”. Passed bills are known as “statutes”. Yet, an executive order also has the “force of law”. A constitution- specifically the United States constitution- is supposed to stand above all of these. An unconstitutional statute, even if it's passed by congress and signed by the president, is overruled by the constitution itself. At least, that’s notionally how it's “supposed” to work.

Then there are court decisions. Court decisions which overturn precedent are sometimes described as “reinterpreting” law. However, another way of thinking about this- which I think is more useful for people who aren’t invested in the ins and outs of the legal system- is that Courts create law. Roe v. Wade made abortion legal nationwide when it was not before. Dobbs v. Jackson Women's Health Organization in turn made it legal for states to overtly criminalize abortion. These were forms of legal creation and destruction. Now, of course, courts are “supposed” to constrain their legal creation and destruction to the ambiguities and contradictions between constitutional provisions, congressional statutes, executive orders and administrative agency guidances etc. The “symbolism” of interpretation is where courts are supposed to derive their legitimacy and ultimately, other bodies of law “should” dominate; Emphasis on should.

Today, of course, it is plain that if this was ever true- it is not true today. The Supreme Court blatantly places Trump administration executive orders above statutory and constitutional provisions. Supreme Court Justice Ketanji Jackson aptly summarized the current situation in a dissenting decision just yesterday: “This is Calvinball jurisprudence with a twist. Calvinball has only one rule: There are no fixed rules. We seem to have two: that one, and this Administration always wins.” This situation is, of course, what I’ve been fixated on from even before I became aware of the Trump-Musk Payments Crisis. As I wrote in my impoundment piece on January 31st “As a famous twentieth century statesman might have said in this situation ‘...and how many divisions does the Constitution have?’” Legitimacy is being treated as a sucker’s game and as long as no major institution responds, isn’t it a sucker’s game?

This “view of law from space” might seem far afield of our topic today, but it is not. It's important to have the big picture in mind because it helps us clarify what concretely protects the Federal Reserve’s “independence”. The founding moment of Federal Reserve independence known as the “Fed-Treasury Accord” happened in March 1951. Note the phrasing: “accord”. It was not a law, it wasn’t even an administrative guidance. It was a terse press release from two government agencies. In other words it's not law- it's a norm. And, as we all know, norms are not long for this world under Donald Trump. The fundamental legal basis for the Fed’s so-called independence was created not in 1951 but in 1935.

Since February 2024 I have, again and again, gone back to the 7 monographs written by one of the most important General Counsels of the Federal Reserve Board- Howard Hackley- which I got from the Federal Reserve through FOIA in discussing the Fed’s legal structure. The most important monograph- “The Status Of The Federal Reserve System In The Federal Government”- is the most comprehensive publicly available legal treatise on the Federal Reserve’s independence- or lack thereof- within the Federal Government. This book makes plain that the Federal Reserve’s independence rests on two foundations- that it is not subject to the appropriations process in determining its budget and the legal protections its leadership has against removal. The question of firing Powell- or any other member of the Federal Reserve Board or the Federal Open Market Committee- is a matter of the latter.

Powell’s Executor

Those protections against removal come from the Banking Act of 1935- which, by happenstance, was signed into law by FDR 90 years ago tomorrow. They built on a supreme court decision which had come just three months beforehand called Humphrey’s Executor v. United States. As I wrote about all the way back in February, this case ruled that FDR’s firing of a Federal Trade Commission (FTC) commissioner was unconstitutional. Its protections were clearly built atop that recent case. This means that there are no special statutory or constitutional protections for the Federal Reserve’s discretion relative to the President. It has the protection that any other independent administrative agency has- or doesn’t have.

Which brings us to the fact that Humphrey’s Executor was struck down by the current supreme court mere days before its 90th anniversary. This is, of course, the holy grail of right wing proponents of “Unitary Executive Theory” i.e. the idea that all “executive power” is under the president’s direct control. A February 18th “Fact Sheet” from the White House summarizing the executive order “Ensuring Accountability for All Agencies” neatly summarizes this “theory”:

Therefore, because all executive power is vested in the President, all agencies must: (1) submit draft regulations for White House review—with no carve-out for so-called independent agencies and (2) consult with the White House on their priorities and strategic plans, and the White House will set their performance standards

The category of “independent agency” is thus, in the view of the Trump administration and the Supreme Court, dead.

Well, the above is a little misleading because I cut a crucial part of the “fact sheet” out. It does give an exception to its sweeping “no carve-out” position. The fact sheet, following the executive order itself, says “except for the monetary policy functions of the Federal Reserve;” [emphasis added]. This exception is, of course, completely ad-hoc. It should not be comforting to even the narrowest supporter of “central bank independence”. Yet the “conventional wisdom processor” on Wall Street did not react with alarm to this executive order the way it should have.

The Supreme Court itself took this ad-hoc exemption and ran with it. It made up an absurd and patently false legislative history for the Federal Reserve system in Trump v. Wilcox:

Finally, respondents Gwynne Wilcox and Cathy Harris contend that arguments in this case necessarily implicate the constitutionality of for-cause removal protections for members of the Federal Reserve’s Board of Governors or other members of the Federal Open Market Committee. [...] We disagree. The Federal Reserve is a uniquely structured, quasi-private entity that follows in the distinct historical tradition of the First and Second Banks of the United States [emphasis added]

This is simply not true. As Columbia law professor Lev Menand says in a quickly written takedown of this claim:

But the Federal Reserve Board and the FOMC are not banks, nor are they corporations, nor are they lending new money to households and businesses like the national banks (antebellum and postbellum). The Federal Reserve Board and the FOMC are government agencies designed to regulate banks

The dissenting Supreme Court justices also note this bizarre Federal Reserve carveout.

Justice Elena Kagan states in her dissent:

The majority closes today’s order by stating, out of the blue, that it has no bearing on “the constitutionality of for-cause removal protections” for members of the Federal Reserve Board or Open Market Committee. Ante, at 2. I am glad to hear it, and do not doubt the majority’s intention to avoid imperiling the Fed. But then, today’s order poses a puzzle. For the Federal Reserve’s independence rests on the same constitutional and analytic foundations as that of the NLRB, MSPB, FTC, FCC, and so on—which is to say it rests largely on Humphrey’s. [...]

Because one way of making new law on the emergency docket (the deprecation of Humphrey’s) turns out to require yet another (the creation of a bespoke Federal Reserve exception). If the idea is to reassure the markets, a simpler—and more judicial—approach would have been to deny the President’s application for a stay on the continued authority of Humphrey’s

This “bespoke” Federal Reserve exemption is one reason that Trump’s attack focuses on building renovations- i.e. Federal Reserve fiscal policy.

The Fed may be independent in its “monetary functions”, whatever that is, but that implies presidential supremacy on “non-monetary” matters. The Federal Reserve itself has taken on this kind of interpretation which is why it left the Network of Central Banks and Supervisors for Greening the Financial System (NGFS) before Trump was even inaugurated and Michael Barr stepped down as vice chair for supervision. It's hard to see why direct control of financial regulation by the president is less “dangerous” than interest rate policy and/or financial asset purchase and sale policy.

Of course, the “Federal Reserve” exception will hold only as long as it is of use to the president. Powell may boldly say that firing him is “not permitted under the law” but, absent radical and bold action on his part, the battle over whether Trump can just fire him was lost when Humphrey’s Executor died in May.

The Unitary Executive is Not a Solution to the Problems with Monetary Policy

Some progressive commentators are embracing presidential supremacy over monetary policy as an outlet for “Democracy”. This has been something I’ve opposed for years. My 2021 commentary on this issue I think holds up quite well:

While in some respects attractive, the self-styled populist perspective is a trap. By accepting the premise that monetary policy is only democratic if interest rates and credit policy decisions are directly set by legislatures or heads of state, outside critics help reinforce the choice of economists to conflate anti-democratic preferences, with issues of administrative action, and careful deliberation. In the post-Trump world, it is easy to casually dismiss such suggestions as dangerous and defend central bank independence as a kind of “lesser evil” to those who are not deeply invested in the issue. Professor Skinner’s beginning submission to this roundtable is a strong recounting of this “lesser evil” case.

We do not have to accept this dichotomy. Rejecting central bank independence doesn’t have to mean rejecting administrative discretion, or some degree of independence from short-term political considerations heads of states and legislatures face. Conversely, arguing for “democratizing” central banking doesn’t necessarily mean more legislative or executive determination of the day to day — or even year to year — decisions. Once we learn to ignore this false dichotomy, we can start to imagine a variety of administrative structures which provide ordinary people the ability to provide meaningful input into these decisions. [emphasis added]

Unitary Executive Theory was on my mind when I wrote those words and the second Trump administration has illustrated my point in spades. We are in a constitutional crisis where the centralization of power under direct control of the president and the disempowerment of independent administrative agencies, congress and the courts is moving forward at a truly breathtaking pace. It's farcical to see yet more Trump capriciousness as a victory for “democracy”.

I have so much more to say on this topic. I want to comment on the fascinating episode between Trump and Powell over Federal Reserve renovations more. I want to comment on the interaction between interest rate policy and government interest payments. I want to unpack whether direct control over monetary policy would even accomplish what Trump would hope to accomplish. But this piece is already very long and we need to see what Chairman Powell will say at Jackson Hole today. I’m very much looking forward to it.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025