Low Interest Rates Don't Drive Market Concentration

A critical assessment of Atif Mian, Amir Sufi and Ernest Liu’s paper

Dear Readers,

As of this article, I’ve returned from my hiatus. I would like to thank you for your patience, especially paid subscribers who chose to continue supporting me. It really means a lot to know that I can take some time when absolutely necessary and my livelihood won’t disappear. In the future I hope to plan guest articles as well as pre-written articles so that the publication of Notes on the Crises will continue uninterrupted during my vacations. (As always, anyone interested in a guest essay should reach out to me at: crisesnotes[at]gmail[dot]com) Over the following month I am preparing to publish at least two articles a week that are original to Notes on the Crises. In addition, in September I will be launching the Spanish version of Notes on the Crises. Ten articles have already been translated, and more are being prepared each week. Finally, I will also be writing opinion pieces for mainstream publications, including one very exciting one which I can’t announce yet. Those articles will, as always, be linked to here. Later this week I will be returning to my long running series on the Federal Reserve’s Coronavirus Response. Thank you again for your patience and support.

On August 18th economists Atif Mian, Amir Sufi and Ernest Liu published a second version of their paper “Low Interest Rates, Market Power, and Productivity Growth”. This influential macroeconomic theory paper articulates a model where low interest rates ultimately lower competition, reduce productivity growth and raise profits. I generally don’t criticize specific new mathematical macroeconomic models in my writing. Parsing these papers takes a particular skillset, and the conclusions are often not necessarily relevant to the economic policy debates I’m involved in. Yet, this paper is increasingly gaining traction in economic policy circles. I was particularly struck that former Federal Deposit Insurance Corporation chair Sheila Bair linked to the piece, when arguing that in the real world low interest rates were driving market concentration:

I’m all for robust antitrust enforcement. Markets don’t work without competition. Yet, overlooked is the role of low interest rates in driving market concentration. https://t.co/MKIw147NNh

— Sheila Bair (@SheilaBair2013) August 23, 2020

It is because of this work’s increasing influence on economic policy circles that I think it's worth responding to. If policymakers become convinced that low interest rates are driving market concentration and inequality, it is possible they will pursue raising rates. This will hurt the economy, at a time when state and local governments are already having budgetary crises, and unemployment is already at devastating levels. Higher interest rates will also make expansionary fiscal policy look less attractive.

While I personally think expansionary fiscal policy is still worth pursuing at higher interest rates, this is not widely agreed upon. Many of the public defenses of spending more now lean on how low interest rates are. Even Green New Deal advocates talk about how the proposal is appealing as interest rates are just so low.

The critical question thus is, does the result from Mian, Sufi and Liu (hereafter “Mian et al”) hold in the real world? To examine that, we will have to examine their argument more deeply.

The clearest concise summary of their argument comes at the beginning of this paper:

When the interest rate is low, the present value of a persistent market leader becomes extremely high. The attraction of becoming a persistent leader generates fierce and costly competition especially if the two firms are close to one another in the productivity space. When making optimal investment decisions, both market leaders and market followers realize that their opponent will fight hard when their distance closes. However, they respond asymmetrically to this realization when deciding how much to invest. Market leaders invest more aggressively in an attempt to ensure they avoid neck-and-neck competition. Market followers, understanding that the market leader will fight harder when they get closer, become discouraged and therefore invest less aggressively. The realization that competition will become more vicious and costly if the leader and follower become closer in the productivity space discourages the follower while encouraging the leader. The main proposition shows that this strategic effect dominates as the interest rate approaches zero.

There are a number of ways that this argument could be criticized. In particular, an entire article could focus on their conception of competition. (However, that will have to wait for another day.). Both the most interesting feature of this passage, and its key problem, is their conception of interest rates.

When Mian (et al) talk about interest rates, they are not really emphasizing the borrowing costs that a firm may face. Instead, they are referencing the “discount rate” that a business may use to compare investments today to their possible financial returns in the future. In mainstream economic theory this is important because there is a “time value” to money that comparing nominal dollars invested today to nominal dollars received in the future would miss. Their assumption — like much of mainstream economics — is that the interest rate firms face “in the market” will determine the “discount rate” that they apply to prospective investments. And then that discount rate will in turn determine their investment decisions. (For the financial theory folks, don’t worry I’ll get to more real world financial theory in a second)

This assumption is important for a number of reasons. One outcome is that the most important parts of the model may not jump out at you, if you’re unused to thinking about interest rates in this way. In a world where the statistical odds of future returns when taking a particular course of action is known with certainty — and there are no financial constraints — the discount rate is the only factor that changes the current level of investment. At low discount rates, the value of future returns (such as being a “market leader” forever) becomes extremely large, in this model. In fact, the article says“as r [the discount rate] approaches zero [...] the value of being a permanent leader goes to infinity”. A zero discount rate on future returns in this thought experiment makes any project with a positive return on investment worthwhile.

The trouble with this is that this is not how discount rates are used in actual business decision-making. This simple point has been shown by a large body of literature over the past few decades. Worse still: the rate used in actual business decisions, hurdle rates, isn’t the main determinant of business decision-making that the model suggests. Let’s consider the quantitative and qualitative research on this topic.

A good place to start is a 2015 paper from Federal Reserve economists Steven Sharpe and Gustavo Saurez which has finally been published by the journal Management Science in 2020. They point to a number of very important issues. First, the quantitative evidence is mixed “at best” for an effect of interest rates on investment. Second, the qualitative evidence (i.e. surveys of executives of companies) uniformly finds that the vast majority of firms wouldn’t change their investment plans for even large declines in interest rates. Particularly relevant here, they use survey data from a special edition of the Duke University Chief Financial Officer Survey with unique questions illustrating this point.

It is worth quoting their summary of the survey in full:

These key survey questions asked the respondents to assume that “demand and cost conditions faced by your firm and industry remain the same” and then answer the following: “By how much would your borrowing costs have to decrease to cause you to initiate, accelerate or increase investment projects in the next year?” (Question 7a) After responding, the executives were asked the opposite question for interest rate increases (Question 7b). They were given six response choices (in addition to the option to answer “N.A.” [not applicable]): 0.5 percentage points, 1 percentage point, 2 percentage points, 3 percentage points, more than 3 percentage points, or “It’s likely we would not change investment plans in response to an interest rate decrease.”

In response to the key survey questions, we find that a large majority of CFOs indicated that their investment plans are quite insensitive to potential changes in borrowing costs. Only 8% of firms would increase investment if borrowing costs declined 100 basis points, and an additional 8% would respond to a decrease of 100 to 200 basis points. Strikingly, 68% did not expect any conceivable decline in interest rates would induce more investment. We find that firms did expect to be somewhat more sensitive to an increase in interest rates, though, even here, only 16% of firms indicated they would reduce investment in response to a 100 basis point increase, whereas 37% did not expect that any conceivable increase in interest rates would cause them to cut back investment plans.

What’s driving these results is that it is financial constraints which constrain business decision-making. Firms with few or inadequate financial assets are very exposed to the availability and cost of ‘external’ finance. But while that’s true in the world, Mian (et al)’s model has no financial constraints. This causes their model to miss that interest rate cuts function more as a tax cut — in the sense that it provides firms additional funds, that they wouldn’t otherwise have access to. From the perspective of the firm, these additional funds can be spent, or saved for a rainy day. Meanwhile, interest rate increases function like tax increases for these very exposed firms. Like tax increases, interest rate increases are more likely to reduce investment spending, than decreasing interest rates are to increase spending.

Meanwhile, firms with lots of savings aren’t very concerned with their financial constraints, either way. So market interest rates are much less directly relevant to them. Note that this suggests that the opposite relation than the one posited by Mian et al. Namely: constrained firms become less sensitive to market interest rates as the level of interest rates falls, and interest burdens fall. Additionally, unlike in their model, firms are more sensitive to interest rate increases than they are interest rate decreases.

Where does that leave us with discount rates? These financial tools have been popularized by finance and accounting scholars. Perhaps more importantly, through training future business people they’ve become widely adopted by non-financial businesses. Along the way, though, they’ve been adjusted and changed to fit the needs of business people. Few businesses directly compare investment returns to a discount rate, nor do they calculate discount rates for given contexts the way business scholars argue is technically correct. Surveys suggest that after a sustained multi-decade campaign from business and finance scholars, majorities of medium sized and large businesses use for their “discount rate” the “weighted average cost of capital” (WACC). However the Capital Asset Pricing Model, the standard model for estimating the cost of equity, is not uniformly used by the businesses that use WACC.

Even among businesses that calculate the weighted average cost of capital, partially using the Capital Asset Pricing Model, there are all sorts of adjustments finance scholars would recommend that aren’t used. One of the most notable is not calculating project specific discount rates. There are other businesses that use CAPM but don’t calculate a cost of debt or weight it along with the cost of equity. For the purposes of this discussion, what matters is that “cost of equity” is almost always calculated in some fashion and very rarely is the interest rate on borrowing the sole input to a discount rate.

The direct result is this: the cost of equity doesn’t fall simply because risk free interest rates fall. Remember that for Mian et al’s results to say anything about our world, low discount rates must be driving particular types and quantities of business investments which drive market concentration through sales growth for market leaders. If we’ve never had low discount rates — even at times when interest rates were low for sustained periods of time — their model can’t explain empirical regularities like rising market concentration. We’d be left with consistent assumptions that fall short of an applicable explanation.

In fact, it gets worse than this. Because whichever model a firm uses, it almost never applies the resulting discount rate to investment decisions. Instead firms produce what are called “hurdle rates” which is typically the outcome of one of these models plus some idiosyncratic process by which a premium is added. Once a hurdle rate is set, it rarely changes. Even if the cost of capital has significantly fallen for a sustained period of time. As it turns out, hurdle rates haven’t fallen much, if at all, in the last 35 years. This is true even after a sustained period of low interest rates resulting from the great financial crisis.

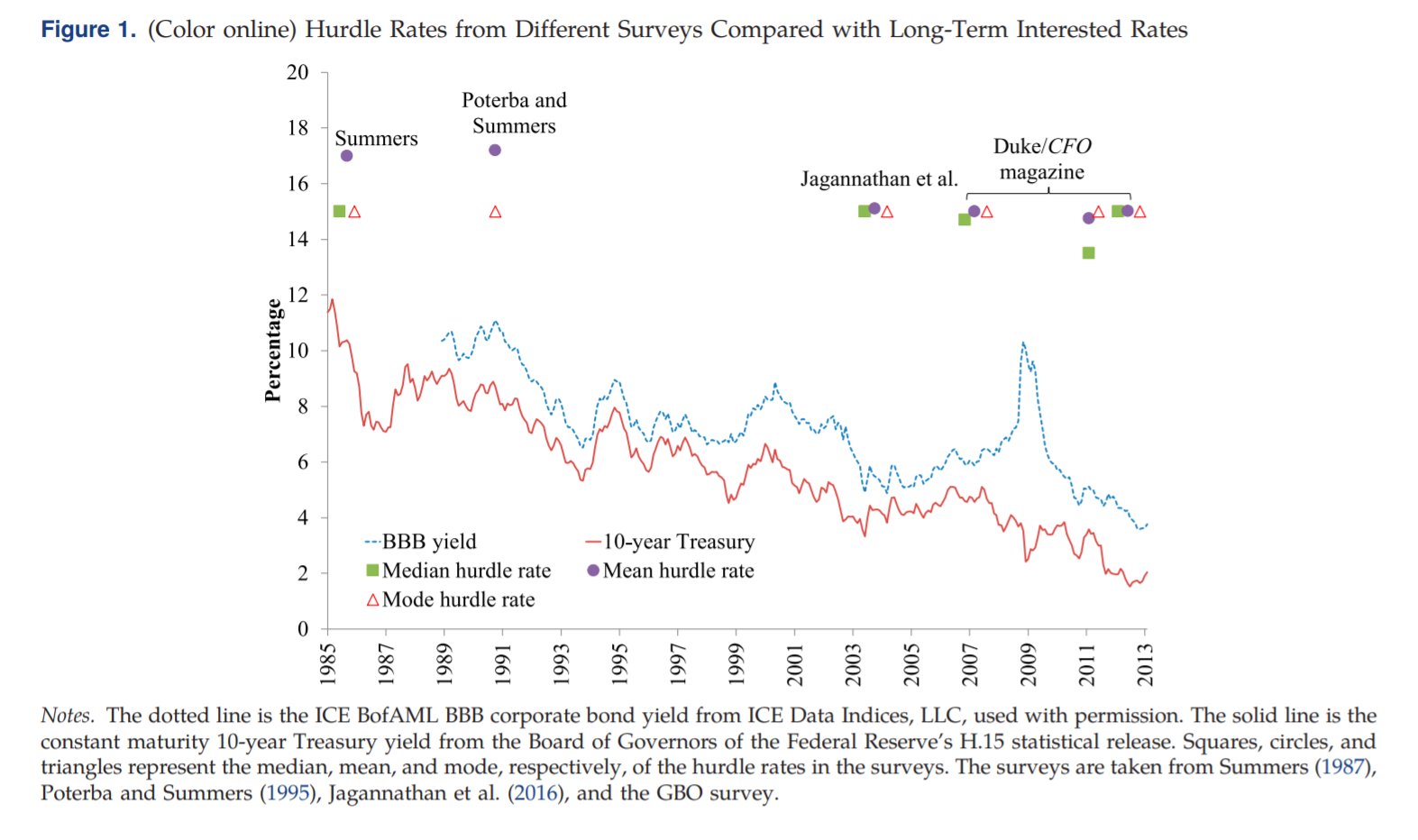

Sharpe and Saurez produce an excellent graph in their paper (reproduced below), showing that even as interest rates have fallen, hurdle rates haven’t really budged. Their work also shows that the interest rates firms face on the market regularly diverge from the “risk free” rates being set by governments. Hurdle rates have been so unresponsive to market interest rates that J.P. Morgan put out a report at the end of 2016 entitled “It’s time to reassess your hurdle rates”. This report basically begged businesses to lower their hurdle rates to match both the fall in “risk free” interest rates and their “implied equity cost of capital”.

Thus, firms have and use the discretion to avoid lowering their hurdle rates. There is even a paper about this published in The Journal of Financial Economics called “Why do firms use high discount rates?” Here the authors argue that high hurdle rates are meant to control the flow of investment projects, and keep them within a manageable level for expert employees and managers.

With this in mind, it is clearly not desirable for hurdle rates to change often — and they have nothing to do with the level of interest rates. Firms with the least financial constraints in fact tend to use the highest hurdle rates.

Keep in mind that firms tend to set fixed capital budgets, and grow them at stable rates. When the capital budget runs out, more investment projects are rarely — if ever — undertaken. When the capital budget still has funds left over, that money is likely to get spent. That’s true even if a specific project doesn’t pass the hurdle rate. Thus hurdle rates are rarely an enabler or a restraining device — especially in the aggregate. In fact, given how idiosyncratically businesses still calculate hurdle rates, especially after enormous pressure (and educational indoctrination) for at least half a century, I think hurdle rates are not serving the purpose finance scholars attribute to them and the use of conventional finance theory in their production is a cultural practice meant to preserve respectability in an environment where so many of one’s colleagues have gotten the same education. Where does that leave us?

Let’s summarize:

- Discount rates aren’t interest rates, especially risk free interest rates

- Hurdle rates aren’t discount rates

- Hurdle rates didn’t fall much after 2008, despite a sustained period of low risk free interest rates

- Hurdle rates aren’t the dominant factor in investment decision-making and projects regularly get left on the table even if their projected return is higher than the firm’s hurdle rate.

- The quantity of finance available is the major financial constraint on investment behavior, not interest rates on new debt.

- As a result, investment is insensitive to interest rates and more, not less, insensitive at low interest rates

- Investment of firms with high levels of savings are even more insensitive to interest rates

In short: Mian et al’s central narrative is fatally disrupted by the lack of low hurdle rates. Their paper may produce something interesting for mathematical economic theory, which contents itself with internal consistency over applicability. But for a model to have explanatory power, it must have discount rates which diverge widely from the risk free interest rate, and then remain diverged.

The implications of this are relevant for all future attempts at this variety of modelling. There are large sets of interest rates and discount rates in the economy, and we should not pretend otherwise. Economists are not well served by trying to model economies using “the interest rate”, rather than a wide interrelated structure of interest rates, discount rates and hurdle rates. This will always vastly overemphasize the importance of interest rates to investment decisions. Firm decision-making processes can’t be dismissed in trying to assess real world causality.

Thus, it can’t be said that low interest rates drive market concentration, at least based on this paper.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025