Trump’s 2026 Oil Crisis Again Highlights a Fundamental Truth: Bottlenecks Are the Quintessential Crisis of the 21st Century

One of the many things I’m months late to covering is the war of choice that the United States and Israel launched against Iran. This, of course, is related to geopolitical events in the middle east that have happened for the past three years. I have mostly avoided commentary on these events in this publication, instead writing about my personal opinions on social media. Yet I can no longer sustain a division between my commentary now that the baseline functioning of the oil market has been disrupted. This war, which started on February 28th has gone on for 108 days and, as of this writing, it has been announced that the U.S. and Iran have signed a deal. At the same time, Israel restarted bombing Beirut, Lebanon which has been a major sticking point for Iran. It is thus unclear whether this deal will survive Israeli intransigence.

In the future I plan to write about the Oil market over the past six months through the lens of my “Conventional Wisdom Processor” framework. For now, however, I want to make a broader point about this crisis. I want to point out how the shortages and disruptions to this key market are something of a preview of the defining economic problem of the 21st century- supply chain disruptions and bottlenecks. Regardless of when or how this crisis is resolved, the “bottleneck” problem will only intensify in the coming decades.

Some might think that the defining problem of the current Iran crisis is simply higher oil prices. Sure, there may be “pain at the pump”, but in the grand scheme of things higher oil prices will hurt households but not the overall functioning of the economy. Even at much higher prices, oil is a much smaller cost to the overall economy—and even to households- than it was fifty years ago. This, however, is the wrong way to think about this crisis. Without diminishing the impact on oil prices, which are produced by commodity exchanges in tandem with futures prices, the real crisis is a question of quantities. In 2019 my coauthors and I came off as odd and quixotic to emphasize that the core economic problem related to “inflation” was bottlenecks in key inputs. In the subsequent years, as a result of the supply chain disruptions coming from Covid, it became commonly appreciated how severe the impact of ongoing and systematic bottlenecks were.

Some have clearly treated the Covid experience as extraordinary. A bad memory to be forgotten, like the “Spanish” influenza epidemic of 1918 in the interwar period. What this crisis exemplifies is what many of us have been saying for a long time now: supply chain disruptions will be the norm, not the exception, in the 21st century. The most overriding reason is climate change. Even absent the intensifying geopolitical crises (like the current one) that climate change will exacerbate and worsen. That will have unavoidable economic impacts, as the modern global economy is built on an extraordinarily logistically complex global system of shipping, trucking and rail transportation. This system operates in…well, the actual world we all inhabit. Which means that sudden, dramatic and increasingly volatile changes to ocean and air currents, sea levels, ocean acidity and more will impact the production and circulation of millions upon millions of qualitatively unique inputs and outputs across the globe. Ecology and economy are not going to be obviously separable (if they ever were!) as climate change intensifies.

This system is also, in most respects, of extremely recent vintage. We’re accustomed to seeing the “economy” as something that “develops” and “grows” on a varying but more or less linear trajectory. But underneath the money flows and the price indices, let alone the reduction of these figures to a single number called “real” Gross Domestic Product, is an extraordinary and fragile accomplishment that is strikingly recent: a truly global system of rapid production and distribution of inputs and outputs. This system was built up on the back of a uniquely stable global political, legal and economic order which emerged for quite unique historical reasons. The rest of this century will see that “blip” in economic history continue to come unstuck. It was also built up atop of intensifying environmental impacts that’s full devastation and unsustainability has not remotely been reckoned with or abated.

Looked at from this angle, and from this historical vantage point, it is very likely that those of us alive in fifty years will be regaling younger people with seemingly mythic tails of this amazingly short apex for the global system of production and distribution. That is—if we don’t mobilize public institutions of all sorts to engage in a project of making this global system of production more sustainable and resilient. Of course, it remains an open question whether a truly global network of production and distribution can be sustainable. Not because it is not possible in principle, or one can’t set out relatively feasible technological arrangements where it could be. But as a historical example we have no precedent and ultimately the only way to prove that it is possible is to accomplish it.

In writing these words, I can’t help but think of one of the most famous parts of John Maynard Keynes’ “The Economic Consequences of the Peace” about the aftermath of World War One and the Versailles Treaty. This work which, in his time, made him famous- not the work of high theory he published seventeen years later called “The General Theory of Employment, Interest and Money”. The General Theory was mostly only ever of interest to specialists and entered popular consciousness as “Keynesianism” through economics textbooks and newspaper articles. It's worth quoting at length:

What an extraordinary episode in the economic progress of man that age was which came to an end in August, 1914! The greater part of the population, it is true, worked hard and lived at a low standard of comfort, yet were, to all appearances, reasonably contented with this lot. But escape was possible, for any man of capacity or character at all exceeding the average, into the middle and upper classes, for whom life offered, at a low cost and with the least trouble, conveniences, comforts, and amenities beyond the compass of the richest and most powerful monarchs of other ages.

The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep; he could at the same moment and by the same means adventure his wealth in the natural resources and new enterprises of any quarter of the world, and share, without exertion or even trouble, in their prospective fruits and advantages; or he could decide to couple the security of his fortunes with the good faith of the townspeople of any substantial municipality in any continent that fancy or information might recommend. He could secure forthwith, if he wished it, cheap and comfortable means of transit to any country or climate without passport or other formality, could despatch his servant to the neighboring office of a bank for such supply of the precious metals as might seem convenient, and could then proceed abroad to foreign quarters, without knowledge of their religion, language, or customs, bearing coined wealth upon his person, and would consider himself greatly aggrieved and much surprised at the least interference.

But, most important of all, he regarded this state of affairs as normal, certain, and permanent, except in the direction of further improvement, and any deviation from it as aberrant, scandalous, and avoidable. The projects and politics of militarism and imperialism, of racial and cultural rivalries, of monopolies, restrictions, and exclusion, which were to play the serpent to this paradise, were little more than the amusements of his daily newspaper, and appeared to exercise almost no influence at all on the ordinary course of social and economic life, the internationalization of which was nearly complete in practice. [emphasis added]

In English language commentary on the economy it is far too often taken for granted that the status quo that emerged in the 1990s was inevitable and forever, rather than a plate precariously spinning on a stick. Indeed, it's difficult to imagine a future without the global internet, let alone global real-time coordinated supply chains. But all of these things require the maintenance of an extraordinarily complex infrastructure to sustain. None more important than the planet itself. The established patterns and volatility of the seas and the winds are far more important “rails” for the functioning of our transportation systems, than actual rail lines and functioning ports.

This is a crucial and key reason why monetary estimates of the damages of climate change are nonsensical. These numbers only have meaning (to the extent they do have meaning) when contextualized by a global economy which presumes the functioning of our existing system. The obvious issue being that in the face of the kind of regionalized and global disruptions under discussion, that very system can’t be presumed. This issue has come into focus in mainstream policy circles under the prosaic term “physical risk”. But underneath this mild term, what we are really talking about is nothing less than the catastrophic collapse of key economic infrastructure beyond certain climatological “tipping points”. My colleague and good friend Boston University Law Professor Madison Condon does great scholarship in this area.

I emphasize the catastrophic nature of this problem not to be alarmist, or to claim that this is inevitable. I don’t think it is: we could still avert the worst outcomes… though the likelihood that we successfully avert climate catastrophe through making this system less vulnerable to damage from the impacts that are already “baked in” (while avoiding the impacts that aren’t) seems slimmer every day that slips past without fundamental change. Things are currently bleak, but not yet hopeless.

Which brings us back to the current geopolitical crisis. The alarming thing about this crisis is the extent to which the impacts of climate change have already contributed to geopolitical instability in the 21st century while, at the same time, this is clearly a war of choice for the Trump administration (along with Israel). The United States does not have a good track record of avoiding enormously destructive conflagrations when we were not (or are not) yet feeling the impacts of the climate changes which the 20th century’s fossil fueled prosperity inevitably is leading to. Modeling the feedback loops between economic activity as currently organized and the climate is still in its infancy. Modeling the feedback loops between economic activity, the climate, the organization of the twenty first century nation state (and the political and economic elites with a vested interest in solving conflicts militarily) is simply too grandiose a project to take on as a matter of mathematical modeling.

John Jay Economist J.W. Mason has a very good way of articulating this point. A “shock” in an economic model is simply a variable that an economist is choosing not to model and instead treats as “exogenous”. The economist does this because they want to highlight a specific set of interactions that they see as amenable to mathematical modeling—not to mention their domain expertise (if they truly have it). The problem becomes when this modeling choice is taken to be a fact about the real world. Geopolitical tensions, political instability and turmoil are not separable and unrelated to the behavior of the oil industry—or relevant markets. Climate change has a causal impact on the oil industry and market—and vice versa. In this sense, describing the current war on Iran as a “shock” to the oil market—or this or that climate disruption as a “shock” to the oil market—is misleading and a misnomer. It's a terminological leakage from the rarified debates among economic modelers to the world at large. In other words—it's not an analytic term, but an ideological pathogen.

Facing the current crisis, as well as the coming waves of systematic supply chain disruptions that will continue to define the 21st century, means beating back the conceptual limitations from this analytical vision. We need a completely different framework to understand the inherently circular production of inputs by means of inputs— to invoke a certain Italian economist—and that the ever ratcheting complexity and physical expansion of this circular process is not an inevitability, but really must be carefully maintained. It can only be maintained by managing and unwinding the pollutants which this process has filled the atmosphere with. Currently we are facing fundamental ecological disruption to the oceans and their various interlinked ecosystems—which undergird and make possible these circular economic processes.

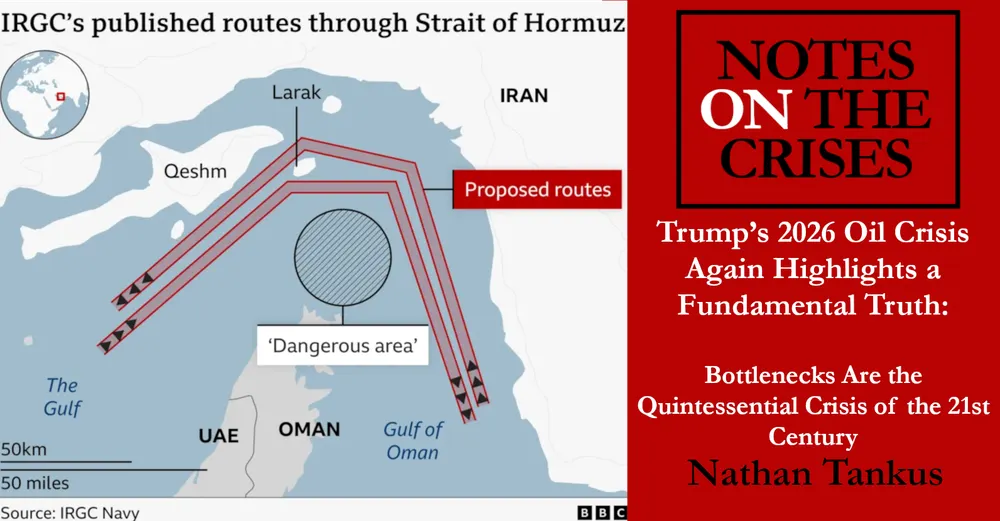

The conundrum we find ourselves in is that governance in the public interest is the only way to accomplish these goals but the apparatuses we have to pursue that kind of governance are themselves behaving as destructive “pollutants”. Trump- and the transnational political movement he is a part of- threaten this system of global production and circulation of inputs and outputs independently of their climate policies. After all, the recent oil crisis has not been because a “meteotsunami” hit the Strait of Hormuz—it's because of American-made bombs hitting Iran as a whole. The task of unwinding and pulling back the destructive forces our governments unleash is no less daunting than the task of building a “decarbonization state”.

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025