What is the Future of Fiscal Policy Now That the Election is Over?

The election has come and gone, a winner has been announced and now the fallout begins. While the details are still being hashed out, and president Trump along with most of the Republican party are not accepting the results (at least not yet), my interest is not so much in the near term partisan fights but the implications of what’s happened for the future of the Coronavirus Depression. To understand this, we must look to the results in the U.S. senate. What we find there is an exceedingly mixed result. Republicans have 50 seats, Democrats have 48 seats and the final results will come from two senate runoff elections in Georgia. Even if the Democrats win those two races, that thin margin would require each and every senator to agree to pass whatever they want to pass. As I said in my pre-election piece:

This means we could possibly go until February 2021 before seeing another economic package. Worse, that package may even require a Democratic senate to become law. It’s possible that even that scenario is optimistic — it could then take a significant amount of time for Democrats to agree on a package among themselves. What happens to millions upon millions of people in that agonizing waiting period? A winter filled with a third wave of Coronavirus and no economic support to individuals is a recipe for absolute disaster — over 200,000 Americans have already died.

Since I wrote this the third wave of Coronavirus has taken off and it seems more likely than ever that we will not have an economic package passed in February. In other words, I worry that fiscal cliffication is just going to intensify. Indeed, it's hard to imagine anything being able to break it at this point. The 2022 midterms are a long time away and there is no guarantee that the outcome would break the deadlock. We’ll likely see some sort of package go through congress in 2021 but it will very likely not be timely as the most optimistic scenarios laid out above had hoped. Meanwhile, the need is no less.

There are some overly rosy possible scenarios circulating financial twitter that make reviewing the unemployment situation important. Headline unemployment is still elevated but it is no longer at the high levels of the spring. However, this hides the damage that is happening underneath. Headline unemployment has mostly been driven by the behavior of temporary layoffs. Businesses laid people off because they had to shut down because of government order or they made discretionary decisions based on risk avoidant customers and their own risk judgments. The hope was that the virus would get under control and businesses could safely reopen. Instead, eventually businesses were reopened prematurely because of state and local government concerns over tax revenue combined with pressure to reopen from businesses who had inadequate (or no) federal fiscal support. We see this pattern in the temporary layoff data. There is a dramatic, unprecedented leep upwards and then a fall off- but temporary layoffs are still very elevated. But the real damage is in the permanent job losses.

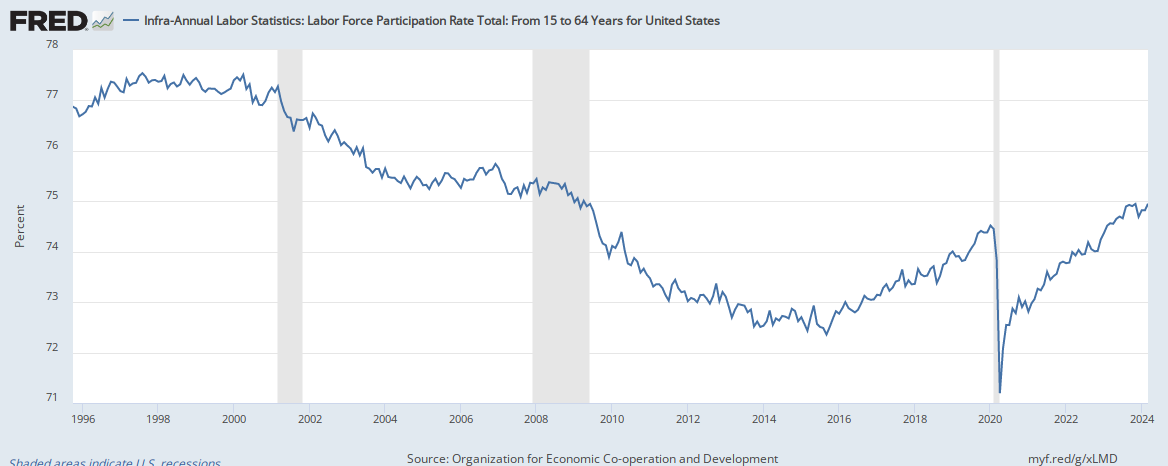

The distinction between temporary layoffs and permanent job losses is very underemphasized in economic reporting and has led to the underlying economic damage from being missed in a lot of economics coverage. My colleagues Alex Williams and Skanda Amarnath at Employ America did a great job of making this point in their piece “The Shock and The Slog” last month. While there has been a lot of recovery in temporary layoffs, there has been a steady increase in permanent layoffs and it will likely keep on increasing as more businesses shutter and the effects of expanded benefits start filtering through the economy (and our economic data). It’s also important to emphasize that labor force participation of individuals 15-64 has only partially recovered from a very steep drop, which makes headline unemployment appear rosier than it is.

{kind=link}

Worse still, the third wave of Coronavirus is in full swing. New York City schools could be shut as early as Monday, and indoor dining should probably already be shut. This second wave of shutdowns will be more economically harmful than the first wave because any savings they had were exhausted by the first wave and it is most likely that most affected businesses have already exhausted their access to credit (and perhaps even their willingness to take on more debt). It’s likely that the second wave of shutdowns will accelerate permanent job losses while the temporary job losses generate renewed drops in demand. In other words, the economic situation has still been deteriorating and it will likely get hammered at a time where fiscal support is, at best, months away.

In this context, the only game left in town is the Federal Reserve. Taking on responsibility for state and local governmental responses is the last thing that the Federal Reserve wants to do. However, the Federal Reserve has a mandate to to pursue maximum employment and price stability and meeting its maximum employment mandate requires it to use the tools it has available to do so. It can expand and use the Municipal Liquidity Facility. It can use its normal authority under section 14.2(b), as I’ve argued, in all sorts of creative but legal ways to support state and local governments. The Federal Reserve’s mandate is not to pursue maximum employment “unless doing so will cause too much political backlash”. It’s mandate is simply to pursue maximum employment and price stability. I’ve focused a lot on this point, and the Federal Reserve, because I have been concerned from nearly the beginning that fiscal cliffication would lead to inadequate congressional fiscal support and I wanted to preemptively push back against the idea that the Fed is doing all that it can do. It can do more, it must do more, political consequences be damned. The Federal Reserve’s “political capital” is not more important than the lives in the balance today.